Inflation-Adjusted Yield

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

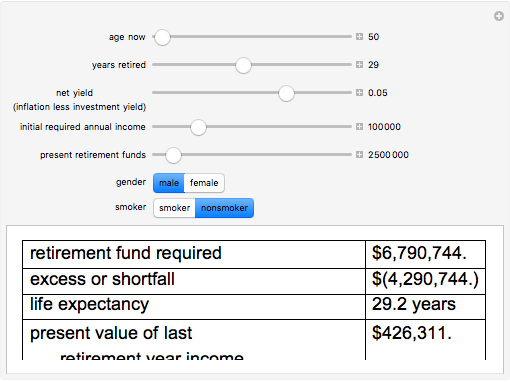

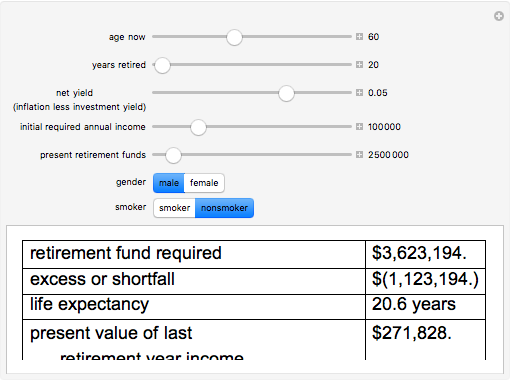

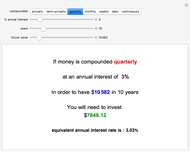

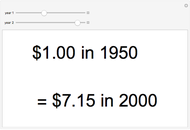

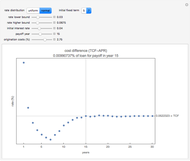

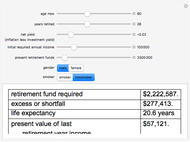

Under the assumption of continuously compounded real investment returns, this Demonstration illustrates how, in the presence of inflation, one's investment life planning turns on the net of nominal investment yield and inflation. Required annual income increases over time if lifestyle is to remain constant, since inflation affects nominal dollars. Yield on present retirement funds has the effect of (a) extending capital and (b) offsetting inflation. Retirement planning often crucially hinges on the net difference between yield and inflation, which can be netted against one another if compounding is continuous.

[more]

Contributed by: Roger J. Brown (March 2011)

Open content licensed under CC BY-NC-SA

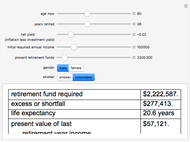

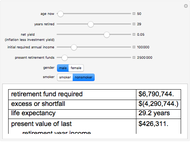

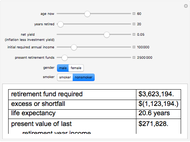

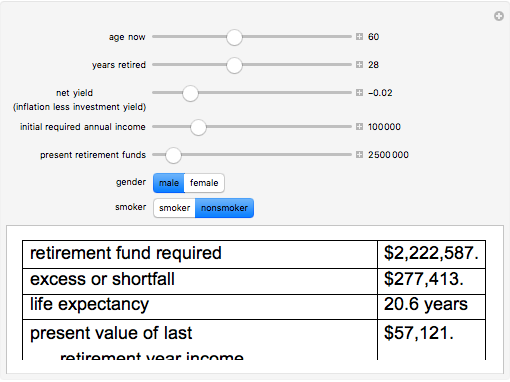

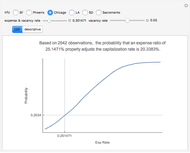

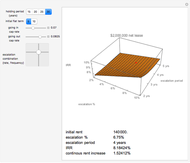

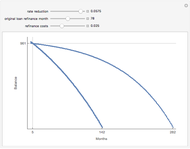

Snapshots

Details

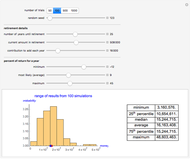

Mortality tables are, at best, a rough guideline. In general, more complicated actuarial computations are necessary. Regardless, this Demonstration should illustrate how incentives are changed by manipulation of the money supply. The decision to save versus spend is influenced by whether and how one can successfully overcome both investment risk and inflation risk. There are two segments of society who are difficult to tax directly: old people (because they vote) and poor people (because it is unconscionable). Inflation becomes a way to tax those segments. As the slider for net yield moves to the right dramatically different outcomes occur as inflation exceeds investment yield.

The interaction of the sliders can also produce some ghoulish implications. One might, given the parameters, be required to not only pick a retirement date but a date of death. Both of these depend on how economic events unfold. There is also an unfortunate but built-in anomaly. While the math of logarithms "smooths" the calculation process, life is, by contrast, bumpy. Spurts of earnings growth are not as perfectly aligned with spurts of inflation as the mathematics in this Demonstration assume.

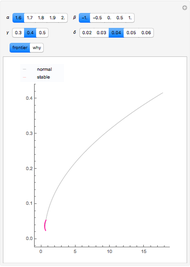

The term "net yield" has a special meaning here: the difference between investment return and inflation. It may seem counterintuitive that moving the slider to the left increases that difference. This arises from the log rule  where

where  and

and  are, respectively, the compounding effect of inflation on the cash flow in the numerator and the discounting effect of investment yield in the denominator of the expansion over time of income and the capital required to support it.

are, respectively, the compounding effect of inflation on the cash flow in the numerator and the discounting effect of investment yield in the denominator of the expansion over time of income and the capital required to support it.

Permanent Citation

Term Structure of Interest Rates

Term Structure of Interest Rates

Roger J. Brown The Value of Tax Deferral

The Value of Tax Deferral

Seth J. Chandler Price-Yield Curve

Price-Yield Curve

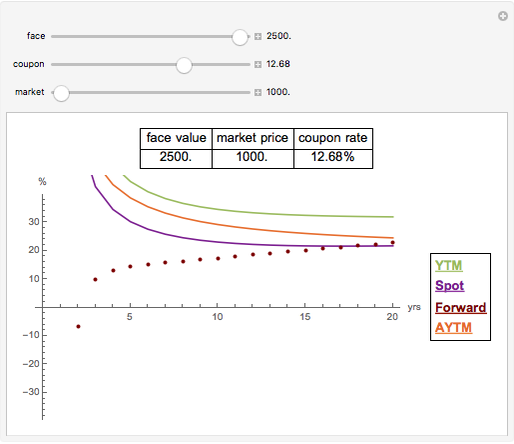

Fiona Maclachlan Yield, Spot, and Forward Curves

Yield, Spot, and Forward Curves

Gergely Nagy Fund Drawdown Simulation

Fund Drawdown Simulation

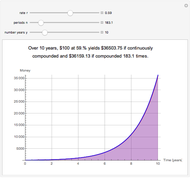

Joe O'Hara Continuous versus Compounded Interest

Continuous versus Compounded Interest

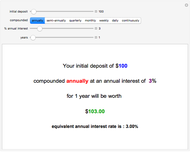

Jonathan Scherzer and Yossi Quint Future Value Calculator

Future Value Calculator

Sarah Lichtblau Present Value Calculator

Present Value Calculator

Craig Bauling Purchasing Power Calculator

Purchasing Power Calculator

Fiona Maclachlan Monte Carlo Simulation of Retirement Savings with Variable Annual Return

Monte Carlo Simulation of Retirement Savings with Variable Annual Return

Paul Savory (University of Nebraska-Lincoln)

-

Dissolving Partnerships

Dissolving Partnerships

Roger J. Brown -

Forming the Efficient Frontier When Returns Are Non-Normal

Forming the Efficient Frontier When Returns Are Non-Normal

Roger J. Brown -

Spectral Measures

Spectral Measures

Roger J. Brown -

Granger-Orr Running Variance Test

Granger-Orr Running Variance Test

Roger J. Brown -

Capitalization Rate Probability

Capitalization Rate Probability

Roger J. Brown -

Net Lease Economics

Net Lease Economics

Roger J. Brown -

The Refinance Decision

The Refinance Decision

Roger J. Brown -

True Cost of Variable Rate Mortgage Funds

True Cost of Variable Rate Mortgage Funds

Roger J. Brown -

Term Structure of Interest Rates

Roger J. Brown -

Generalized Central Limit Theorem

Generalized Central Limit Theorem

Roger J. Brown -

Inflation-Adjusted Yield

Inflation-Adjusted Yield

Roger J. Brown -

Simulating the IRR

Simulating the IRR

Roger J. Brown -

Real Options

Real Options

Roger J. Brown -

The Price-Terms Tradeoff

The Price-Terms Tradeoff

Roger J. Brown -

Fitting an Elephant

Fitting an Elephant

Roger J. Brown -

Solving the Subprime Loan Problem

Solving the Subprime Loan Problem

Roger J. Brown -

Why Location Matters: The Bid Rent Curve

Why Location Matters: The Bid Rent Curve

Roger J. Brown -

Explaining Real Estate Price Bubbles

Explaining Real Estate Price Bubbles

Roger J. Brown -

Value Added Growth Model

Value Added Growth Model

Roger J. Brown -

Connecting the CDF and the PDF

Connecting the CDF and the PDF

Roger J. Brown