Simultaneity Bias

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

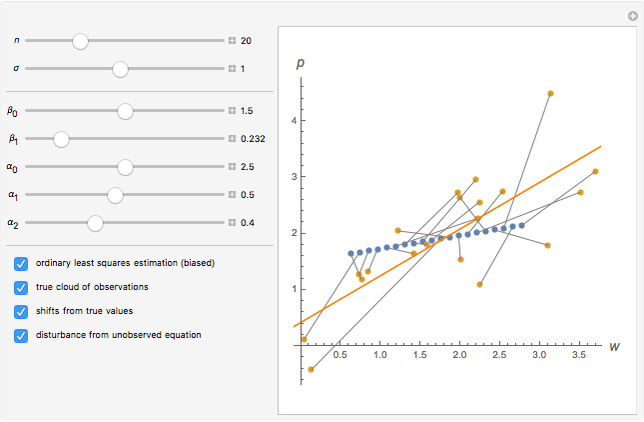

This Demonstration develops the geometric intuition behind the concept of simultaneity bias. We consider a true linear system of simultaneous equations (the index  for each observation is dropped for readability):

for each observation is dropped for readability):

Contributed by: Timur Gareev (May 2018)

Open content licensed under CC BY-NC-SA

Snapshots

Details

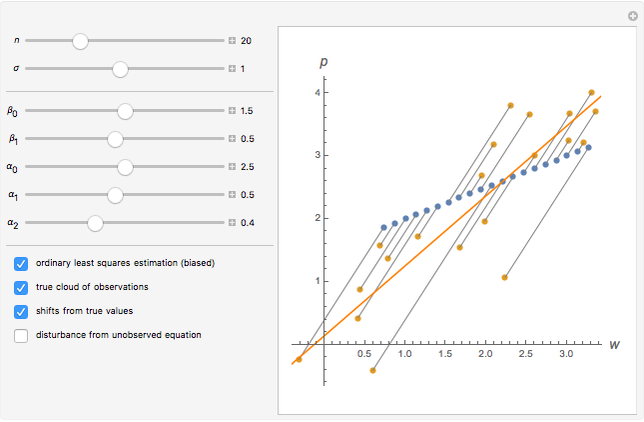

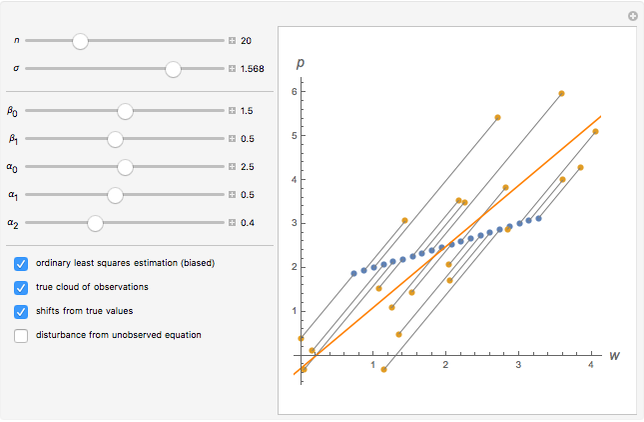

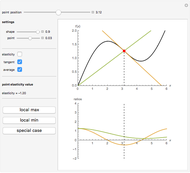

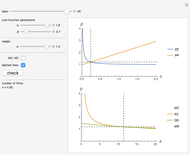

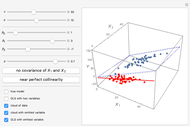

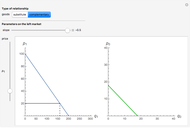

Consider a system of simultaneous equations where each observation gives one point as its solution and which is shifted by error terms. Even if there are many observations, the cloud of points does not allow us to understand the model. In order to identify the relationship between  and

and  (both endogenous variables), we need to have at least one exogenous variable (

(both endogenous variables), we need to have at least one exogenous variable ( in our case), so we simulate several values of . If there are no error terms

in our case), so we simulate several values of . If there are no error terms  and

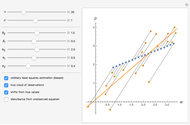

and  in the model, we would get the blue points that reflect the true relationship between and . If the error terms and do not suffer from endogeneity, we could use ordinary least squares to fit the model of the form

in the model, we would get the blue points that reflect the true relationship between and . If the error terms and do not suffer from endogeneity, we could use ordinary least squares to fit the model of the form

.

.

The problem is that such is not the case. To simplify matters and make the visualization more appealing, we keep the error term in the unobserved equation  by default (the bottom checkbox changes this setting).

by default (the bottom checkbox changes this setting).

We may express algebraically in reduced form from the system of simultaneous equations and see that it depends on :

.

.

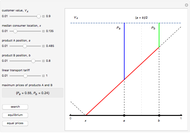

As a result, each observation shifts  to the value of

to the value of  horizontally. At the very same time,

horizontally. At the very same time,  shifts to the value of

shifts to the value of  vertically. Because

vertically. Because  changes from observation to observation randomly, we see such a pattern on the plot:

changes from observation to observation randomly, we see such a pattern on the plot:

.

.

We may divide the vertical to horizontal shift and find the slope of shifts, which is the same for all observations as cancels out. Indeed:

.

.

This effect is shown on the plot. Use the  slider to see the shift effect. Use the checkboxes to turn on and off different plot elements and study their behavior.

slider to see the shift effect. Use the checkboxes to turn on and off different plot elements and study their behavior.

In order to estimate the model, you can use either instrumental variable (IV) or control function (CF) approaches. For instance, can be regressed on , which is a natural instrument for this toy example. In practice, finding and substantiating relevant instruments is a challenging task.

References

[1] Wikipedia. "Endogeneity (Econometrics)." (Mar 30, 2018) en.wikipedia.org/wiki/Endogeneity_(econometrics).

[2] C. Dougherty, Introduction to Econometrics, 5th ed., Oxford, UK: Oxford University Press, 2016 pp. 345–350.

Permanent Citation

Endogeneity Bias

Endogeneity Bias

Timur Gareev Constant Elasticity of Substitution Production

Constant Elasticity of Substitution Production

Kevin Balch and Seth J. Chandler Revenue and Costs Curves Analysis

Revenue and Costs Curves Analysis

Timur Gareev Elasticity Function

Elasticity Function

Timur Gareev Hotelling Model of Product Quality Differentiation

Hotelling Model of Product Quality Differentiation

Timur Gareev Volatility Surface in the Heston Model

Volatility Surface in the Heston Model

Slava Solganik Mean-Reverting Random Walks

Mean-Reverting Random Walks

Jason Cawley Term Structure of Interest Rates

Term Structure of Interest Rates

Roger J. Brown Expected Returns of the Dow Industrials, Beta Model

Expected Returns of the Dow Industrials, Beta Model

Jeff Hamrick and Jason Cawley Expected Returns of the Dow Industrials, Fama-French Model

Expected Returns of the Dow Industrials, Fama-French Model

Jeff Hamrick and Jason Cawley

-

Krugman's Model of Increasing Returns and Monopolistic Competition

Krugman's Model of Increasing Returns and Monopolistic Competition

Timur Gareev -

Returns to Scale in One-Factor Production Functions

Returns to Scale in One-Factor Production Functions

Timur Gareev -

Omitted Variable Bias in 3D

Omitted Variable Bias in 3D

Timur Gareev -

Revenue and Costs Curves Analysis

Timur Gareev -

Leontief Production Function

Leontief Production Function

Timur Gareev -

Simultaneity Bias

Simultaneity Bias

Timur Gareev -

Firm Costs Optimization Problem in Primal and Dual Form

Firm Costs Optimization Problem in Primal and Dual Form

Timur Gareev -

Comparative and Absolute Advantage

Comparative and Absolute Advantage

Timur Gareev -

Firm with Two Plants

Firm with Two Plants

Timur Gareev -

Elasticity Function

Timur Gareev -

Substitute and Complementary Goods

Substitute and Complementary Goods

Timur Gareev -

Monopoly with Two Plants

Monopoly with Two Plants

Timur Gareev -

Best Response in Static Two-Player Games

Best Response in Static Two-Player Games

Timur Gareev -

Hotelling Model of Product Quality Differentiation

Timur Gareev -

Endogeneity Bias

Timur Gareev -

Discriminating Monopolist with Two Independent Markets

Discriminating Monopolist with Two Independent Markets

Timur Gareev -

Monopsony in the Labor Market

Monopsony in the Labor Market

Timur Gareev -

Nondiscriminating Monopolist with Two Independent Markets

Nondiscriminating Monopolist with Two Independent Markets

Timur Gareev -

Supply Curve from Piecewise Linear Cost Function

Supply Curve from Piecewise Linear Cost Function

Timur Gareev -

Duopoly Model in 3D

Duopoly Model in 3D

Timur Gareev