Compound Interest Table

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

These kinds of tables for looking up compound interest for various factors are very commonly used in engineering economics.

[more]

Contributed by: Vivek J Joshi (March 2011)

Open content licensed under CC BY-NC-SA

Snapshots

Details

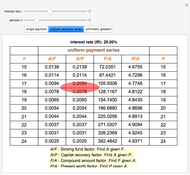

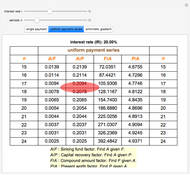

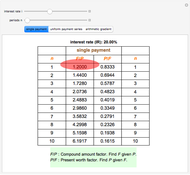

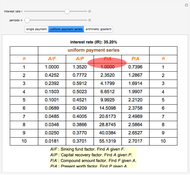

A single payment is a one-time investment of  compounded at interest rate

compounded at interest rate  for

for  periods that will reach a value

periods that will reach a value  . Or you can use the inverse, a discount factor, expressing the portion of a desired final value that must be invested to grow to in periods when invested at percent.

. Or you can use the inverse, a discount factor, expressing the portion of a desired final value that must be invested to grow to in periods when invested at percent.

A uniform payment means that instead of a one-time investment, equal amounts are paid into a fund that compounds at interest rate for each of the periods. " given " gives the portion of the desired future accumulated amount that must be contributed at each time period to reach the desired goal. " given " shows the amount that must be paid to amortize an amount borrowed over the same period, with interest paid rather than earned on the outstanding balance—for example, a conventional mortgage.

given " gives the portion of the desired future accumulated amount that must be contributed at each time period to reach the desired goal. " given " shows the amount that must be paid to amortize an amount borrowed over the same period, with interest paid rather than earned on the outstanding balance—for example, a conventional mortgage.

The inverses of those quantities are " given " and " given ". Notice that " given " shows the value of the accumulated sum of an amount , saved in each of periods and compounding at interest rate . On the other hand, " given " is the present value of an amount that can be paid off by making payments of amount .

For example, the  factor for 30 years at 5% is 15.3725, so payments of $12,000 a year would pay off a loan of 12000×15.3725 = $184,470 at that rate over that period. The

factor for 30 years at 5% is 15.3725, so payments of $12,000 a year would pay off a loan of 12000×15.3725 = $184,470 at that rate over that period. The  factor of 66.4388 means that the same $12,000 a year contributed to, for example, a retirement savings account earning 5% would grow in 30 years to $797,265.60.

factor of 66.4388 means that the same $12,000 a year contributed to, for example, a retirement savings account earning 5% would grow in 30 years to $797,265.60.

The arithmetic gradient series shows accumulations and amortizations possible by using increasing (rather than level) payments, where the amount of the payment starts at zero, but changes by  dollars per year. Otherwise, this part of the Demonstration should be interpreted like the level payment accumulation and amortization factor series. Note that series of payments or contributions that start above zero and then increase at a fixed rate can be calculated as the sum of two terms—a level payment series for the initial amount and a gradient series for the increases.

dollars per year. Otherwise, this part of the Demonstration should be interpreted like the level payment accumulation and amortization factor series. Note that series of payments or contributions that start above zero and then increase at a fixed rate can be calculated as the sum of two terms—a level payment series for the initial amount and a gradient series for the increases.

Reference: T. G. Eschenbach, D. G. Newnan, and J. P. Lavelle, Engineering Economic Analysis, New York: Oxford Univ. Press, 2004.

Permanent Citation

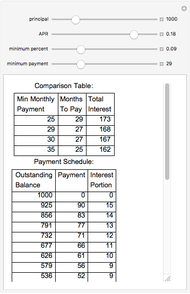

Analysis of Minimum Credit Card Payments

Analysis of Minimum Credit Card Payments

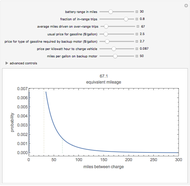

Andreas Lauschke The Equivalent Mileage of an Electric Vehicle with Backup Gasoline Propulsion

The Equivalent Mileage of an Electric Vehicle with Backup Gasoline Propulsion

Seth J. Chandler Term Structure of Interest Rates

Term Structure of Interest Rates

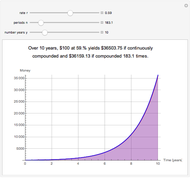

Roger J. Brown Continuous versus Compounded Interest

Continuous versus Compounded Interest

Jonathan Scherzer and Yossi Quint The 2001 CSO Mortality Tables

The 2001 CSO Mortality Tables

Seth J. Chandler Amortized Loan Interest and Principal

Amortized Loan Interest and Principal

Fiona Maclachlan Macroeconomic Effects of Interest Rate Cuts

Macroeconomic Effects of Interest Rate Cuts

Jason Cawley and Fred Meinberg (Wolfram Research) Inflation-Adjusted Yield

Inflation-Adjusted Yield

Roger J. Brown The Value of Tax Deferral

The Value of Tax Deferral

Seth J. Chandler Auto Loan Calculator

Auto Loan Calculator

Igor C. Antonio