Autoregressive Moving-Average Generator

Initializing live version

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

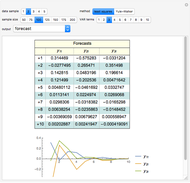

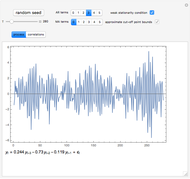

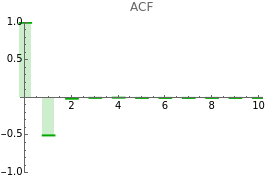

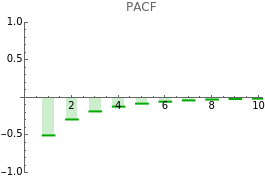

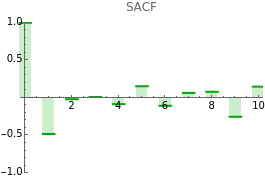

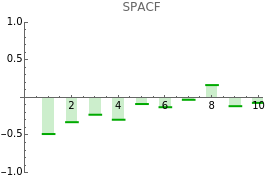

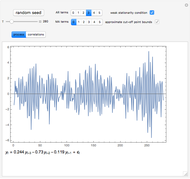

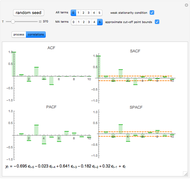

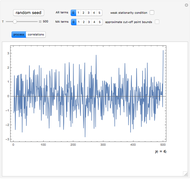

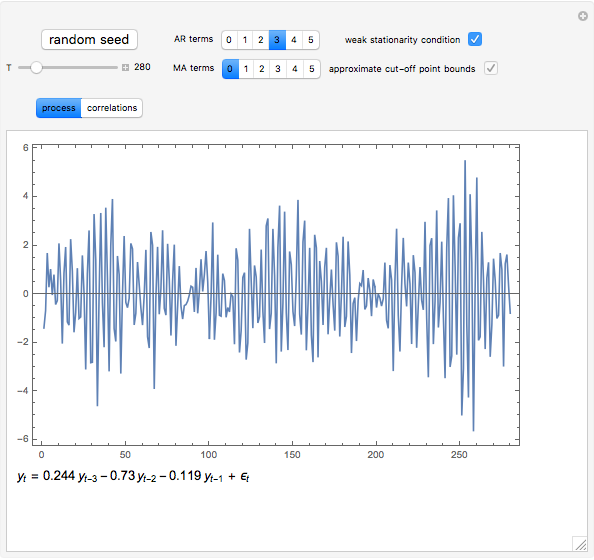

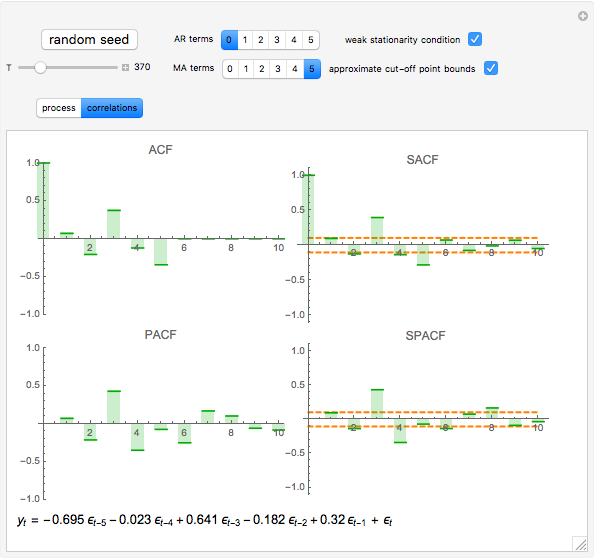

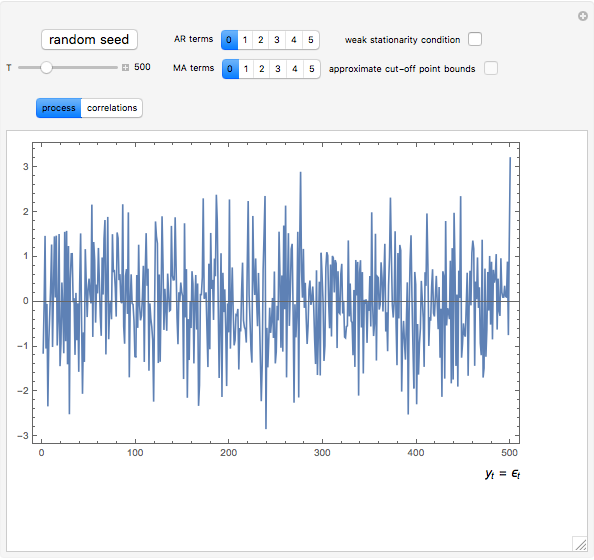

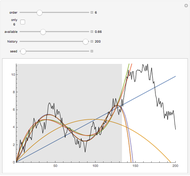

The autoregressive moving-average process (ARMA) is a discrete-time and continuous-state random process. This generator randomly chooses parameters of the model from the interval  ; you can set the condition for (weak) stationarity.

; you can set the condition for (weak) stationarity.

Contributed by: Matus Baniar (June 2013)

Open content licensed under CC BY-NC-SA

Snapshots

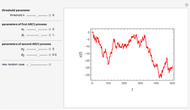

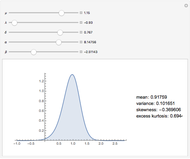

Details

.

.

References

[1] T. Cipra, Finanční ekonometrie, Praha, Czech Republic: Ekopress, 2008.

[2] Z. Prášková, Základy náhodných procesů II, Praha, Czech Republic: Karolinum, 2004.

Permanent Citation

Related Demonstrations

More by Author

Autoregressive Moving-Average Simulation (First Order)

Autoregressive Moving-Average Simulation (First Order)

David von Seggern (University of Nevada) Auto-Regressive Simulation (Second-Order)

Auto-Regressive Simulation (Second-Order)

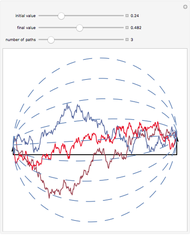

David von Seggern (University of Nevada) Two Jump Diffusion Processes

Two Jump Diffusion Processes

Andrzej Kozlowski The Return Distribution of the Variance Gamma Process

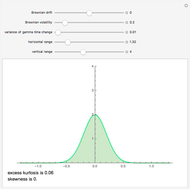

The Return Distribution of the Variance Gamma Process

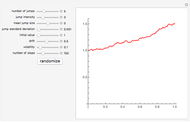

Andrzej Kozlowski Merton's Jump Diffusion Model

Merton's Jump Diffusion Model

Andrzej Kozlowski Brownian Bridge

Brownian Bridge

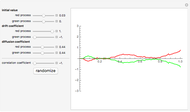

Andrzej Kozlowski Correlated Wiener Processes

Correlated Wiener Processes

Andrzej Kozlowski Polynomial Fits of Random Walks

Polynomial Fits of Random Walks

Michael Schreiber Two-Regime Threshold Autoregressive Model Simulation

Two-Regime Threshold Autoregressive Model Simulation

Jozef Barunik Generalized Hyperbolic Distribution

Generalized Hyperbolic Distribution

Andrzej Kozlowski