Bond Pricing

Initializing live version

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

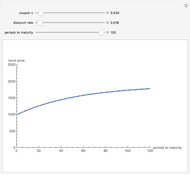

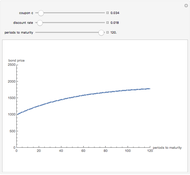

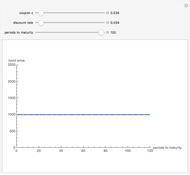

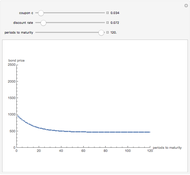

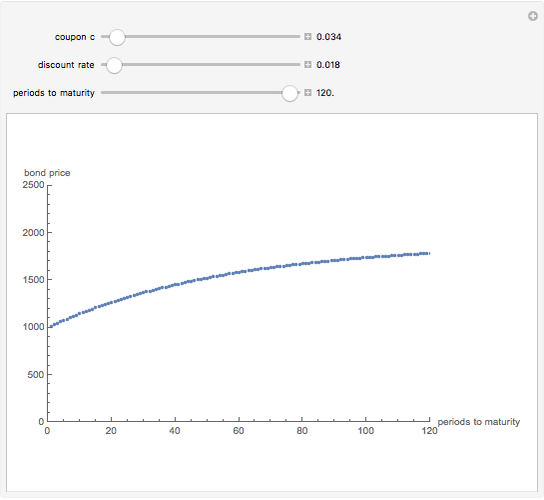

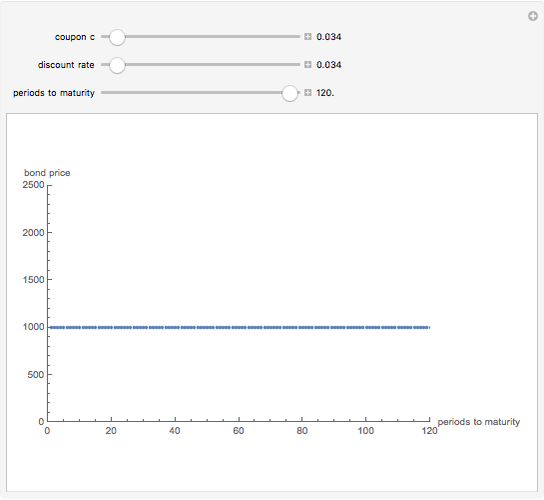

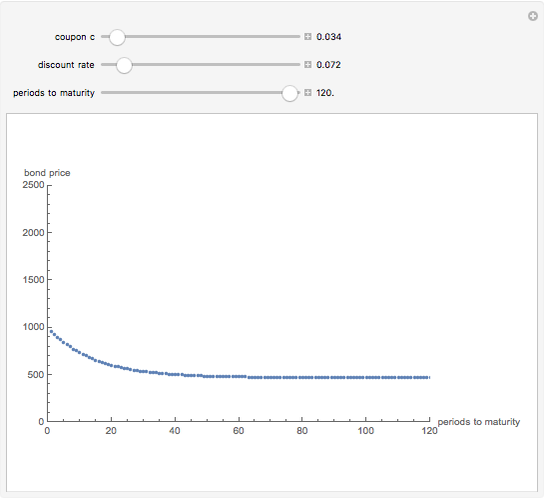

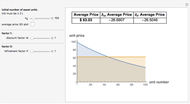

See how the price of a bond with a face value of 1000 changes by manipulating the discount rate, the coupon (as percentage of face value), and the number of coupon payments prior to maturity.

Contributed by: Frederic Erler (March 2011)

Open content licensed under CC BY-NC-SA

Snapshots

Details

detailSectionParagraphPermanent Citation

"Bond Pricing"

http://demonstrations.wolfram.com/BondPricing/

Wolfram Demonstrations Project

Published: March 7 2011

Related Demonstrations

More by Author

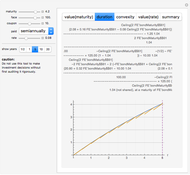

Determinants of the NPV of a Bond

Determinants of the NPV of a Bond

Thomas Lindner Price-Yield Curve

Price-Yield Curve

Fiona Maclachlan Valuation and Management of Bonds

Valuation and Management of Bonds

Charles N. Bagley (University of Massachusetts at Amherst) TARP Toxic (Illiquid) Assets Pricing Model

TARP Toxic (Illiquid) Assets Pricing Model

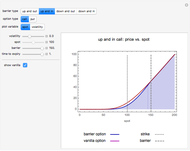

Phil Kongtcheu Barrier Option Pricing within the Black-Scholes Model

Barrier Option Pricing within the Black-Scholes Model

Peter Falloon Explaining Real Estate Price Bubbles

Explaining Real Estate Price Bubbles

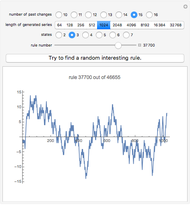

Roger J. Brown Exploring Minimal Models of the Complexity of Security Prices

Exploring Minimal Models of the Complexity of Security Prices

Philip Maymin Minimal Model of Simulating Prices of Financial Securities Using an Iterated Finite Automaton

Minimal Model of Simulating Prices of Financial Securities Using an Iterated Finite Automaton

Philip Maymin Post-Event Bonding

Post-Event Bonding

Seth J. Chandler Pricing Power Options in the Black-Scholes Model

Pricing Power Options in the Black-Scholes Model

Peter Falloon