American Options on Assets with Dividends Near Expiry

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

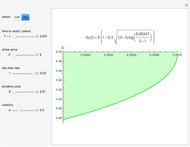

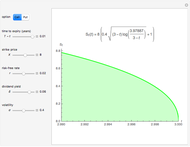

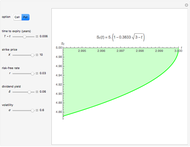

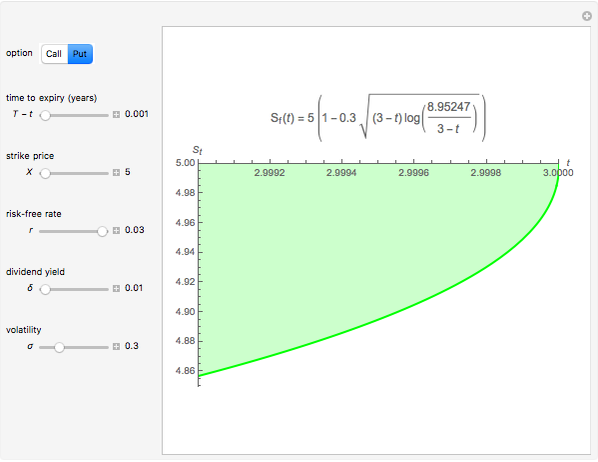

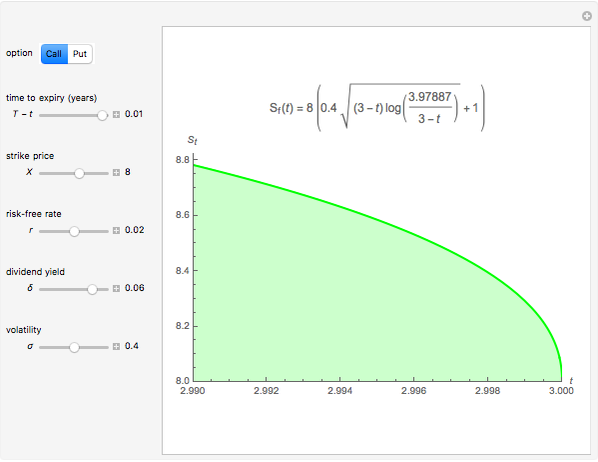

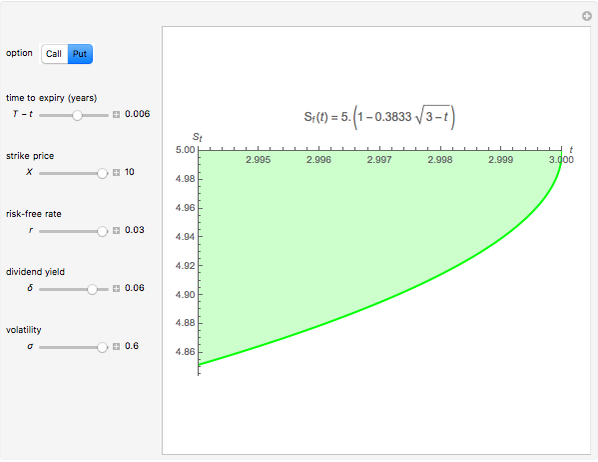

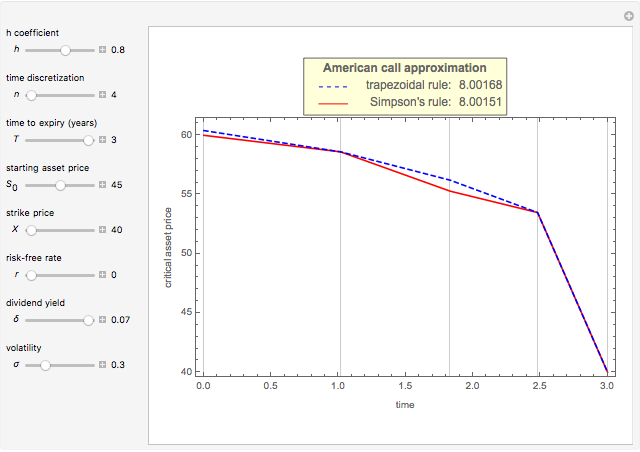

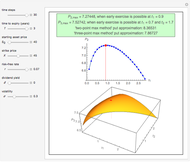

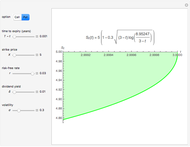

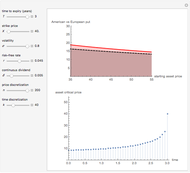

This Demonstration shows an explicit expression for the optimal exercise boundary of American options on assets with dividends. The function  of the optimal exercise boundary is only valid near expiry. The graph shows the curve (green line) near expiry for a three-year maturity option. For the option's holder, it is not optimal to exercise the option while the asset price

of the optimal exercise boundary is only valid near expiry. The graph shows the curve (green line) near expiry for a three-year maturity option. For the option's holder, it is not optimal to exercise the option while the asset price  moves within the colored area.

moves within the colored area.

Contributed by: Michail Bozoudis (March 2016)

Suggested by: Michail Boutsikas

Open content licensed under CC BY-NC-SA

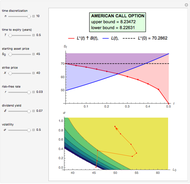

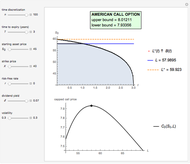

Snapshots

Details

J. D. Evans, R. Kuske, and J. B. Keller [1] provide explicit expressions valid near expiry ( ) for the optimal exercise boundary of American put and call options on assets with dividends. The results depend sensitively on the ratio of the dividend yield rate

) for the optimal exercise boundary of American put and call options on assets with dividends. The results depend sensitively on the ratio of the dividend yield rate  to the interest rate

to the interest rate  .

.

The optimal exercise boundary is singular at expiry, and its behavior is a classical problem of mathematical finance. The nature of these singularities cannot be determined by numerical calculation. Due to the behavior of the optimal exercise boundary near expiry, it is more difficult to retain accuracy in approximating the boundary using numerical methods and other types of approximations. These inaccuracies become more significant when pricing these options in the period close to expiry. In both lattice methods and the projected successive over-relaxation (SOR) method for partial differential equations (PDE), a fine discretization must be used near expiry, and this is both expensive and limited in accuracy. Therefore, the explicit expression near expiry can be combined with the numerical methods to calculate the optimal exercise boundary away from expiry.

The analytic expressions are derived twice: once by solving an integral equation and again by constructing matched asymptotic expansions. For  the put boundary near expiry tends parabolically to the value

the put boundary near expiry tends parabolically to the value  , where

, where  is the strike price, while for

is the strike price, while for  the boundary tends to in the parabolic-logarithmic form:

the boundary tends to in the parabolic-logarithmic form:

•  ,

,  ,

,

•  ,

,  ,

,

• ,  , where

, where  .

.

Analogous results for the optimal exercise boundary of an American call option on an asset with dividends are:

• ,  ,

,

• ,  ,

,

• ,  .

.

Reference

[1] J. D. Evans, R. Kuske, and J. B. Keller, “American Options on Assets with Dividends Near Expiry,” Mathematical Finance, 12(3), 2002 pp. 219–237. doi:10.1111/1467-9965.02008.

Permanent Citation

American Capped Call Options with Exponential Cap

American Capped Call Options with Exponential Cap

Michail Bozoudis American Capped Call Options with Constant Cap

American Capped Call Options with Constant Cap

Michail Bozoudis Kim's Method for Pricing American Options

Kim's Method for Pricing American Options

Michail Bozoudis A Canonical Optimal Stopping Problem for American Options

A Canonical Optimal Stopping Problem for American Options

Michail Bozoudis Kim's Method with Nonuniform Time Grid for Pricing American Options

Kim's Method with Nonuniform Time Grid for Pricing American Options

Michail Bozoudis Pricing American Options with the Lower-Upper Bound Approximation (LUBA) Method

Pricing American Options with the Lower-Upper Bound Approximation (LUBA) Method

Michail Bozoudis Pricing American Options with the Two- and Three-Point Maximum Methods

Pricing American Options with the Two- and Three-Point Maximum Methods

Michail Bozoudis Pricing Put Options with the Trinomial Method

Pricing Put Options with the Trinomial Method

Michail Bozoudis Pricing Put Options with the Binomial Method

Pricing Put Options with the Binomial Method

Michail Bozoudis A Recursive Integration Method for Options Pricing

A Recursive Integration Method for Options Pricing

Michail Bozoudis

-

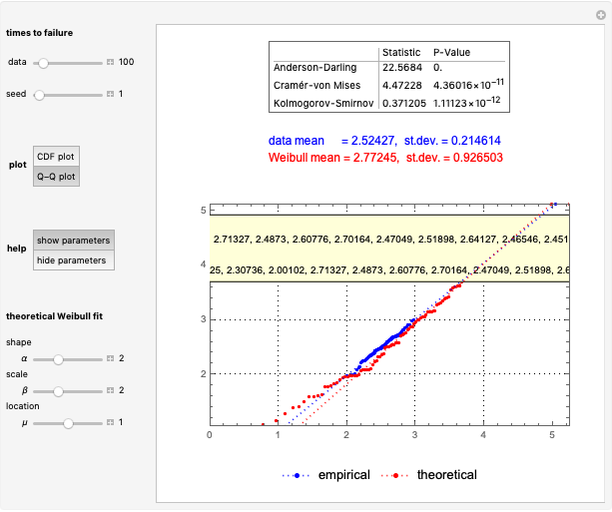

Fitting Times-to-Failure to a Weibull Distribution

Fitting Times-to-Failure to a Weibull Distribution

Michail Bozoudis -

A Canonical Optimal Stopping Problem for American Options

Michail Bozoudis -

A Recursive Integration Method for Options Pricing

Michail Bozoudis -

Adaptive Mesh Relocation-Refinement (AMrR) on Kim's Method for Options Pricing

Adaptive Mesh Relocation-Refinement (AMrR) on Kim's Method for Options Pricing

Michail Bozoudis -

Kim's Method with Nonuniform Time Grid for Pricing American Options

Michail Bozoudis -

Geometric Brownian Motion with Nonuniform Time Grid

Geometric Brownian Motion with Nonuniform Time Grid

Michail Bozoudis -

Kim's Method for Pricing American Options

Michail Bozoudis -

Simultaneous Confidence Interval for the Weibull Parameters

Simultaneous Confidence Interval for the Weibull Parameters

Michail Bozoudis -

Binomial Black-Scholes with Richardson Extrapolation (BBSR) Method

Binomial Black-Scholes with Richardson Extrapolation (BBSR) Method

Michail Bozoudis -

Pricing American Options with the Lower-Upper Bound Approximation (LUBA) Method

Michail Bozoudis -

American Options on Assets with Dividends Near Expiry

American Options on Assets with Dividends Near Expiry

Michail Bozoudis -

Hold-or-Exercise for an American Put Option

Hold-or-Exercise for an American Put Option

Michail Bozoudis -

American Capped Call Options with Exponential Cap

Michail Bozoudis -

American Capped Call Options with Constant Cap

Michail Bozoudis -

Pricing Put Options with the Crank-Nicolson Method

Pricing Put Options with the Crank-Nicolson Method

Michail Bozoudis -

Pricing Put Options with the Implicit Finite-Difference Method

Pricing Put Options with the Implicit Finite-Difference Method

Michail Bozoudis -

Estimating a Distribution Function Subject to a Stochastic Order Restriction

Estimating a Distribution Function Subject to a Stochastic Order Restriction

Michail Bozoudis -

Maximizing a Bermudan Put with a Single Early-Exercise Temporal Point

Maximizing a Bermudan Put with a Single Early-Exercise Temporal Point

Michail Bozoudis -

Fitting Data to a Lognormal Distribution

Fitting Data to a Lognormal Distribution

Michail Bozoudis -

SARIMA Process Forecasting Model

SARIMA Process Forecasting Model

Michail Bozoudis