Two-Asset Markowitz Feasible Set

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

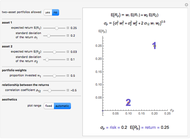

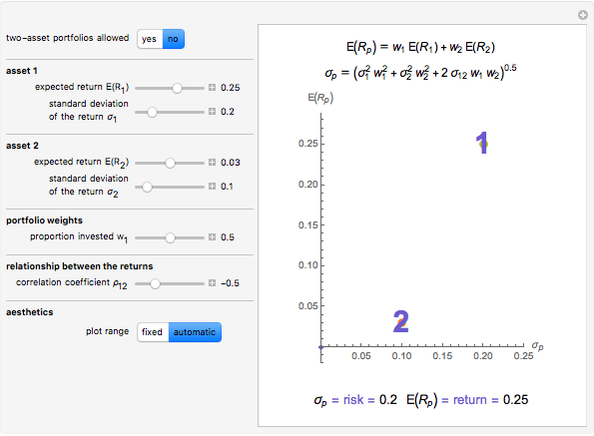

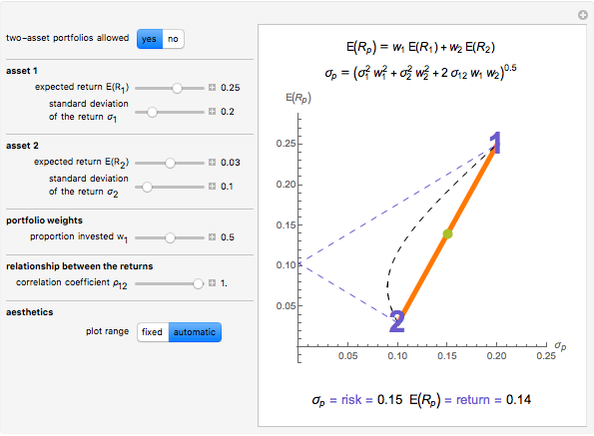

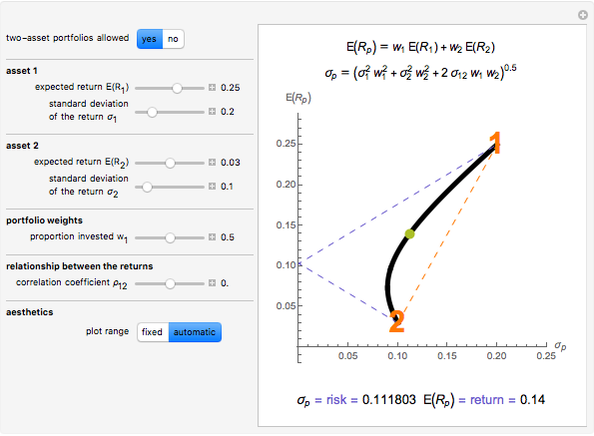

Set the "two-asset portfolios allowed" toggle to "yes" to visualize the relationship between risk and expected return for two-asset portfolios, for varying levels of expected return and risk for the two individual assets, and of the correlation between their returns.

Contributed by: Jim R Larkin (March 2011)

Open content licensed under CC BY-NC-SA

Snapshots

Details

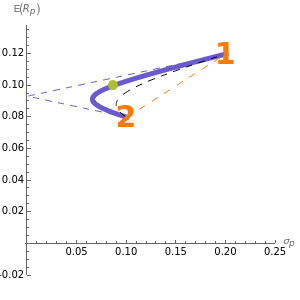

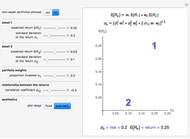

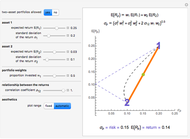

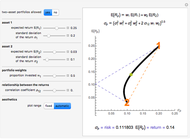

The loci of all possible two-asset portfolio risk and return combinations is called the two-asset feasible set. For two risky assets the orange straight dashed line shows the two-asset feasible set for the case of perfect positive correlation; the black dashed curve shows the two-asset feasible set for the case of zero correlation; and the two slate blue dashed line segments show the two-asset feasible set for the case of perfect negative correlation. The thick blue line shows the actual two-asset feasible set given the actual selection for the (Pearson) correlation coefficient, while the green ball shows the actual risk-return combination given the actual proportion invested in asset 1. The Demonstration does not allow for short selling of any asset. When the "two-asset portfolios allowed" toggle is set to "no" a proportion invested in asset 1 exceeding (or falling short of) 0.50 is treated as 100% invested in asset 1 (or 2).

Permanent Citation

"Two-Asset Markowitz Feasible Set"

http://demonstrations.wolfram.com/TwoAssetMarkowitzFeasibleSet/

Wolfram Demonstrations Project

Published: March 7 2011

Three-Asset Efficient Frontier

Three-Asset Efficient Frontier

Fiona Maclachlan Brownian Motion Path and Maximum Drawdown

Brownian Motion Path and Maximum Drawdown

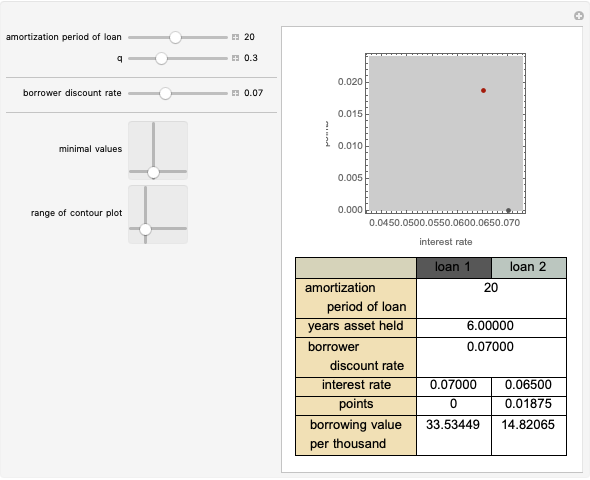

Neil Chriss Pay the Points?

Pay the Points?

Seth J. Chandler Fund Drawdown Simulation

Fund Drawdown Simulation

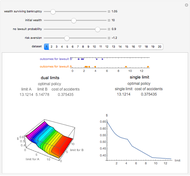

Joe O'Hara The Efficient Dual-Limit Liability Insurance Contract

The Efficient Dual-Limit Liability Insurance Contract

Seth J. Chandler Property Coinsurance

Property Coinsurance

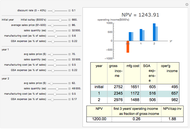

Seth J. Chandler NPV and its Contributions

NPV and its Contributions

Joe O'Hara Efficient Single Limit Liability Insurance

Efficient Single Limit Liability Insurance

Seth J. Chandler Investment Leverage Effect

Investment Leverage Effect

Michael Schreiber Valuation and Management of Bonds

Valuation and Management of Bonds

Charles N. Bagley (University of Massachusetts at Amherst)