Rational Refinancing of a Residential Mortgage

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

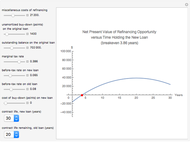

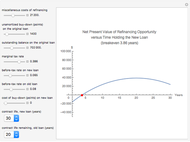

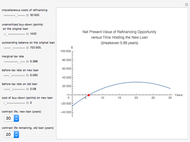

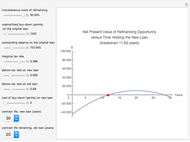

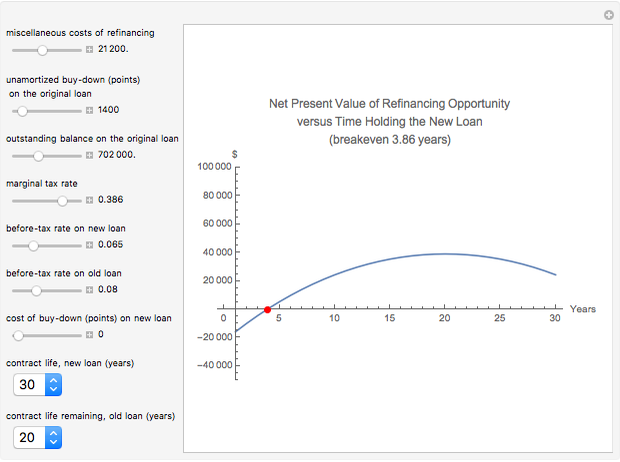

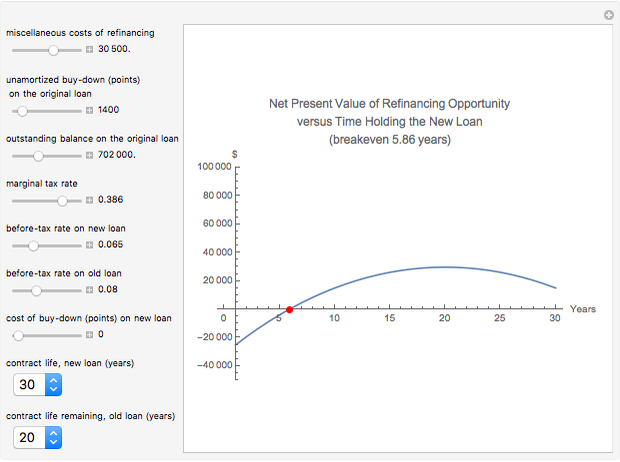

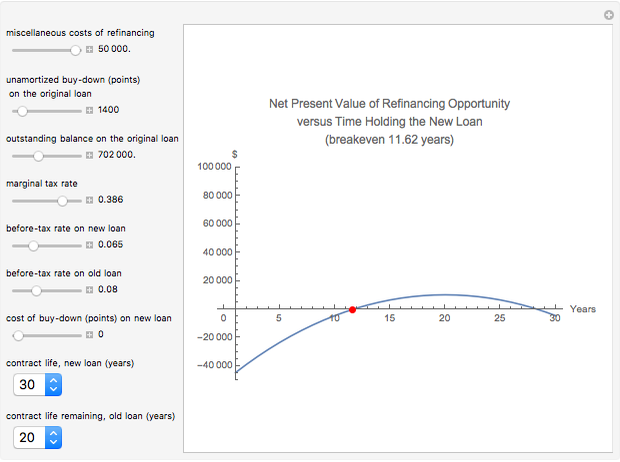

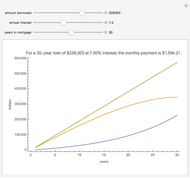

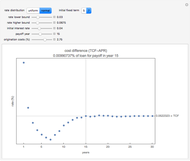

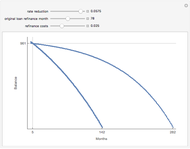

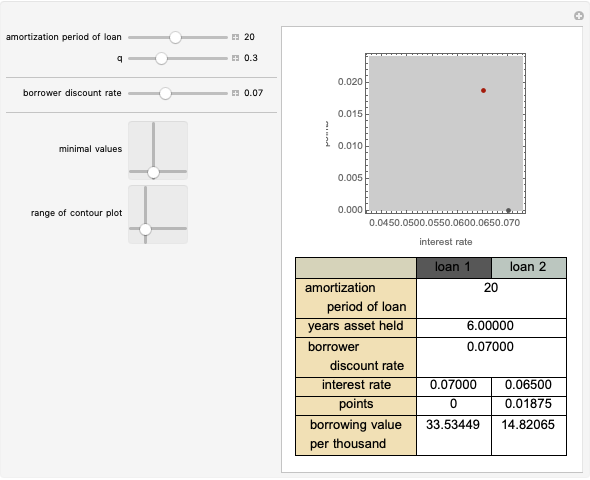

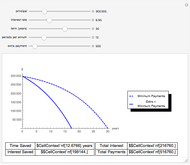

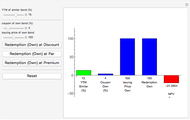

When interest rates drop, holders of residential mortgages face the decision of whether or not to refinance. Rationally, the decision involves taking the present value of expected mortgage payments under the existing loan and comparing that to the present value of expected payments under the refinanced loan, plus the costs associated with financing. The decision is complicated by the tax treatment of mortgage payments in the United States, which allows the interest portion of payments on a primary mortgage to be deducted from one's income tax, and which allows the cost of buying down the interest rate ("points") to be amortized over the contract life of the new loan, while any unamortized points on an existing loan can be deducted immediately if the loan is refinanced with a new lender.

[more]

Contributed by: Michael Stern (January 2014)

Open content licensed under CC BY-NC-SA

Snapshots

Details

Reference

[1] G. L. Hoover, "The Mortgage Refinance Decision: An Equation-Based Model," Financial Services Review, 12(4), 2003 pp. 319–337.

Permanent Citation

"Rational Refinancing of a Residential Mortgage"

http://demonstrations.wolfram.com/RationalRefinancingOfAResidentialMortgage/

Wolfram Demonstrations Project

Published: January 17 2014

Variation in the Value of Mortgage Strips

Variation in the Value of Mortgage Strips

Michael Stern Mortgage Calculator

Mortgage Calculator

Ed Pegg Jr True Cost of Variable Rate Mortgage Funds

True Cost of Variable Rate Mortgage Funds

Roger J. Brown and Tom Compton The Refinance Decision

The Refinance Decision

Roger J. Brown Pay the Points?

Pay the Points?

Seth J. Chandler Effect of Extra Payments on an Amortizing Loan

Effect of Extra Payments on an Amortizing Loan

Ben Carbery Determinants of the NPV of a Bond

Determinants of the NPV of a Bond

Thomas Lindner Financial Engineering of a Bond

Financial Engineering of a Bond

Thomas Lindner Bubbles in a Simple Behavioral Finance Model

Bubbles in a Simple Behavioral Finance Model

Kevin W. Capehart Post-Event Bonding

Post-Event Bonding

Seth J. Chandler