Employer Health Insurance Choices under H.R.3590 and H.R.3962

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

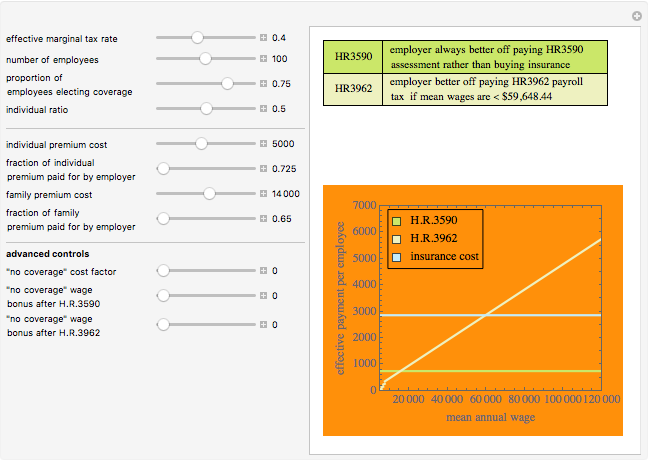

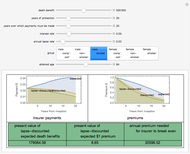

Healthcare reform bills pending in the United States Congress in 2009 generally force employers either to provide health insurance for their employees or pay the government to subsidize the healthcare those employees are nonetheless expected to receive. This Demonstration puts you in the role of an employer and shows the financial consequences of providing health insurance or declining to do so in 2014 and beyond. It does so under the two leading reform contenders: H.R.3590, the Patient Protection and Affordable Care Act (Senate), and H.R.3962, the Affordable Health Care for America Act (House of Representatives). Basically, H.R.3590 requires many employers not providing compliant health insurance to pay an assessment of $750 per employee. H.R.3962 imposes a payroll tax from 2% to 8% on many noncomplying employees.

[more]

Contributed by: Seth J. Chandler (March 2011)

Additional contributions by: Ira Shepard

Open content licensed under CC BY-NC-SA

Snapshots

Details

The model developed here does not consider the proposed addition of section 45R to the Internal Revenue Code that would provide a tax credit to certain small employers for purchasing health insurance on behalf of their employees through one of the "Exchanges" established by the reform bills.

Precisely modeling the indirect costs occasioned when an employer declines to provide health coverage to its employees is difficult. This model assumes that such costs are a user-selectable coefficient multiplied by the difference between the total average premiums the employer would have paid for coverage and any "bonus" the employer chooses to provide the employee after dropping coverage.

The provisions underlying this Demonstration may be found in section 1513 of H.R.3590 and section 512 of H.R.3962.

Although there are many exceptions, health insurance in the United States frequently comes in two "flavors": individual coverage provides health insurance only for the purchaser; family coverage provides health insurance for the purchaser and for certain members of the purchaser's immediate family.

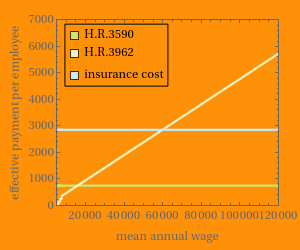

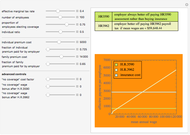

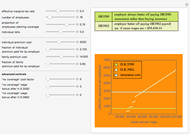

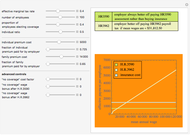

Snapshot 1: the Demonstration in its default settings; these numbers are intended to typify values likely to face employers

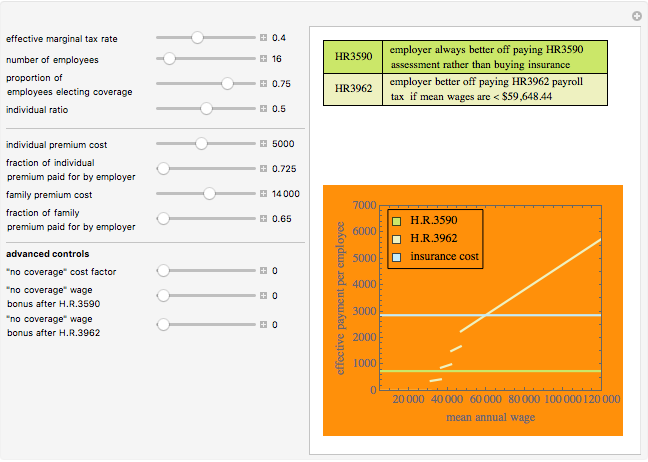

Snapshot 2: the Demonstration in its default settings, except that the number of employees has dropped to 16

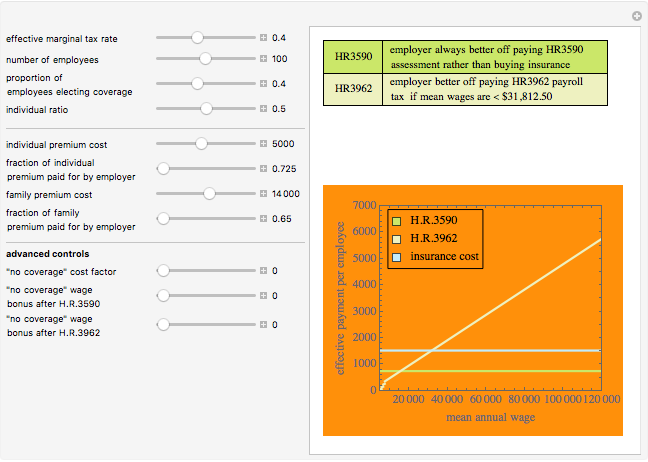

Snapshot 3: the Demonstration in its default settings, except that the proportion of employees electing coverage is assumed to drop to 0.4

Snapshot 4: the Demonstration in its default settings, except that the premiums for individual and family coverage have declined

Snapshot 5: the Demonstration in its default settings, except that the indirect costs of dropping coverage have increased; notice that the employer now does better to purchase insurance under H.R.3590 but still does better under H.R.3962 to drop insurance and pay the payroll tax instead

Snapshot 6: the Demonstration in its default settings, except that the "no coverage" wage bonus under H.R.3590 has increased to $3200; the employer does better dropping coverage and paying the employees $3200 each rather than keep providing health insurance

Permanent Citation

"Employer Health Insurance Choices under H.R.3590 and H.R.3962"

http://demonstrations.wolfram.com/EmployerHealthInsuranceChoicesUnderHR3590AndHR3962/

Wolfram Demonstrations Project

Published: March 7 2011

Individual Insurance Decisions under HR 3560 and HR 3962

Individual Insurance Decisions under HR 3560 and HR 3962

Seth J. Chandler Retiree Stop-Loss Reinsurance

Retiree Stop-Loss Reinsurance

Seth J. Chandler Insurance Disclosures

Insurance Disclosures

Seth J. Chandler Efficient Single Limit Liability Insurance

Efficient Single Limit Liability Insurance

Seth J. Chandler Risk Aversion, Load, and Optimal Insurance

Risk Aversion, Load, and Optimal Insurance

Seth J. Chandler Life Insurance Pricing

Life Insurance Pricing

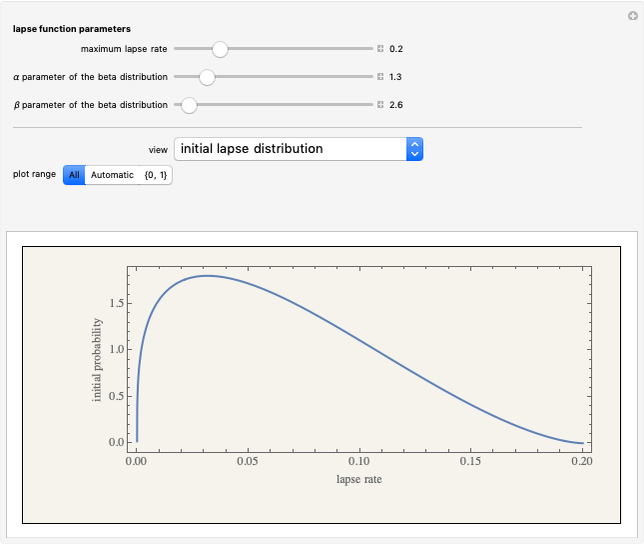

Seth J. Chandler A Theory of Insurance Lapses

A Theory of Insurance Lapses

Seth J. Chandler Coordination of Insurance Policies

Coordination of Insurance Policies

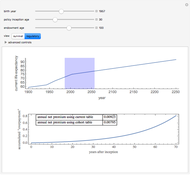

Seth J. Chandler Current versus Cohort Life Tables and the Regulation of Life Insurance

Current versus Cohort Life Tables and the Regulation of Life Insurance

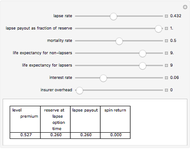

Seth J. Chandler A Conceptual Model of Lapse Financed Life Insurance

A Conceptual Model of Lapse Financed Life Insurance

Seth J. Chandler

-

Post-Event Bonding

Post-Event Bonding

Seth J. Chandler -

Emulating Land Use Evolution with a Cellular Automaton

Emulating Land Use Evolution with a Cellular Automaton

Seth J. Chandler -

General Assembly Resolution Viewer

General Assembly Resolution Viewer

Seth J. Chandler -

Random Acyclic Networks

Random Acyclic Networks

Seth J. Chandler -

A Theory of Insurance Lapses

Seth J. Chandler -

Asylum in the United States

Asylum in the United States

Seth J. Chandler -

Property Coinsurance

Property Coinsurance

Seth J. Chandler -

The Persuasion Effect: A Traditional Two-Stage Jury Model

The Persuasion Effect: A Traditional Two-Stage Jury Model

Seth J. Chandler -

Cellular Automata with Global Control

Cellular Automata with Global Control

Seth J. Chandler -

Sports Seasons Based on Score Distributions

Sports Seasons Based on Score Distributions

Seth J. Chandler -

Evidentiary Uncertainty

Evidentiary Uncertainty

Seth J. Chandler -

Spectral Measures

Spectral Measures

Seth J. Chandler -

The Banzhaf Power Index of States for Presidential Candidates

The Banzhaf Power Index of States for Presidential Candidates

Seth J. Chandler -

Liability Insurance Desirability under Lognormal Loss Distributions

Liability Insurance Desirability under Lognormal Loss Distributions

Seth J. Chandler -

The Effects of Coinsurance and Deductibles on Optimal Precautions for Weibull-Distributed Loss

The Effects of Coinsurance and Deductibles on Optimal Precautions for Weibull-Distributed Loss

Seth J. Chandler -

Collocation by Chi Square

Collocation by Chi Square

Seth J. Chandler -

The Present Value of Future Gas Use

The Present Value of Future Gas Use

Seth J. Chandler -

Visualizing Legal Rules: A Homicide Case

Visualizing Legal Rules: A Homicide Case

Seth J. Chandler -

Communities of Nations Bridged by Language Similarity

Communities of Nations Bridged by Language Similarity

Seth J. Chandler