Effect of Shock on the Stationary and Nonstationary Autoregressive (AR) Process

Initializing live version

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

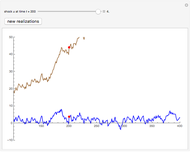

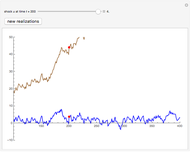

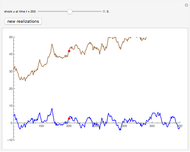

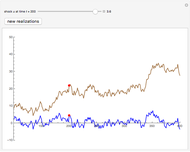

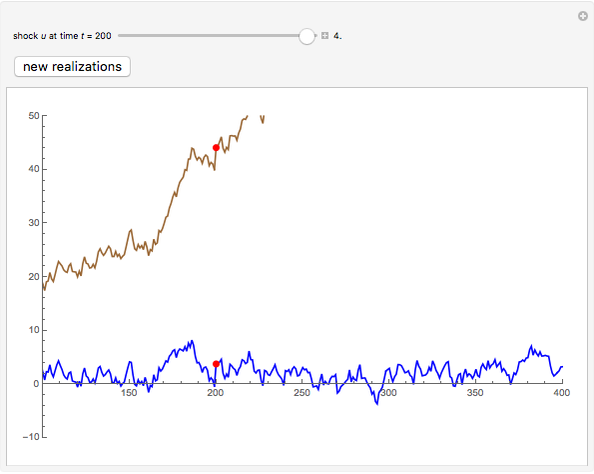

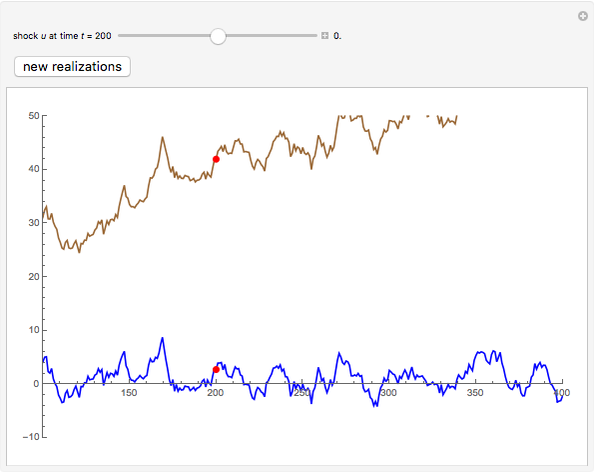

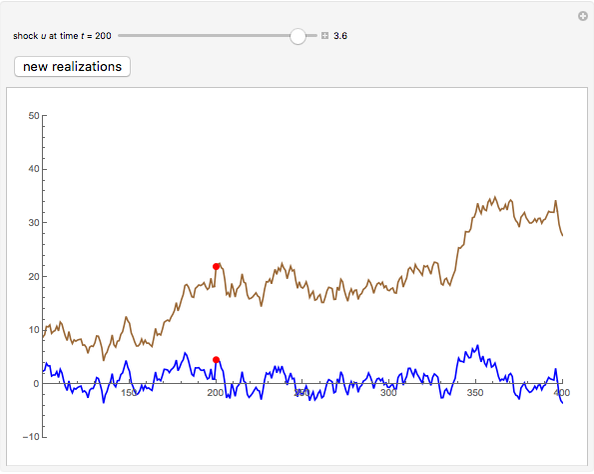

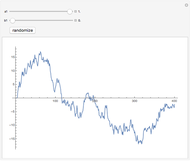

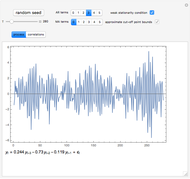

Changing the stochastic shock  occurring at time

occurring at time  , one can see its effect on later values of the time series in the stationary (blue) and nonstationary (brown) autoregressive AR(1) process. In the case of a stationary process, the effect of the shock disappears and the time series reverts to its mean value. In the nonstationary case, stochastic shock has a permanent effect and the process does not revert to its mean value.

, one can see its effect on later values of the time series in the stationary (blue) and nonstationary (brown) autoregressive AR(1) process. In the case of a stationary process, the effect of the shock disappears and the time series reverts to its mean value. In the nonstationary case, stochastic shock has a permanent effect and the process does not revert to its mean value.

Contributed by: Ako Sauga (August 2018)

Open content licensed under CC BY-NC-SA

Details

Snapshots

Permanent Citation

Related Demonstrations

More by Author

Autocorrelation and Partial Autocorrelation Functions of AR(1) Process

Autocorrelation and Partial Autocorrelation Functions of AR(1) Process

Jozef Barunik Two-Regime Threshold Autoregressive Model Simulation

Two-Regime Threshold Autoregressive Model Simulation

Jozef Barunik Autoregressive Moving-Average Simulation (First Order)

Autoregressive Moving-Average Simulation (First Order)

David von Seggern (University of Nevada) Simulating the Poisson Process

Simulating the Poisson Process

Heikki Ruskeepää Simulating the Birth-Death Process

Simulating the Birth-Death Process

Heikki Ruskeepää Estimating a Centered Ornstein-Uhlenbeck Process under Measurement Errors

Estimating a Centered Ornstein-Uhlenbeck Process under Measurement Errors

Didier A. Girard Distance Distributions in Finite Uniformly Random Point Processes

Distance Distributions in Finite Uniformly Random Point Processes

Sunil Srinivasa and Martin Haenggi Autoregressive Moving-Average Generator

Autoregressive Moving-Average Generator

Matus Baniar The Meixner Process

The Meixner Process

Andrzej Kozlowski Stable Lévy Process

Stable Lévy Process

Andrzej Kozlowski