Power Law Tails in Log Normal Data

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

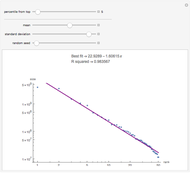

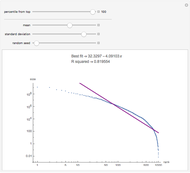

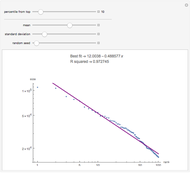

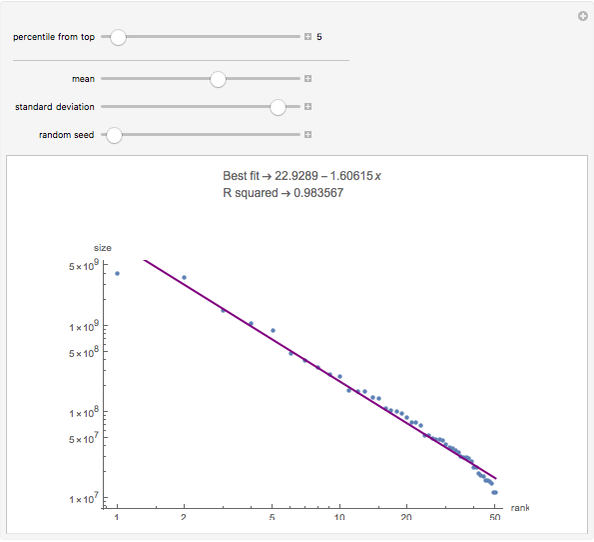

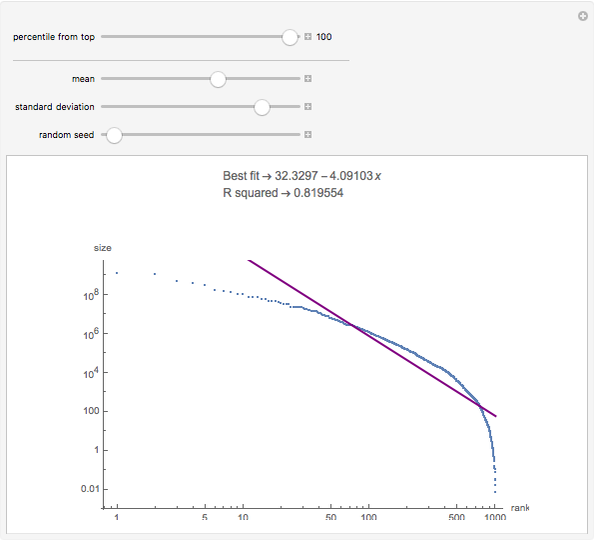

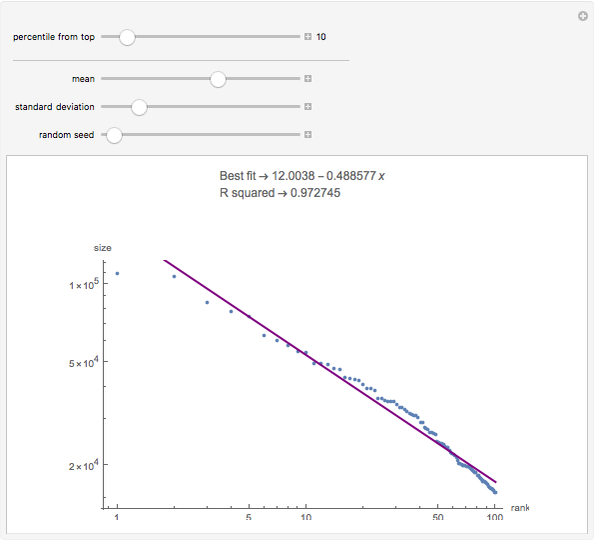

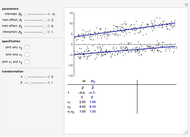

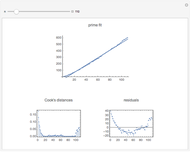

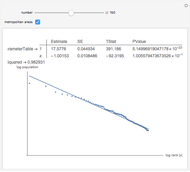

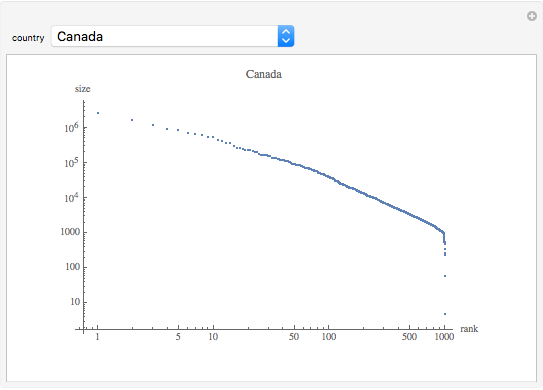

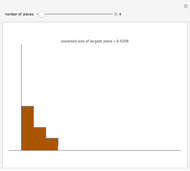

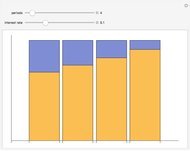

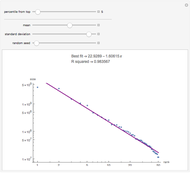

Empirical distributions of magnitudes such as income, wealth, and firm size are often characterized as lognormal with power law upper tails. This Demonstration illustrates how the upper tail of lognormally distributed data can appear to conform to a power law. A thousand random points from a lognormal distribution are generated and the log of the size is regressed on the log of the rank. If only the top percentiles of points are included in the regression, R-squareds of over 0.98 are not uncommon.

Contributed by: Fiona Maclachlan (March 2011)

Open content licensed under CC BY-NC-SA

Snapshots

Details

detailSectionParagraphPermanent Citation

"Power Law Tails in Log Normal Data"

http://demonstrations.wolfram.com/PowerLawTailsInLogNormalData/

Wolfram Demonstrations Project

Published: March 7 2011

Tail Conditional Expectations

Tail Conditional Expectations

Seth J. Chandler Zipf's Law for Natural Languages

Zipf's Law for Natural Languages

Giovanna Roda Stock Price Probability with Stable Distributions

Stock Price Probability with Stable Distributions

Bob Rimmer Estimating Insurance Premiums Using Exceedance Data and the Method of Moments

Estimating Insurance Premiums Using Exceedance Data and the Method of Moments

Seth J. Chandler Estimating Loss Functions Using Exceedance Data and the Method of Moments

Estimating Loss Functions Using Exceedance Data and the Method of Moments

Seth J. Chandler Benford's Law and Data Spread

Benford's Law and Data Spread

Stan Wagon (Macalester College) Multiplicative Interactions

Multiplicative Interactions

Alrik Thiem Fitting Primes to a Linear Model

Fitting Primes to a Linear Model

Darren Glosemeyer Influential Points in Regression

Influential Points in Regression

Ian McLeod Statistical Mechanics of Money

Statistical Mechanics of Money

Ian Wright

-

Zipf's Law for U.S. Cities

Zipf's Law for U.S. Cities

Fiona Maclachlan -

How Continuous Innovation Affects Supply, Producer Surplus, and Consumer Surplus

How Continuous Innovation Affects Supply, Producer Surplus, and Consumer Surplus

Fiona Maclachlan -

Monopoly Model

Monopoly Model

Fiona Maclachlan -

Competitive Model

Competitive Model

Fiona Maclachlan -

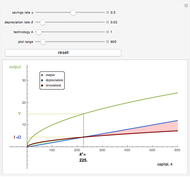

Simple Solow Model

Simple Solow Model

Fiona Maclachlan -

Zipf's Law for Cities

Zipf's Law for Cities

Fiona Maclachlan -

Money Supply Process

Money Supply Process

Fiona Maclachlan -

A Model of Market Shares I

A Model of Market Shares I

Fiona Maclachlan -

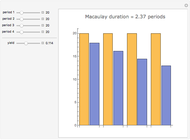

Macaulay Duration

Macaulay Duration

Fiona Maclachlan -

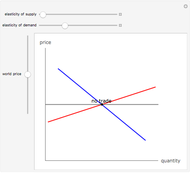

Gains from Trade

Gains from Trade

Fiona Maclachlan -

Broken Stick Rule

Broken Stick Rule

Fiona Maclachlan -

Amortized Loan Interest and Principal

Amortized Loan Interest and Principal

Fiona Maclachlan -

Interest Rate Swap

Interest Rate Swap

Fiona Maclachlan -

Elasticity, Total Revenue, and the Linear Demand Curve

Elasticity, Total Revenue, and the Linear Demand Curve

Fiona Maclachlan -

Power Law Tails in Log Normal Data

Power Law Tails in Log Normal Data

Fiona Maclachlan -

Concentric Circles

Concentric Circles

Fiona Maclachlan -

Long-Run Average Total Cost

Long-Run Average Total Cost

Fiona Maclachlan -

Purchasing Power Calculator

Purchasing Power Calculator

Fiona Maclachlan -

Three-Asset Efficient Frontier

Three-Asset Efficient Frontier

Fiona Maclachlan -

Beta Distribution

Beta Distribution

Fiona Maclachlan