Dollar Duration

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

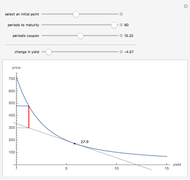

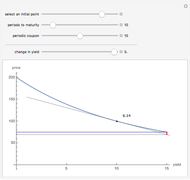

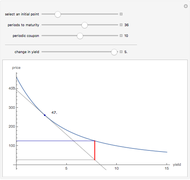

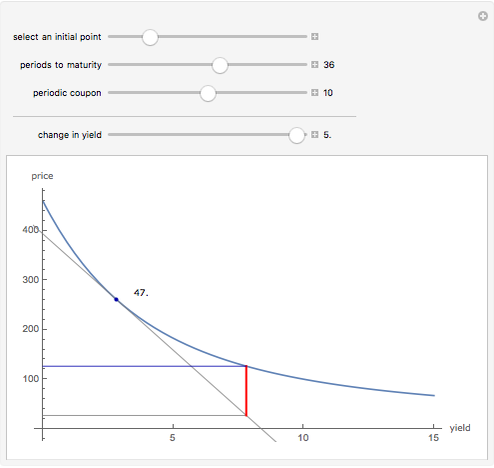

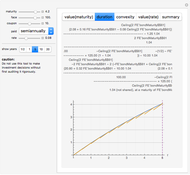

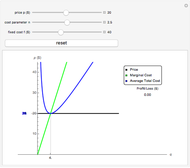

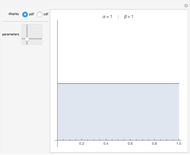

Dollar duration is the first derivative of the price-yield relationship. It is used to approximate the change in the price of a fixed-income security in response to a change in the yield. For example, a dollar duration of 6.14 says that a change in the yield of one percentage point (or 100 basis points) would lead to a change of approximately $6.14 in the price of $100 of face value. The red vertical line indicates the amount of error in the approximation. The amount of error varies with the convexity (i.e., the second derivative) of the price-yield relationship, which in turn varies with the coupon and the time to maturity.

Contributed by: Fiona Maclachlan (March 2011)

Open content licensed under CC BY-NC-SA

Snapshots

Details

In this Demonstration, the maturity, coupon, and yield are all expressed in periodic, rather than annual, terms. The yield and price are expressed in percentage terms. A related measure, DV01 (dollar value of a basis point), approximates the change in the price in response to a one basis point change in the yield. DV01 is also known as PVBP, for present value of a basis point.

Permanent Citation

"Dollar Duration"

http://demonstrations.wolfram.com/DollarDuration/

Wolfram Demonstrations Project

Published: March 7 2011

Macaulay Duration

Macaulay Duration

Fiona Maclachlan Price-Yield Curve

Price-Yield Curve

Fiona Maclachlan Amortized Loan Interest and Principal

Amortized Loan Interest and Principal

Fiona Maclachlan Valuation and Management of Bonds

Valuation and Management of Bonds

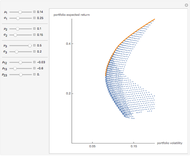

Charles N. Bagley (University of Massachusetts at Amherst) Three-Asset Efficient Frontier

Three-Asset Efficient Frontier

Fiona Maclachlan Profit Maximization in Perfect Competition

Profit Maximization in Perfect Competition

Fiona Maclachlan A Model of Market Shares I

A Model of Market Shares I

Fiona Maclachlan Gains from Trade

Gains from Trade

Fiona Maclachlan Interest Rate Swap

Interest Rate Swap

Fiona Maclachlan Binomial Option Pricing Model

Binomial Option Pricing Model

Fiona Maclachlan

-

Zipf's Law for U.S. Cities

Zipf's Law for U.S. Cities

Fiona Maclachlan -

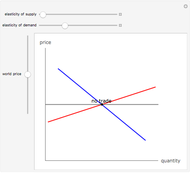

How Continuous Innovation Affects Supply, Producer Surplus, and Consumer Surplus

How Continuous Innovation Affects Supply, Producer Surplus, and Consumer Surplus

Fiona Maclachlan -

Monopoly Model

Monopoly Model

Fiona Maclachlan -

Competitive Model

Competitive Model

Fiona Maclachlan -

Simple Solow Model

Simple Solow Model

Fiona Maclachlan -

Zipf's Law for Cities

Zipf's Law for Cities

Fiona Maclachlan -

Money Supply Process

Money Supply Process

Fiona Maclachlan -

A Model of Market Shares I

Fiona Maclachlan -

Macaulay Duration

Fiona Maclachlan -

Gains from Trade

Fiona Maclachlan -

Broken Stick Rule

Broken Stick Rule

Fiona Maclachlan -

Amortized Loan Interest and Principal

Fiona Maclachlan -

Interest Rate Swap

Fiona Maclachlan -

Elasticity, Total Revenue, and the Linear Demand Curve

Elasticity, Total Revenue, and the Linear Demand Curve

Fiona Maclachlan -

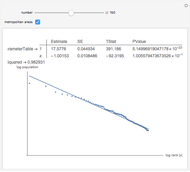

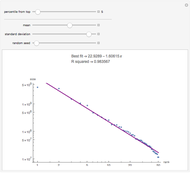

Power Law Tails in Log Normal Data

Power Law Tails in Log Normal Data

Fiona Maclachlan -

Concentric Circles

Concentric Circles

Fiona Maclachlan -

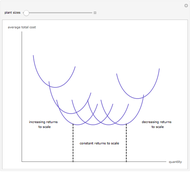

Long-Run Average Total Cost

Long-Run Average Total Cost

Fiona Maclachlan -

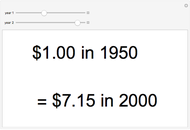

Purchasing Power Calculator

Purchasing Power Calculator

Fiona Maclachlan -

Three-Asset Efficient Frontier

Fiona Maclachlan -

Beta Distribution

Beta Distribution

Fiona Maclachlan