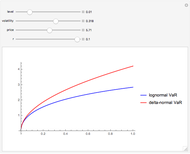

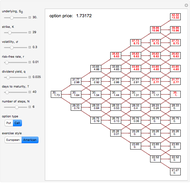

VaR Methods

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

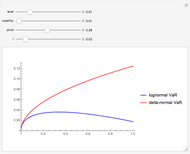

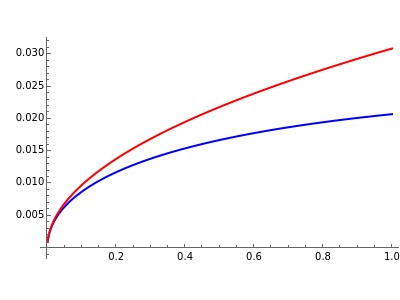

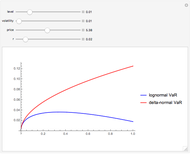

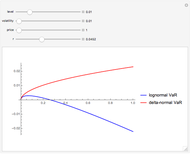

This Demonstration shows a comparison between calculating value at risk (VaR) with the delta-normal method and the lognormal distribution method.

[more]

Contributed by: Dimos Karaflos (January 2015)

Open content licensed under CC BY-NC-SA

Snapshots

Details

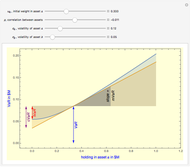

As you can see, the lognormal VaR method is more sensitive to volatility changes! This is due to the fact that the mean of the distribution depends on volatility. Specifically, this is due to the factor  .

.

The difference is that the same input values in these models assess different measures of loss over the same time horizon. This depends on the fact that the mathematical calculation is different in each case.

The lognormal VaR method is calculated with the code:

stockPrice-Quantile[LogNormalDistribution[Log[stockPrice]+(r-volatility^2/2) time,volatility Sqrt[time]],confidenceLevel]],

which is based on the geometric Brownian process.

The delta-normal method for VaR calculation is calculated with the code:

-Quantile[NormalDistribution[0,1],level] price volatility Sqrt[time],

where it is assumed that the coefficient of variation of the asset returns is described with the normal distribution N[0,1].

The delta-normal method is related to the hedging factor and sensitivity measure delta, which is multiplied in the formula of the delta-normal approach. In this Demonstration we refer to stock VaR, thus delta is equal to 1.

Choosing one model instead of another can lead to large changes in the variables.

The negative values of VaR denote that there is no potential of loss!

References

[1] J. C. Hull, Options, Futures, and Other Derivatives, 7th ed., Upper Saddle River, NJ: Prentice Hall, 2009.

[2] P. Jorion, Value at Risk: The New Benchmark for Managing Financial Risk, 3rd ed., New York: McGraw-Hill, 2007.

Permanent Citation

Portfolio Diversification Benefit from Subadditive VaR

Portfolio Diversification Benefit from Subadditive VaR

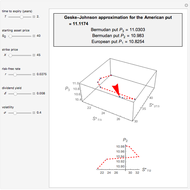

Pichet Thiansathaporn Geske-Johnson Method

Geske-Johnson Method

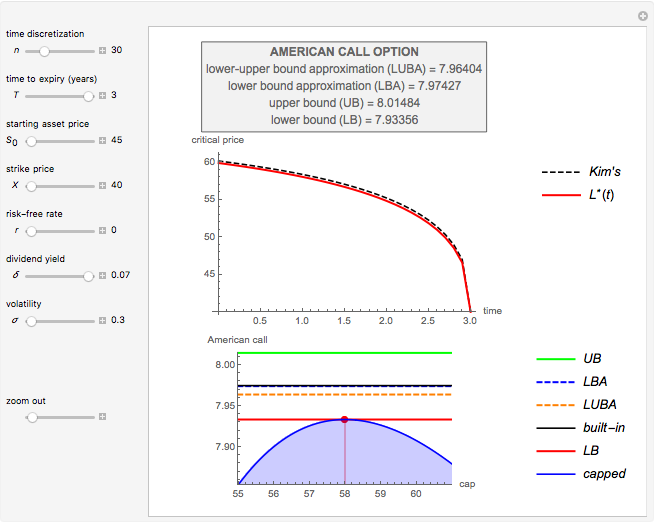

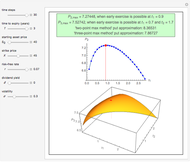

Michail Bozoudis Pricing American Options with the Lower-Upper Bound Approximation (LUBA) Method

Pricing American Options with the Lower-Upper Bound Approximation (LUBA) Method

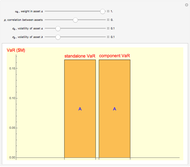

Michail Bozoudis Attributing Portfolio Value at Risk: Relations with Component VaR, Marginal VaR, and Incremental VaR

Attributing Portfolio Value at Risk: Relations with Component VaR, Marginal VaR, and Incremental VaR

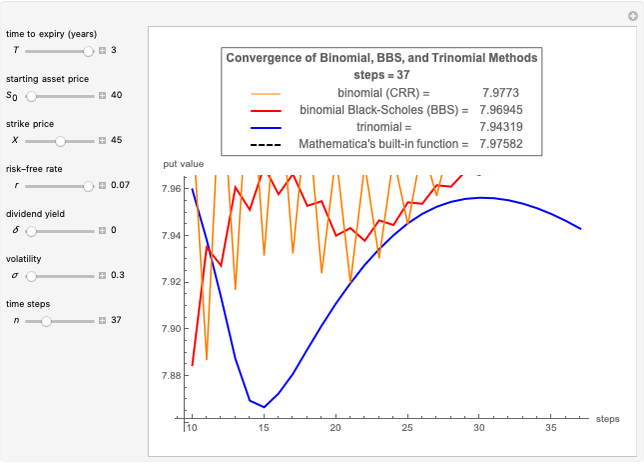

Pichet Thiansathaporn Convergence of Binomial, Binomial Black-Scholes, and Trinomial Option Pricing Methods

Convergence of Binomial, Binomial Black-Scholes, and Trinomial Option Pricing Methods

Michail Bozoudis Pricing American Options with the Two- and Three-Point Maximum Methods

Pricing American Options with the Two- and Three-Point Maximum Methods

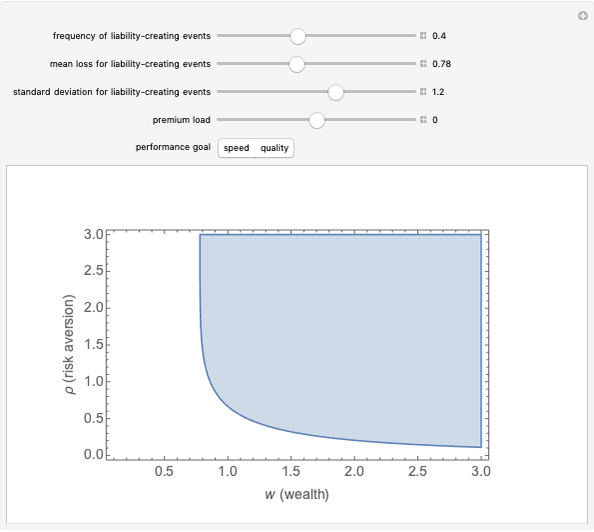

Michail Bozoudis Liability Insurance Desirability under Lognormal Loss Distributions

Liability Insurance Desirability under Lognormal Loss Distributions

Seth J. Chandler Trinomial Tree Option Pricing Method

Trinomial Tree Option Pricing Method

Darius Kirevicius A Recursive Integration Method for Options Pricing

A Recursive Integration Method for Options Pricing

Michail Bozoudis Kim's Method for Pricing American Options

Kim's Method for Pricing American Options

Michail Bozoudis