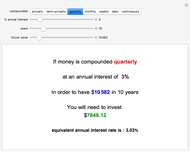

Discounted Present Value

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

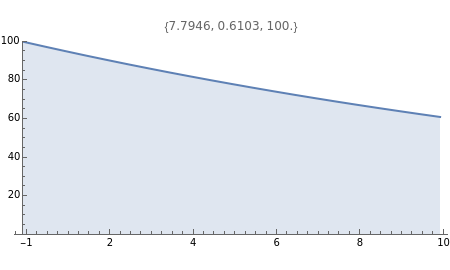

Discounted present value of a stream of level payments with an ending payment, for various discount rates, compounding periods, and number of years.

Contributed by: Jason Cawley (March 2011)

Open content licensed under CC BY-NC-SA

Snapshots

Details

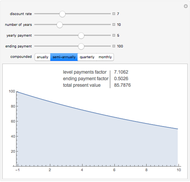

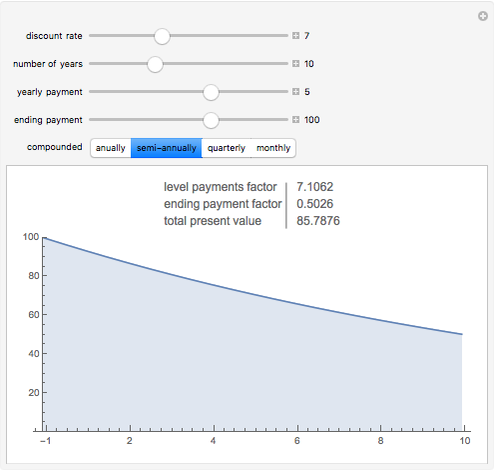

Snapshot 1: The price of a bond with a 5% coupon rate, lower than the 7% discounting rate.

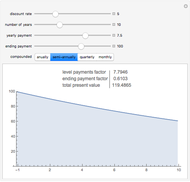

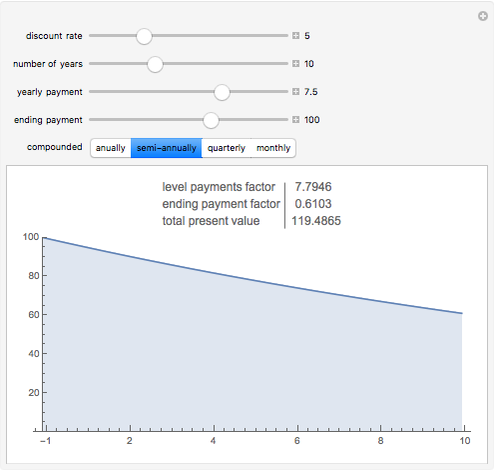

Snapshot 2: The price of a bond with a 7.5% coupon rate, higher than the 5% discounting rate.

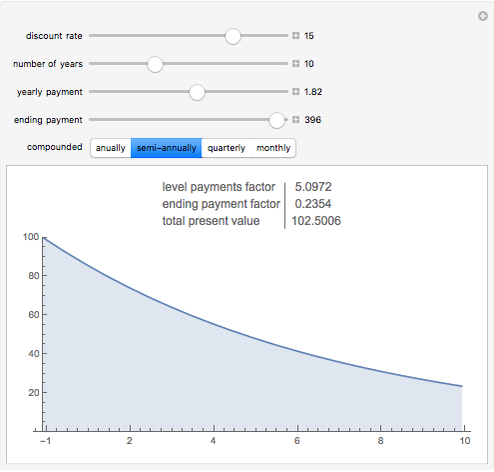

Snapshot 3: The 10-year price change a stock index paying 1.82% dividends would need to produce a 15% rate of return.

Snapshot 4: The actual return, 5.58%; the same index would pay if the price only increased by 50% over 10 years.

Snapshot 5: The break-even ending value, 37, needed to justify a long series of yearly inputs, discounted at 6%.

Snapshot 6: The internal rate of return achieved if instead the future value is 80.

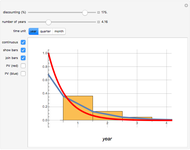

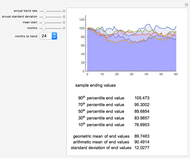

The discounted present value is the sum of the values of each of the individual cash flows, each discounted at the discount rate, for the time it occurs.

The graph shows the falling weight assigned to each cash flow, depending on its timing. The numbers in the table give the numerical total present value and its major components.

The discounted present value can be decomposed into a sum of two terms, one factor times the level payment, and another factor times the ending payment. The former is the sum of the series of discounting terms, and the latter is the last element of that series.

The yearly payment figure used must be an annualized figure, e.g. not a monthly payment. The compounded buttons change the discounting period used, and should be aligned with. the actual cash flows.

Yearly compounding is appropriate for planning purposes for many projects. Bonds generally compound twice a year. Dividends are generally quarterly. Rents and mortgages are generally monthly.

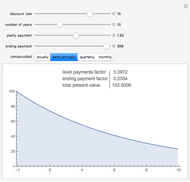

When the discount rate and the yearly payments are the same, the present value is the same as the ending payment. Thus a 100 ending value bond is "at par" if the prevailing interest rate is equal to its coupon rate.

When the discount rate is higher than the yearly payments, the present value is lower then the ending payment. A bond with a low coupon is thus "at a discount".

When the discount rate is lower than the yearly payments, the present value is higher than the ending payment. A bond with a high coupon is "at a premium".

A zero payment will give the price of a zero coupon bond or the value of a single future cash flow.

Targeted rates of return from appreciating assets can be analyzed by inputing the desired return as the discount rate, and seeing what ending payment would be required to realize that rate of return.

Alternately, estimates of future value can be input as the ending payment, and the discount rate adjusted until the present value reads the amount initially invested. The discount rate that equalizes the two is the rate of return that ending value would provide.

A negative level of payments can be used to determine the present value or internal rate of return of ongoing investment, returned in a lump sum value at the end.

Breakeven points between positive and negative inputs and outputs can be investigated by asking at what value of the parameters the discounted present value is zero.

Permanent Citation

"Discounted Present Value"

http://demonstrations.wolfram.com/DiscountedPresentValue/

Wolfram Demonstrations Project

Published: March 7 2011

Net Present Value

Net Present Value

Fiona Maclachlan Value Added Growth Model

Value Added Growth Model

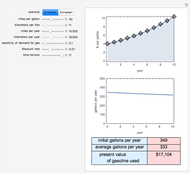

Roger J. Brown The Present Value of Future Gas Use

The Present Value of Future Gas Use

Seth J. Chandler Present Value Calculator

Present Value Calculator

Craig Bauling Exploring Social Choice Theory

Exploring Social Choice Theory

Earl Mitchell Macroeconomic Effects of Interest Rate Cuts

Macroeconomic Effects of Interest Rate Cuts

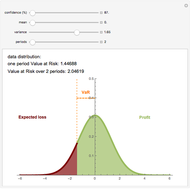

Jason Cawley and Fred Meinberg (Wolfram Research) Value at Risk

Value at Risk

Gergely Nagy Options: Time Value

Options: Time Value

Peter Falloon Future Value Calculator

Future Value Calculator

Sarah Lichtblau Continuous and Discrete Time Discounting

Continuous and Discrete Time Discounting

Arne Eide

-

Expected Returns of the Dow Industrials, Beta Model

Expected Returns of the Dow Industrials, Beta Model

Jason Cawley -

Comparing Data on Countries

Comparing Data on Countries

Jason Cawley -

Rank Plots for Countries

Rank Plots for Countries

Jason Cawley -

Country Groups

Country Groups

Jason Cawley -

Country Data and Benford's Law

Country Data and Benford's Law

Jason Cawley -

Cellular Automata with Global Control

Cellular Automata with Global Control

Jason Cawley -

Simulating the 2008 U.S. Presidential Election

Simulating the 2008 U.S. Presidential Election

Jason Cawley -

Exploring Social Choice Theory

Jason Cawley -

Fully Random, Five-Rule Interactive Cellular Automata (ICA)

Fully Random, Five-Rule Interactive Cellular Automata (ICA)

Jason Cawley -

Algorithmic Architecture with Cellular Automata

Algorithmic Architecture with Cellular Automata

Jason Cawley -

Modeling Return Distributions

Modeling Return Distributions

Jason Cawley -

Expected Returns of the Dow Industrials, Fama-French Model

Expected Returns of the Dow Industrials, Fama-French Model

Jason Cawley -

Credit Risk

Credit Risk

Jason Cawley -

Highlighting Patterns in Cellular Automata

Highlighting Patterns in Cellular Automata

Jason Cawley -

Markov Volatility Random Walks

Markov Volatility Random Walks

Jason Cawley -

Asset Allocation

Asset Allocation

Jason Cawley -

Mean-Reverting Random Walks

Mean-Reverting Random Walks

Jason Cawley -

An Amoeba Problem

An Amoeba Problem

Jason Cawley -

Totalistic K3 R 1/2 Cellular Automata

Totalistic K3 R 1/2 Cellular Automata

Jason Cawley -

Cellular Automaton Model of Pine Savanna Dynamics in Response to Fire and Hurricanes

Cellular Automaton Model of Pine Savanna Dynamics in Response to Fire and Hurricanes

Jason Cawley