Pricing Put Options with the Crank-Nicolson Method

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

This Demonstration shows the application of the Crank–Nicolson (CN) method in options pricing. The CN method [1] is a central-time, central-space (CTCS) finite-difference method (FDM) for numerically solving partial differential equations (PDE). The CN scheme is the average of the implicit [2] and the explicit [3] schemes and can be used to numerically solve the Black–Scholes–Merton PDE [4, 5]. The CN scheme produces estimates of greater accuracy than either the explicit or implicit schemes.

Contributed by: Michail Bozoudis (December 2015)

Suggested by: Michail Boutsikas

Open content licensed under CC BY-NC-SA

Snapshots

Details

• The asset log price into  uniform steps with length

uniform steps with length  , using

, using  nodes indexed

nodes indexed  .

.

• The option maturity time into  uniform steps with length

uniform steps with length  , using

, using  nodes indexed

nodes indexed  .

.

Then  denotes the option value at the

denotes the option value at the  node. Three FDM schemas are widely used to approximate the derivatives:

node. Three FDM schemas are widely used to approximate the derivatives:

• The Crank-Nicolson [1] scheme, also referred to as "central-time, central-space (CTCS)", uses the average of the above approximations. The error term of the CN scheme is  .

.

Compared to the implicit scheme, the explicit is considered simpler and faster but less stable and accurate. It is relatively accurate for a small number of steps. The explicit scheme is similar to the trinomial tree [6], in that both provide an explicit formula for determining future states of the option process in terms of the current state, whereas the implicit and CN schemas require the iterative solution of linear equations linking consecutive time steps.

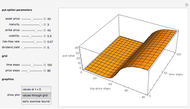

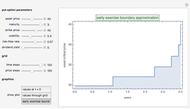

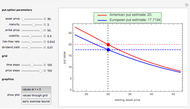

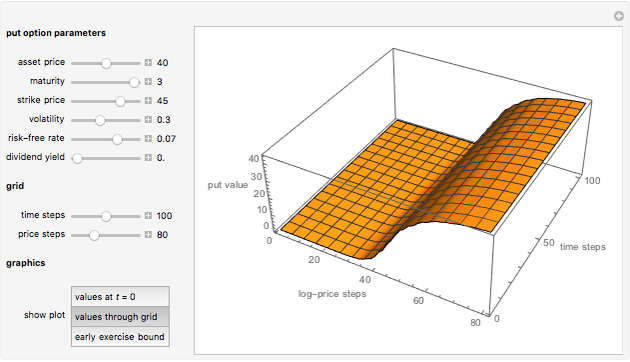

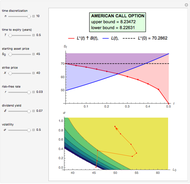

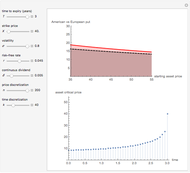

You can use the controllers to select the put option parameters and to determine the log price and time steps of the spatial grid. The minimum and maximum limits of the log-price grid are automatically estimated in order to ensure convergence and stability. You can choose among three graphical displays:

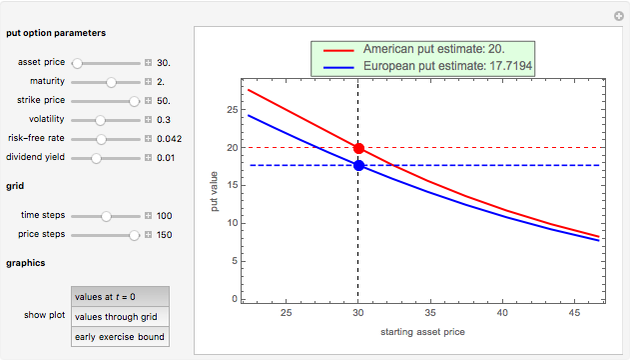

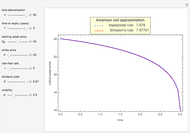

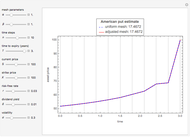

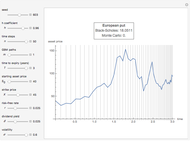

• The American and European put option estimates at  , depending on the underlying asset spot price. The European put value is never greater than the American, because the American put can be exercised at any time up to maturity, while the European put can only be exercised at maturity.

, depending on the underlying asset spot price. The European put value is never greater than the American, because the American put can be exercised at any time up to maturity, while the European put can only be exercised at maturity.

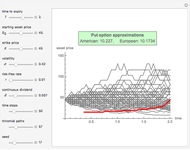

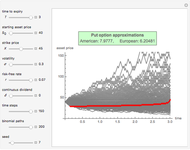

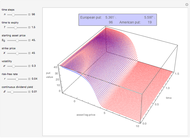

• The 3D illustration of the American put option values over the spatial grid.

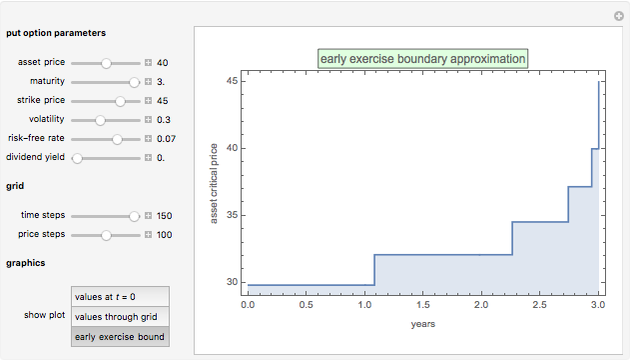

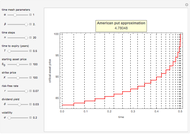

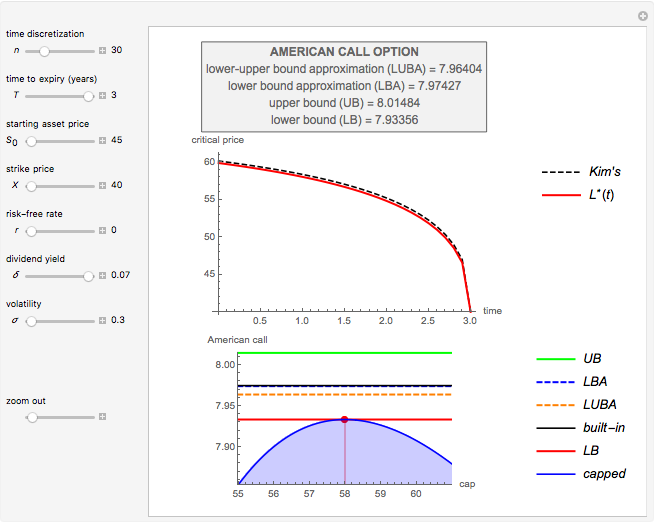

• The early exercise boundary approximation for the American put option. Whenever the asset price falls below this boundary, early exercise is considered optimal and the option is instantly exercised.

References

[1] J. Crank and P. Nicolson, "A Practical Method for Numerical Evaluation of Solutions of Partial Differential Equations of the Heat-Conduction Type," Proceedings of the Cambridge Philosophical Society, 43(1), 1947 pp. 50–67. doi:10.1017/S0305004100023197.

[2] M. J. Brennan and E. S. Schwartz, "Finite Difference Methods and Jump Processes Arising in the Pricing of Contingent Claims: A Synthesis," The Journal of Financial and Quantitative Analysis, 13(3), 1978 pp. 461–474. www.jstor.org/stable/2330152.

[3] J. Hull and A. White, "Valuing Derivative Securities Using the Explicit Finite Difference Method," Journal of Financial and Quantitative Analysis, 25(1), 1990 pp. 87–100. www.jstor.org/stable/2330889.

[4] F. Black and M. Scholes, "The Pricing of Options and Corporate Liabilities," Journal of Political Economy, 81(3), 1973 pp. 637–654. www.jstor.org/stable/1831029.

[5] R. Merton, "Theory of Rational Option Pricing," The Bell Journal of Economics and Management Science, 4(1), 1973 pp. 141–183. www.jstor.org/stable/3003143.

[6] P. Boyle, "Option Valuation Using a Three Jump Process," International Options Journal, 3(2), 1986 pp. 7–12.

Permanent Citation

Pricing Put Options with the Trinomial Method

Pricing Put Options with the Trinomial Method

Michail Bozoudis Pricing Put Options with the Binomial Method

Pricing Put Options with the Binomial Method

Michail Bozoudis Pricing Put Options with the Explicit Finite-Difference Method

Pricing Put Options with the Explicit Finite-Difference Method

Michail Bozoudis Kim's Method for Pricing American Options

Kim's Method for Pricing American Options

Michail Bozoudis A Recursive Integration Method for Options Pricing

A Recursive Integration Method for Options Pricing

Michail Bozoudis Kim's Method with Nonuniform Time Grid for Pricing American Options

Kim's Method with Nonuniform Time Grid for Pricing American Options

Michail Bozoudis Adaptive Mesh Relocation-Refinement (AMrR) on Kim's Method for Options Pricing

Adaptive Mesh Relocation-Refinement (AMrR) on Kim's Method for Options Pricing

Michail Bozoudis Pricing American Options with the Lower-Upper Bound Approximation (LUBA) Method

Pricing American Options with the Lower-Upper Bound Approximation (LUBA) Method

Michail Bozoudis Pricing American Options with the Two- and Three-Point Maximum Methods

Pricing American Options with the Two- and Three-Point Maximum Methods

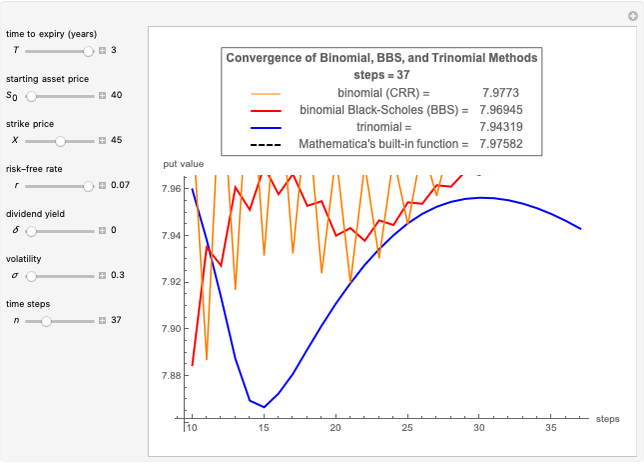

Michail Bozoudis Convergence of Binomial, Binomial Black-Scholes, and Trinomial Option Pricing Methods

Convergence of Binomial, Binomial Black-Scholes, and Trinomial Option Pricing Methods

Michail Bozoudis

-

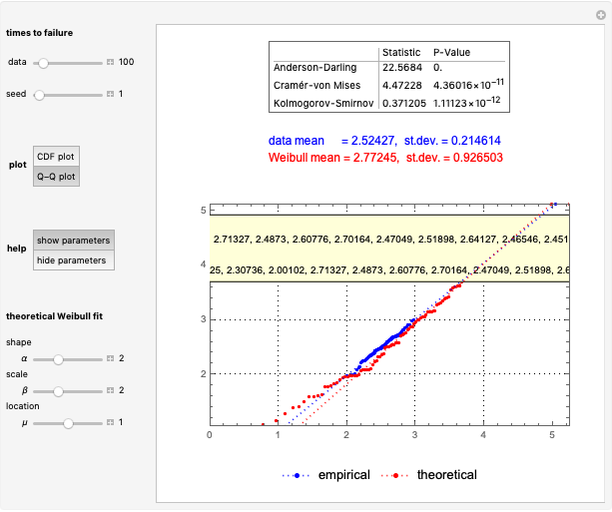

Fitting Times-to-Failure to a Weibull Distribution

Fitting Times-to-Failure to a Weibull Distribution

Michail Bozoudis -

A Canonical Optimal Stopping Problem for American Options

A Canonical Optimal Stopping Problem for American Options

Michail Bozoudis -

A Recursive Integration Method for Options Pricing

Michail Bozoudis -

Adaptive Mesh Relocation-Refinement (AMrR) on Kim's Method for Options Pricing

Michail Bozoudis -

Kim's Method with Nonuniform Time Grid for Pricing American Options

Michail Bozoudis -

Geometric Brownian Motion with Nonuniform Time Grid

Geometric Brownian Motion with Nonuniform Time Grid

Michail Bozoudis -

Kim's Method for Pricing American Options

Michail Bozoudis -

Simultaneous Confidence Interval for the Weibull Parameters

Simultaneous Confidence Interval for the Weibull Parameters

Michail Bozoudis -

Binomial Black-Scholes with Richardson Extrapolation (BBSR) Method

Binomial Black-Scholes with Richardson Extrapolation (BBSR) Method

Michail Bozoudis -

Pricing American Options with the Lower-Upper Bound Approximation (LUBA) Method

Michail Bozoudis -

American Options on Assets with Dividends Near Expiry

American Options on Assets with Dividends Near Expiry

Michail Bozoudis -

Hold-or-Exercise for an American Put Option

Hold-or-Exercise for an American Put Option

Michail Bozoudis -

American Capped Call Options with Exponential Cap

American Capped Call Options with Exponential Cap

Michail Bozoudis -

American Capped Call Options with Constant Cap

American Capped Call Options with Constant Cap

Michail Bozoudis -

Pricing Put Options with the Crank-Nicolson Method

Pricing Put Options with the Crank-Nicolson Method

Michail Bozoudis -

Pricing Put Options with the Implicit Finite-Difference Method

Pricing Put Options with the Implicit Finite-Difference Method

Michail Bozoudis -

Estimating a Distribution Function Subject to a Stochastic Order Restriction

Estimating a Distribution Function Subject to a Stochastic Order Restriction

Michail Bozoudis -

Maximizing a Bermudan Put with a Single Early-Exercise Temporal Point

Maximizing a Bermudan Put with a Single Early-Exercise Temporal Point

Michail Bozoudis -

Fitting Data to a Lognormal Distribution

Fitting Data to a Lognormal Distribution

Michail Bozoudis -

SARIMA Process Forecasting Model

SARIMA Process Forecasting Model

Michail Bozoudis