Bubbles in a Simple Behavioral Finance Model

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

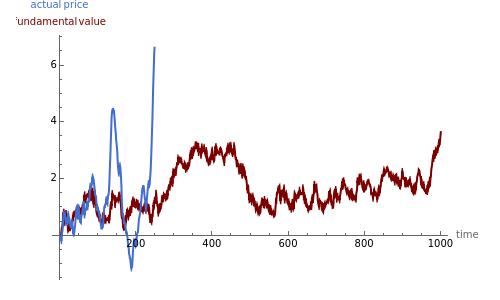

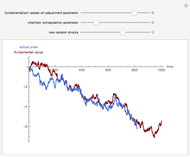

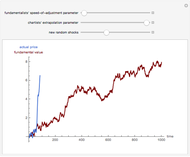

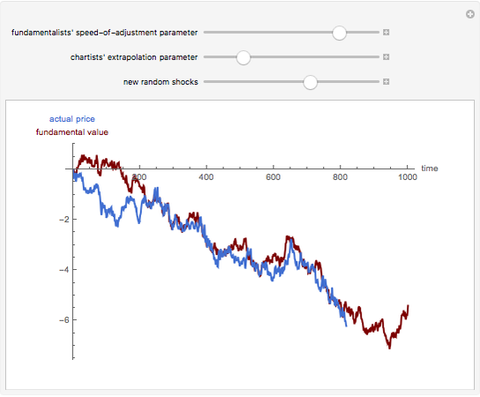

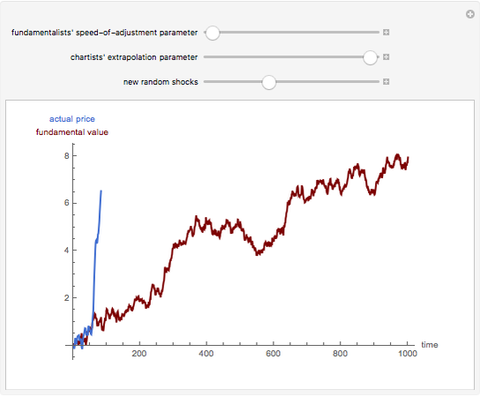

Suppose participants in a financial market adopt either a "fundamentalist" or "chartist" trading strategy based on the historical, risk-adjusted profitability of each strategy. Fundamentalists bet that price will adjust (at a speed determined by the "speed-of-adjustment parameter") towards a value justified by economic fundamentals (the "fundamental value", assumed to follow a random walk). Chartists bet that price will follow its historical trend, such that a percentage (determined by the "extrapolation parameter") of the previous period's price movement will occur again. This Demonstration shows how deviations of price from fundamental value ("bubbles") are affected by the parameters of the trading strategy and the stochastic nature of the model.

Contributed by: Kevin W. Capehart (March 2011)

After work by: Paul De Grauwe and Marianna Grimaldi

Open content licensed under CC BY-NC-SA

Snapshots

Details

See De Grauwe and Grimaldi (2006) for a detailed discussion of the model implemented here, as well as many extensions to it.

P. De Grauwe and M. Grimaldi, The Exchange Rate in a Behavioral Finance Framework, Princeton, NY and Oxford, UK: Princeton University Press, 2006.

Permanent Citation

"Bubbles in a Simple Behavioral Finance Model"

http://demonstrations.wolfram.com/BubblesInASimpleBehavioralFinanceModel/

Wolfram Demonstrations Project

Published: March 7 2011

The Paradox of Thrift in a Simple Stock-Flow Consistent Model

The Paradox of Thrift in a Simple Stock-Flow Consistent Model

Kevin W. Capehart Explaining Real Estate Price Bubbles

Explaining Real Estate Price Bubbles

Roger J. Brown The Hazards of Propping Up: Bubbles and Chaos

The Hazards of Propping Up: Bubbles and Chaos

Philip Maymin Option Prices in Merton's Jump Diffusion Model

Option Prices in Merton's Jump Diffusion Model

Peter Falloon Implied Volatility in Merton's Jump Diffusion Model

Implied Volatility in Merton's Jump Diffusion Model

Peter Falloon Barrier Option Pricing within the Black-Scholes Model

Barrier Option Pricing within the Black-Scholes Model

Peter Falloon Distribution of Returns from Merton's Jump Diffusion Model

Distribution of Returns from Merton's Jump Diffusion Model

Peter Falloon Pricing Power Options in the Black-Scholes Model

Pricing Power Options in the Black-Scholes Model

Peter Falloon Minimal Model of Simulating Prices of Financial Securities Using an Iterated Finite Automaton

Minimal Model of Simulating Prices of Financial Securities Using an Iterated Finite Automaton

Philip Maymin Exploring Minimal Models of the Complexity of Security Prices

Exploring Minimal Models of the Complexity of Security Prices

Philip Maymin