Effect of Volatility and Drift on Random Walks

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

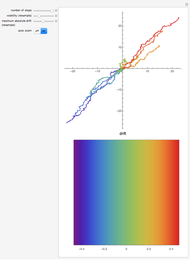

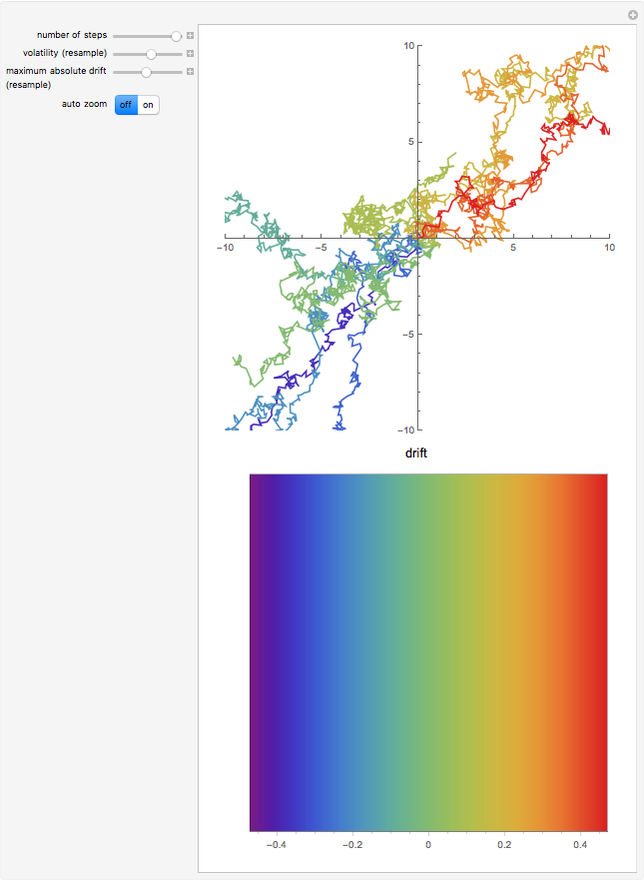

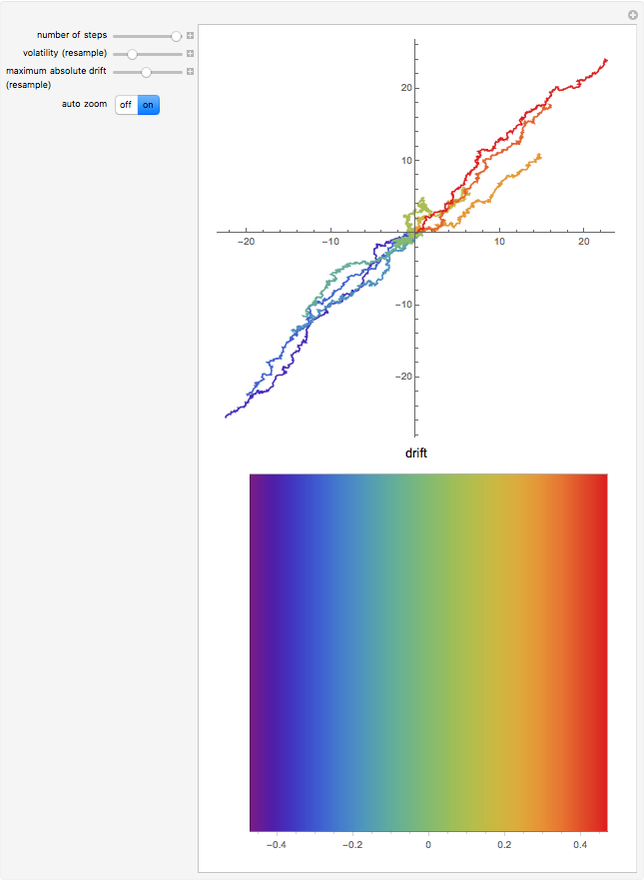

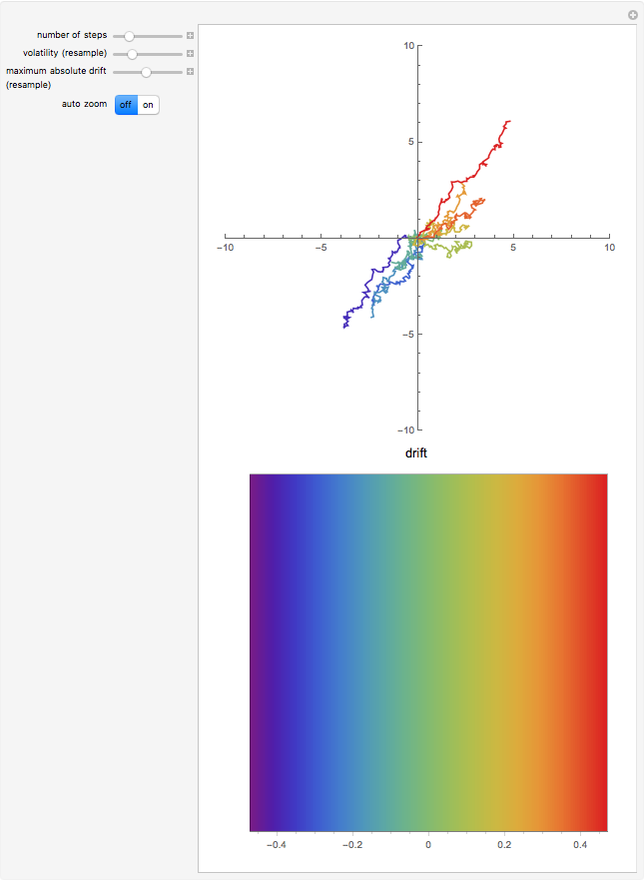

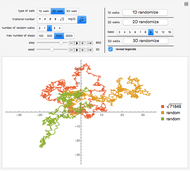

This Demonstration generates 10 sample paths of Brownian motion with values of drift governed by a user-defined maximum absolute value. The user can vary the number of steps and volatility of the random walk. A random walk is a mathematical model for the motion of particles in suspension in a fluid. The volatility represents the temperature of the fluid and drift represents an external force applied to the particles, such as an electric field. Drift values are the same for the  and

and  axes, resulting in drifting directions {1,1} and {-1,1}.

axes, resulting in drifting directions {1,1} and {-1,1}.

Contributed by: Felipe Dimer de Oliveira (August 2013)

Open content licensed under CC BY-NC-SA

Snapshots

Details

detailSectionParagraphPermanent Citation

"Effect of Volatility and Drift on Random Walks"

http://demonstrations.wolfram.com/EffectOfVolatilityAndDriftOnRandomWalks/

Wolfram Demonstrations Project

Published: August 21 2013

Constrained Random Walk

Constrained Random Walk

Erik Mahieu Self-Avoiding Random Walks

Self-Avoiding Random Walks

Rob Morris Cycles in Random Sample Permutations

Cycles in Random Sample Permutations

Michael Schreiber Markov Volatility Random Walks

Markov Volatility Random Walks

Jason Cawley Entropy of a Message Using Random Variables

Entropy of a Message Using Random Variables

Daniel de Souza Carvalho Comparing Real Mathematical Constants and Random Numbers

Comparing Real Mathematical Constants and Random Numbers

Daniel de Souza Carvalho Rauzy Fractals of Order Four

Rauzy Fractals of Order Four

Dieter Steemann Time Evolution of a Symmetric System

Time Evolution of a Symmetric System

Ulrich Mutze Mandelbrot Set Doodle

Mandelbrot Set Doodle

Michael Schreiber Real Number Walks versus Algorithmic Random Walks

Real Number Walks versus Algorithmic Random Walks

Khoa Tran and Laila Zhexembay