Tax Deferral

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

Investment income can be taxed in several ways by the government. In the United States, tax law generally chooses for each class of investment whether to tax growth in the value of the investment on an annual basis (even if the investor does not withdraw any funds) or defer taxation until a gain is "realized" by the investor, usually through withdrawing funds from the investment. This latter tax is often referred to as a "capital gains tax" and is generally applied to the difference between the value of the investment at the time of "realization" and the "basis" in the investment, generally the amount of money actually put into the investment over time.

[more]

Contributed by: Seth J. Chandler (September 2019)

Open content licensed under CC BY-NC-SA

Details

The formula for the share of the investor is:

,

,

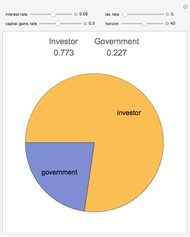

where  is the tax rate on annual investment growth,

is the tax rate on annual investment growth,  is the tax rate on capital gains,

is the tax rate on capital gains,  is the interest rate and

is the interest rate and  is the time horizon. The government's share is one minus the investor's share.

is the time horizon. The government's share is one minus the investor's share.

This formula is derived as follows:

Step 1: Let  be the amount invested by the taxpayer each year. Assume the tax is paid at the end of the year. Solve the dual recurrence equations

be the amount invested by the taxpayer each year. Assume the tax is paid at the end of the year. Solve the dual recurrence equations  and

and  , where

, where  represents the taxpayer's account and

represents the taxpayer's account and  represents the government's account after payment of income taxes but before consideration of any capital gains tax. Both accounts are set to zero at time 0.

represents the government's account after payment of income taxes but before consideration of any capital gains tax. Both accounts are set to zero at time 0.  \:201a and

\:201a and  . The solutions to these equations, which can be found using the Wolfram Language RSolveValue function, are

. The solutions to these equations, which can be found using the Wolfram Language RSolveValue function, are  and

and  .

.

Step 2: Now recognize that the capital gains payable at time  is the capital gains tax rate

is the capital gains tax rate  multiplied by the difference between

multiplied by the difference between  and

and  , the latter of which is the amount of money paid in by the taxpayer (the so-called "basis").

, the latter of which is the amount of money paid in by the taxpayer (the so-called "basis").

Step 3: Subtract the capital gains tax from the taxpayer's account and call it  ; add the capital gains tax to the government's account and call it

; add the capital gains tax to the government's account and call it  . Some algebra shows the results are

. Some algebra shows the results are  and

and  .

.

Step 4. Now divide the taxpayer's post-capital gains account  by the total

by the total  to get the taxpayer's share; divide the government's post-capital gains account

to get the taxpayer's share; divide the government's post-capital gains account  by the total

by the total  to get the government's share. The

to get the government's share. The  's in both equations cancel out and the results are

's in both equations cancel out and the results are  and

and  , respectively. One can check that the results are plausible by adding the two values together; the result is 1.

, respectively. One can check that the results are plausible by adding the two values together; the result is 1.

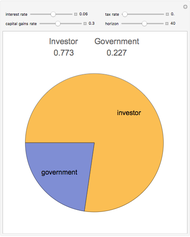

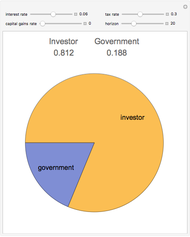

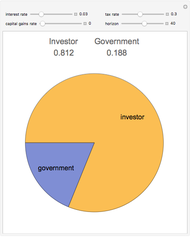

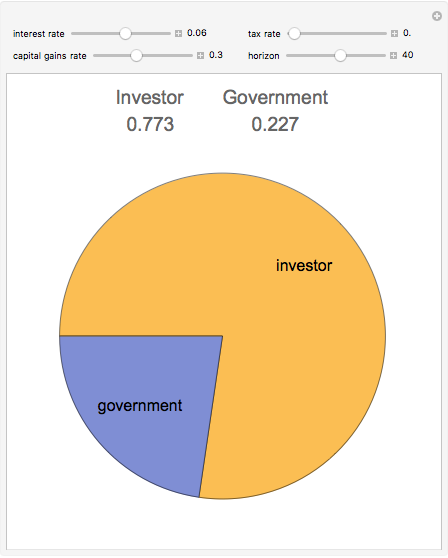

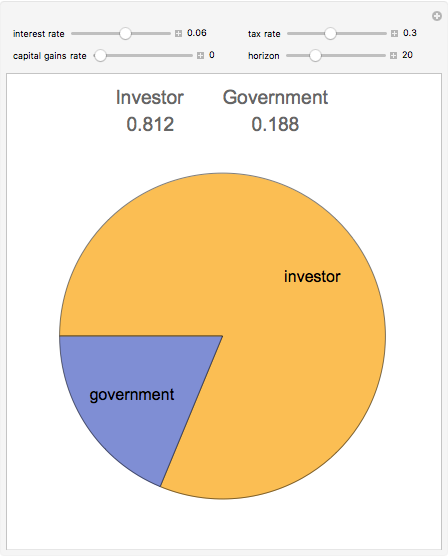

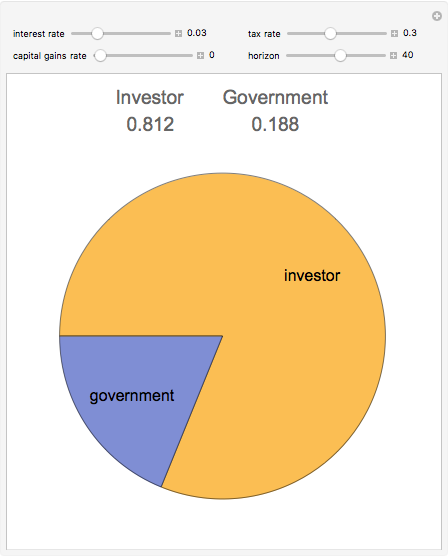

Snapshot 1: reducing the time horizon reduces the government's share

Snapshot 2: lowering the interest rate reduces the government's share

Snapshot 3: treating the investment growth as "ordinary income" results in a greater government share than deferral resulting from treatment as a "capital gain"

Reference

[1] A. Auerbach, "Retrospective Capital Gains Taxation," National Bureau of Economic Research, Working Paper No. 2792, 1988. (Aug 22, 2019) www.nber.org/papers/w2792.pdf.

Snapshots

Permanent Citation

The Value of Tax Deferral

The Value of Tax Deferral

Seth J. Chandler Tax Rates and Tax Revenue

Tax Rates and Tax Revenue

Seth J. Chandler Tax Incidence

Tax Incidence

Nicholas Palmer Supply and Demand Excise Tax

Supply and Demand Excise Tax

Nicholas Palmer Sales Tax and Discounts

Sales Tax and Discounts

Sarah Lichtblau Pay the Points?

Pay the Points?

Seth J. Chandler Post-Event Bonding

Post-Event Bonding

Seth J. Chandler The Efficient Dual-Limit Liability Insurance Contract

The Efficient Dual-Limit Liability Insurance Contract

Seth J. Chandler Property Coinsurance

Property Coinsurance

Seth J. Chandler Efficient Single Limit Liability Insurance

Efficient Single Limit Liability Insurance

Seth J. Chandler

-

Tax Deferral

Tax Deferral

Seth J. Chandler -

Multiplication of Hazard in Expo-Power Distributions

Multiplication of Hazard in Expo-Power Distributions

Seth J. Chandler -

Probit and Logit Models with Normal Errors

Probit and Logit Models with Normal Errors

Seth J. Chandler -

Insolvency Setoff

Insolvency Setoff

Seth J. Chandler -

Post-Event Bonding

Seth J. Chandler -

Emulating Land Use Evolution with a Cellular Automaton

Emulating Land Use Evolution with a Cellular Automaton

Seth J. Chandler -

General Assembly Resolution Viewer

General Assembly Resolution Viewer

Seth J. Chandler -

Random Acyclic Networks

Random Acyclic Networks

Seth J. Chandler -

A Theory of Insurance Lapses

A Theory of Insurance Lapses

Seth J. Chandler -

Asylum in the United States

Asylum in the United States

Seth J. Chandler -

Property Coinsurance

Seth J. Chandler -

The Persuasion Effect: A Traditional Two-Stage Jury Model

The Persuasion Effect: A Traditional Two-Stage Jury Model

Seth J. Chandler -

Cellular Automata with Global Control

Cellular Automata with Global Control

Seth J. Chandler -

Sports Seasons Based on Score Distributions

Sports Seasons Based on Score Distributions

Seth J. Chandler -

Evidentiary Uncertainty

Evidentiary Uncertainty

Seth J. Chandler -

Spectral Measures

Spectral Measures

Seth J. Chandler -

The Banzhaf Power Index of States for Presidential Candidates

The Banzhaf Power Index of States for Presidential Candidates

Seth J. Chandler -

Liability Insurance Desirability under Lognormal Loss Distributions

Liability Insurance Desirability under Lognormal Loss Distributions

Seth J. Chandler -

The Effects of Coinsurance and Deductibles on Optimal Precautions for Weibull-Distributed Loss

The Effects of Coinsurance and Deductibles on Optimal Precautions for Weibull-Distributed Loss

Seth J. Chandler