Options: Time Value

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

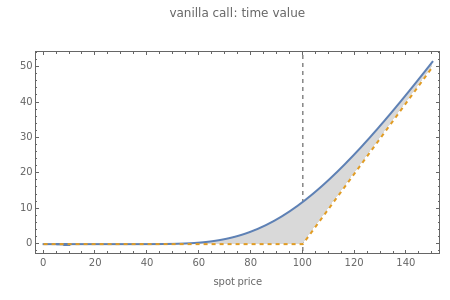

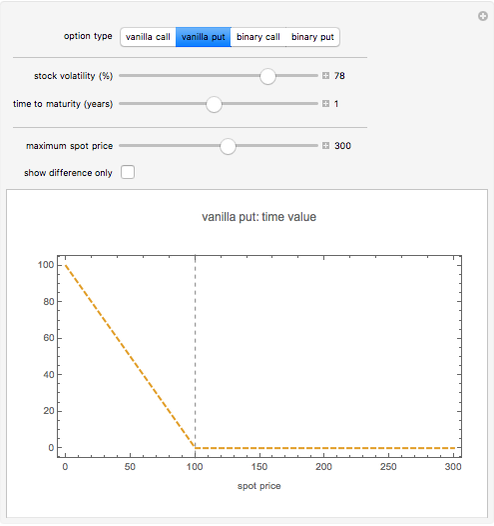

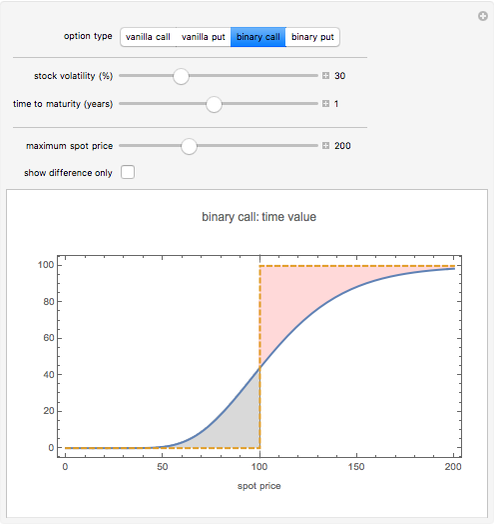

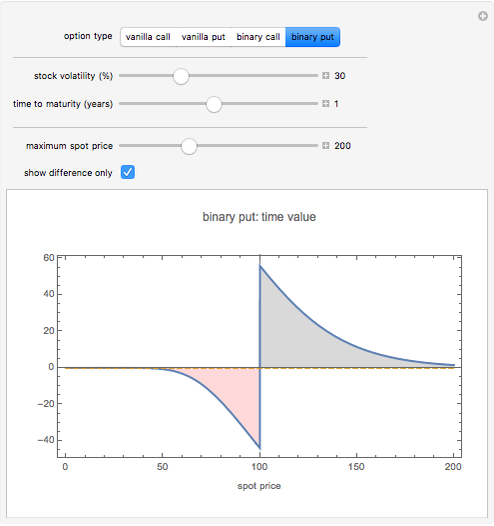

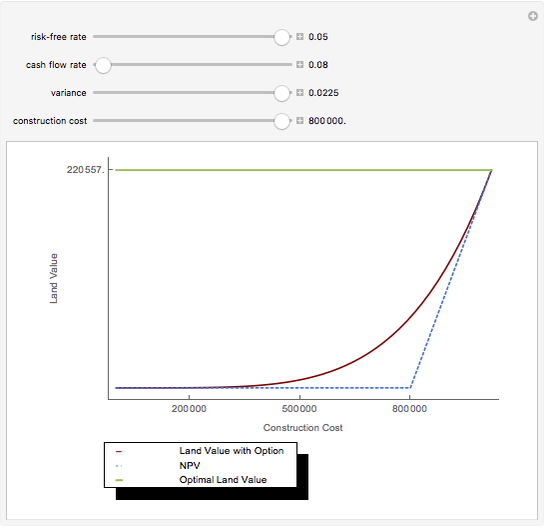

This Demonstration illustrates the concept of "time value" for European-style put and call options of both "vanilla" and "binary" type. The time value of an option is the difference between its current price and the payoff that would be obtained if it could be exercised at the current spot price. Regular vanilla options always have positive time value, whereas binary options can have either positive or negative time value. The magnitude of the time value is largest for "at-the-money" options (when the spot price equals the strike price). For simplicity, we assume zero interest rates and consider a fixed strike price of 100.

Contributed by: Peter Falloon (March 2011)

Open content licensed under CC BY-NC-SA

Snapshots

Details

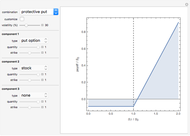

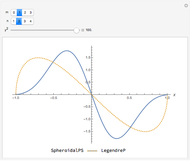

Snapshot 1: positive time value of vanilla put option

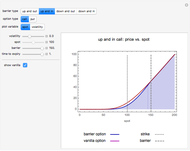

Snapshot 2: time value of binary call option: positive when spot is below strike, negative when it is above

Snapshot 3: an alternative view showing the time value explicitly rather than as the difference between two curves

Reference: J. C. Hull, Options, Futures, and Other Derivatives, 6th ed., Upper Saddle River, NJ: Prentice Hall, 2006.

Permanent Citation

"Options: Time Value"

http://demonstrations.wolfram.com/OptionsTimeValue/

Wolfram Demonstrations Project

Published: March 7 2011

Chooser Options

Chooser Options

Peter Falloon Pricing Power Options in the Black-Scholes Model

Pricing Power Options in the Black-Scholes Model

Peter Falloon Basic Option Trading Strategies

Basic Option Trading Strategies

Peter Falloon Barrier Option Pricing within the Black-Scholes Model

Barrier Option Pricing within the Black-Scholes Model

Peter Falloon Options Board Using Black-Scholes Prices

Options Board Using Black-Scholes Prices

Peter Falloon Option Prices in Merton's Jump Diffusion Model

Option Prices in Merton's Jump Diffusion Model

Peter Falloon Real Options

Real Options

Roger J. Brown Present Value Calculator

Present Value Calculator

Craig Bauling Net Present Value

Net Present Value

Fiona Maclachlan American Call and Put Option

American Call and Put Option

Andrzej Kozlowski

-

Option Prices in Merton's Jump Diffusion Model

Peter Falloon -

Chooser Options

Peter Falloon -

Binary Options: Pricing and Greeks

Binary Options: Pricing and Greeks

Peter Falloon -

Angular Spheroidal Functions as a Function of Spheroidicity

Angular Spheroidal Functions as a Function of Spheroidicity

Peter Falloon -

Hyperbolic Distribution

Hyperbolic Distribution

Peter Falloon -

Variance-Gamma Distribution

Variance-Gamma Distribution

Peter Falloon -

Options Board Using Black-Scholes Prices

Peter Falloon -

Properties of a Simple Random Walk with Boundaries

Properties of a Simple Random Walk with Boundaries

Peter Falloon -

Visualizing Superellipses

Visualizing Superellipses

Peter Falloon -

Haar Functions

Haar Functions

Peter Falloon -

Barrier Option Pricing within the Black-Scholes Model

Peter Falloon -

Clebsch-Gordan Coefficients

Clebsch-Gordan Coefficients

Peter Falloon -

Constant Coordinate Curves for Elliptic Coordinates

Constant Coordinate Curves for Elliptic Coordinates

Peter Falloon -

Chi-Squared Distribution and the Central Limit Theorem

Chi-Squared Distribution and the Central Limit Theorem

Peter Falloon -

Multiple Slit Diffraction Pattern

Multiple Slit Diffraction Pattern

Peter Falloon -

Constant Coordinate Curves for Parabolic and Polar Coordinates

Constant Coordinate Curves for Parabolic and Polar Coordinates

Peter Falloon -

Distribution of Returns from Merton's Jump Diffusion Model

Distribution of Returns from Merton's Jump Diffusion Model

Peter Falloon -

Pricing Power Options in the Black-Scholes Model

Peter Falloon -

Implied Volatility in Merton's Jump Diffusion Model

Implied Volatility in Merton's Jump Diffusion Model

Peter Falloon -

Game Clock

Game Clock

Peter Falloon