Bivariate First-Order Vector Autoregression Model with Correlated Random Shocks

Initializing live version

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

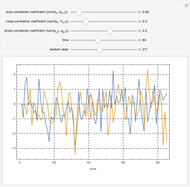

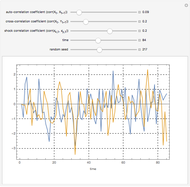

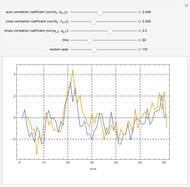

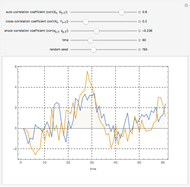

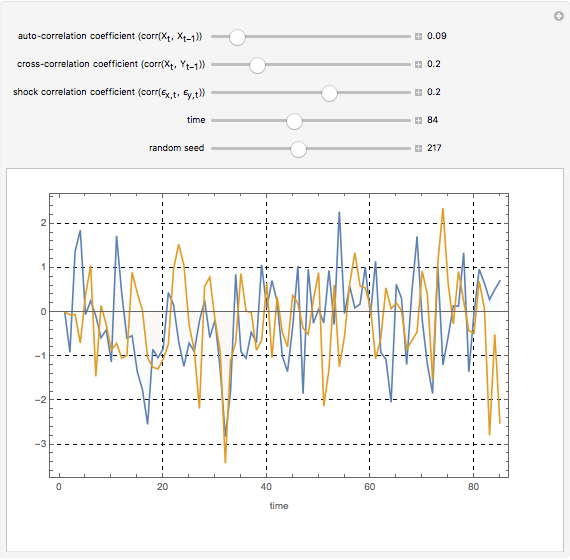

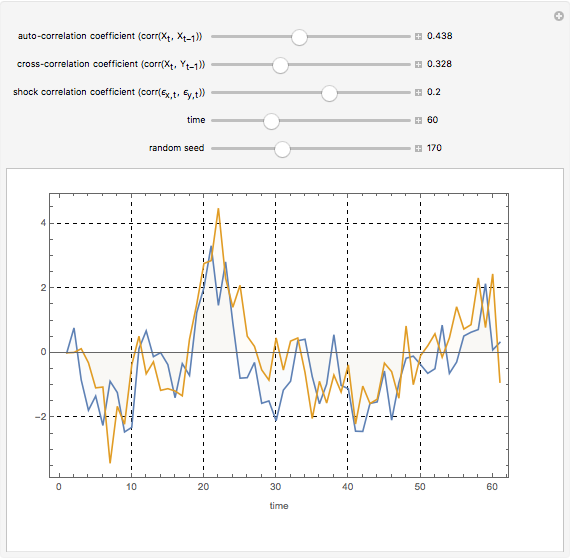

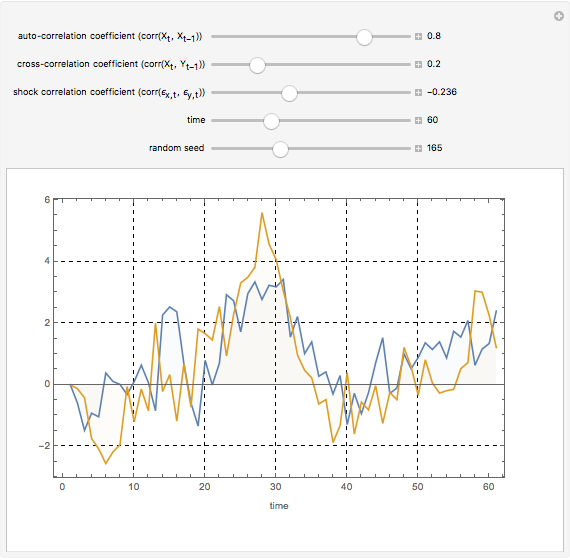

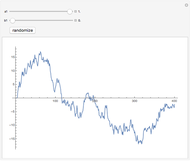

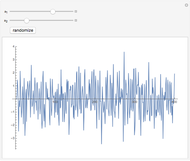

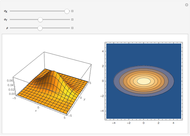

This Demonstration generates and visualizes a bivariate first-order vector autoregression (VAR) model with a symmetric coefficient matrix and correlated random shocks.

[more]

Contributed by: N. Baris Vardar (January 2013)

Paris School of Economics, Université Paris, 1 Panthéon Sorbonne

Open content licensed under CC BY-NC-SA

Snapshots

Details

detailSectionParagraph

Related Demonstrations

More by Author

Autoregressive Moving-Average Simulation (First Order)

Autoregressive Moving-Average Simulation (First Order)

David von Seggern (University of Nevada) Auto-Regressive Simulation (Second-Order)

Auto-Regressive Simulation (Second-Order)

David von Seggern (University of Nevada) Correlation and Regression Explorer

Correlation and Regression Explorer

Ian McLeod (The University of Western Ontario) Goodness of Fit for Random Subsets

Goodness of Fit for Random Subsets

Michael Rogers (Oxford College of Emory University) Estimating and Diagnostic Checking in Censored Normal Random Samples

Estimating and Diagnostic Checking in Censored Normal Random Samples

Nagham Muslim Mohammad and Ian McLeod Joint Density of Bivariate Gaussian Random Variables

Joint Density of Bivariate Gaussian Random Variables

John M. Shea Two-Regime Threshold Autoregressive Model Simulation

Two-Regime Threshold Autoregressive Model Simulation

Jozef Barunik Correlation and Covariance of Random Discrete Signals

Correlation and Covariance of Random Discrete Signals

Daniel de Souza Carvalho The Bivariate Normal Distribution

The Bivariate Normal Distribution

Chris Boucher The Bivariate Normal and Conditional Distributions

The Bivariate Normal and Conditional Distributions

Chris Boucher