Simulating the IRR

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

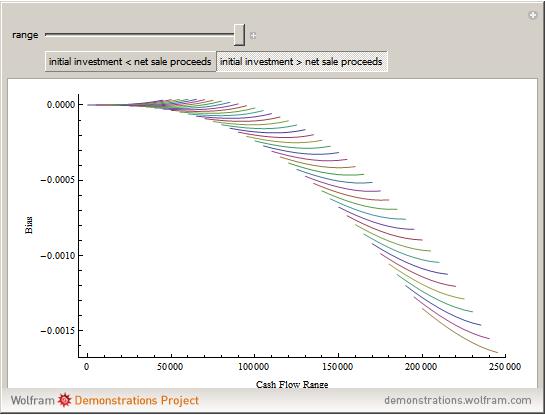

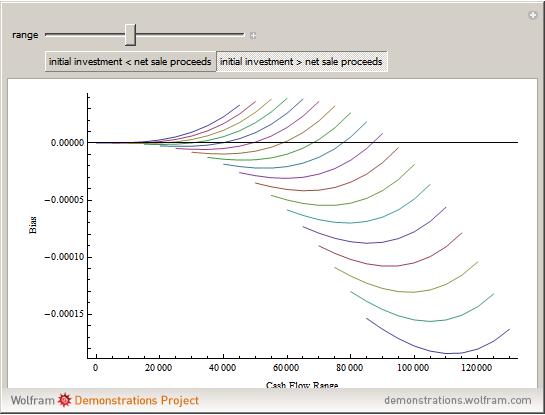

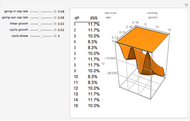

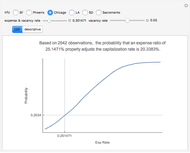

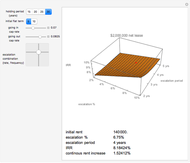

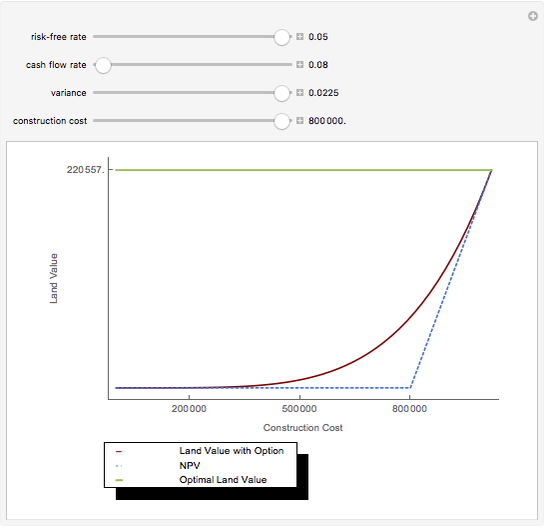

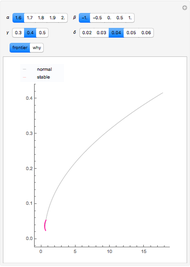

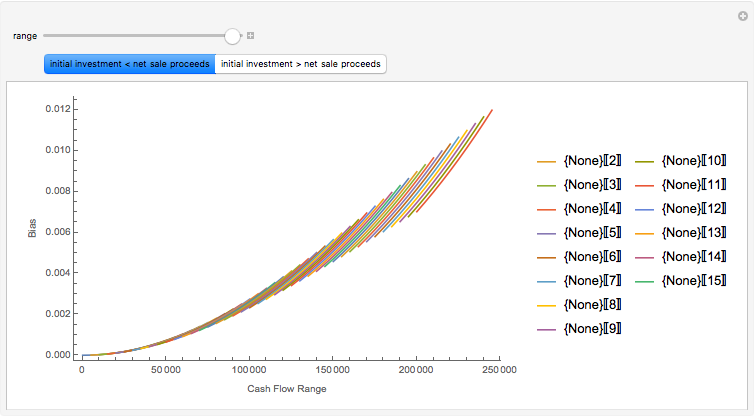

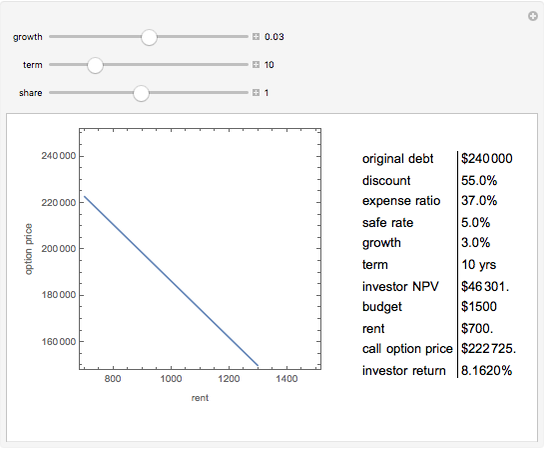

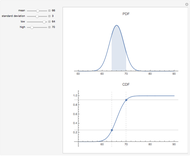

Monte Carlo simulation is useful when actual data does not exist or is hard to acquire. Many simulations are conducted for the purposes of predicting the mean or forming a probability distribution. The real estate analyst, often faced with a paucity of data, is tempted to simulate the internal rate of return (IRR) for a project. However, simulation introduces inaccuracies because of Jensen's inequality. Operationally, the problem arises from the curved nature of the IRR function. Simulation uses the concept of the expectation, which is a linear operator. Calculating an expectation for a curved function is a form of linear interpolation that has a built-in error to the extent the straight line between two points does not coincide with the curve. This Demonstration refers to this error as a bias.

[more]

Contributed by: Roger J. Brown (March 2011)

Reproduced by permission of Academic Press from Private Real Estate Investment ©2005

Open content licensed under CC BY-NC-SA

Snapshots

Details

J. L. W. V. Jensen, "Sur les fonctions convexes et les inégalités entre les valeurs moyennes," Acta Math., 30, 1906 pp. 175–193.

Jensen's inequality holds that a function  is convex in the interval

is convex in the interval  if and only if the following inequality is satisfied for all

if and only if the following inequality is satisfied for all  in and for all

in and for all  with

with  :

:  . A common description of this theorem would be that the function of the expectation is always less than or equal to the expectation of the function. The bias described in this Demonstration is a measure of how these two differ. The bias direction will depend on whether the function is convex or concave (resulting in "less than or equal to…" becoming "equal to or more than…" in the statement above).

. A common description of this theorem would be that the function of the expectation is always less than or equal to the expectation of the function. The bias described in this Demonstration is a measure of how these two differ. The bias direction will depend on whether the function is convex or concave (resulting in "less than or equal to…" becoming "equal to or more than…" in the statement above).

R. J. Brown, "Sins of the IRR," The Journal of Real Estate Portfolio Management, 12(2), 2006 pp. 195-200.

More information is available in Chapter Four of Private Real Estate Investment and at mathestate.com.

R. J. Brown, Private Real Estate Investment: Data Analysis and Decision Making, Burlington, MA: Elsevier Academic Press, 2005.

Permanent Citation

Simulating the Poisson Process

Simulating the Poisson Process

Heikki Ruskeepää Monte Carlo Simulation of Retirement Savings with Variable Annual Return

Monte Carlo Simulation of Retirement Savings with Variable Annual Return

Paul Savory (University of Nebraska-Lincoln) Expected Returns of the Dow Industrials, Fama-French Model

Expected Returns of the Dow Industrials, Fama-French Model

Jeff Hamrick and Jason Cawley The Price-Terms Tradeoff

The Price-Terms Tradeoff

Roger J. Brown The Effect of Holding Period on Real Estate Investment Return

The Effect of Holding Period on Real Estate Investment Return

Roger J. Brown Capitalization Rate Probability

Capitalization Rate Probability

Roger J. Brown Net Lease Economics

Net Lease Economics

Roger J. Brown Explaining Real Estate Price Bubbles

Explaining Real Estate Price Bubbles

Roger J. Brown Value Added Growth Model

Value Added Growth Model

Roger J. Brown Real Options

Real Options

Roger J. Brown

-

Dissolving Partnerships

Dissolving Partnerships

Roger J. Brown -

Forming the Efficient Frontier When Returns Are Non-Normal

Forming the Efficient Frontier When Returns Are Non-Normal

Roger J. Brown -

Spectral Measures

Spectral Measures

Roger J. Brown -

Granger-Orr Running Variance Test

Granger-Orr Running Variance Test

Roger J. Brown -

Capitalization Rate Probability

Roger J. Brown -

Net Lease Economics

Roger J. Brown -

The Refinance Decision

The Refinance Decision

Roger J. Brown -

True Cost of Variable Rate Mortgage Funds

True Cost of Variable Rate Mortgage Funds

Roger J. Brown -

Term Structure of Interest Rates

Term Structure of Interest Rates

Roger J. Brown -

Generalized Central Limit Theorem

Generalized Central Limit Theorem

Roger J. Brown -

Inflation-Adjusted Yield

Inflation-Adjusted Yield

Roger J. Brown -

Simulating the IRR

Simulating the IRR

Roger J. Brown -

Real Options

Roger J. Brown -

The Price-Terms Tradeoff

Roger J. Brown -

Fitting an Elephant

Fitting an Elephant

Roger J. Brown -

Solving the Subprime Loan Problem

Solving the Subprime Loan Problem

Roger J. Brown -

Why Location Matters: The Bid Rent Curve

Why Location Matters: The Bid Rent Curve

Roger J. Brown -

Explaining Real Estate Price Bubbles

Roger J. Brown -

Value Added Growth Model

Roger J. Brown -

Connecting the CDF and the PDF

Connecting the CDF and the PDF

Roger J. Brown