Implied and Local Volatility Dynamics in the SABR Model

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

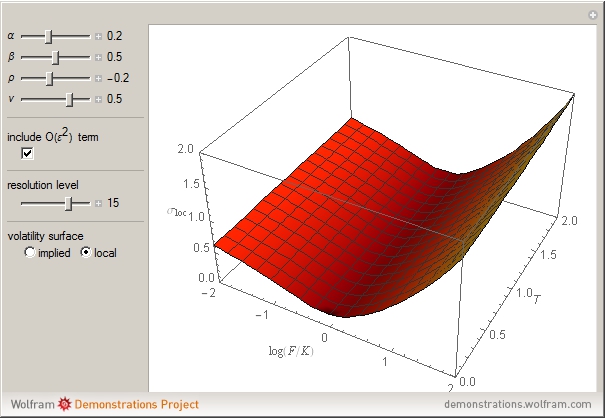

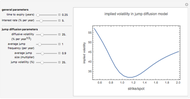

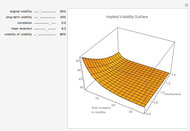

The stochastic (SABR) model [1] provides a parsimonious parametrization of the implied volatility surface, based on a singular perturbation series of a particularly simple stochastic volatility model. The popularity of the SABR model is mainly due to its overwhelming empirical success, but also because it is extraordinary easy to calibrate. In this Demonstration, the asymptotic refinements of [3] are used. The local volatility surface is calculated exactly along the famous Dupire equation [2] in terms of implied volatility.

(SABR) model [1] provides a parsimonious parametrization of the implied volatility surface, based on a singular perturbation series of a particularly simple stochastic volatility model. The popularity of the SABR model is mainly due to its overwhelming empirical success, but also because it is extraordinary easy to calibrate. In this Demonstration, the asymptotic refinements of [3] are used. The local volatility surface is calculated exactly along the famous Dupire equation [2] in terms of implied volatility.

Contributed by: Thomas Mazzoni (August 2011)

Open content licensed under CC BY-NC-SA

Snapshots

Details

The SABR model [1] is based on the simplest possible stochastic volatility model for forward prices

,

,

,

,

under the forward measure, where  and

and  are Brownian motions with

are Brownian motions with  and

and  . In detail,

. In detail,  is the initial volatility,

is the initial volatility,  is the CEV-exponent (CEV stands for constant elasticity of variance),

is the CEV-exponent (CEV stands for constant elasticity of variance),  is the volatility of volatility (volvol), and

is the volatility of volatility (volvol), and  is the correlation between the two sources of random fluctuations.

is the correlation between the two sources of random fluctuations.

Because the SABR model is the result of a perturbation series, there is a term of order  , which may or may not be included. The corrections due to this term are usually about 1%.

, which may or may not be included. The corrections due to this term are usually about 1%.

References

[1] P. S. Hagan, D. Kumar, A. S. Lesniewski, and D. E. Woodward, "Managing Smile Risk," Wilmott Magazine, September 2002 pp. 84–108.

[2] B. Dupire, "Pricing with a Smile," Risk, 7, 1994 pp. 18–20.

[3] J. Oblój, "Fine-Tune Your Smile: Correction to Hagan et al.," Wilmott Magazine, May 2008.

Permanent Citation

Implied Volatility in the Variance Gamma Model

Implied Volatility in the Variance Gamma Model

Andrzej Kozlowski Implied Volatility in Merton's Jump Diffusion Model

Implied Volatility in Merton's Jump Diffusion Model

Peter Falloon Volatility Surface in the Heston Model

Volatility Surface in the Heston Model

Slava Solganik Dynamics in the Solow-Swan Growth Model

Dynamics in the Solow-Swan Growth Model

Richard Foltyn Expected Dynamics of an Imitation Model in 2x2 Symmetric Games

Expected Dynamics of an Imitation Model in 2x2 Symmetric Games

Luis R. Izquierdo and Segismundo S. Izquierdo A Spatial Dynamic Jury Model

A Spatial Dynamic Jury Model

Seth J. Chandler Local Digit Values

Local Digit Values

Michael Schreiber Expected Dynamics of an Imitation Model in the Hawk-Dove Game

Expected Dynamics of an Imitation Model in the Hawk-Dove Game

Luis R. Izquierdo and Segismundo S. Izquierdo A Model of Plasmodium Falciparum Population Dynamics in a Patient during Treatment with Artesunate

A Model of Plasmodium Falciparum Population Dynamics in a Patient during Treatment with Artesunate

Sompob Saralamba Dynamics of a Susceptible-Exposed-Infected-Recovered (SEIR) Epidemic Model with Time Delay

Dynamics of a Susceptible-Exposed-Infected-Recovered (SEIR) Epidemic Model with Time Delay

Clay Gruesbeck