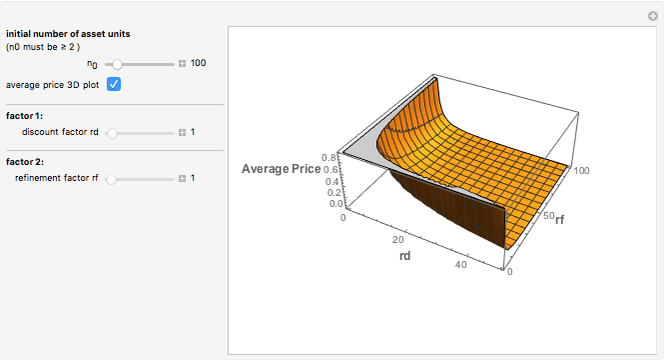

TARP Toxic (Illiquid) Assets Pricing Model

Initializing live version

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

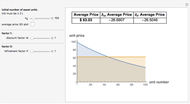

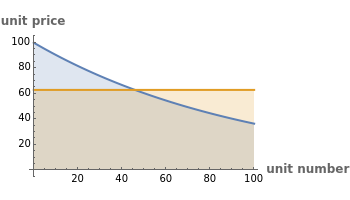

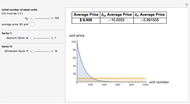

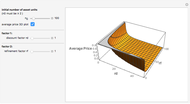

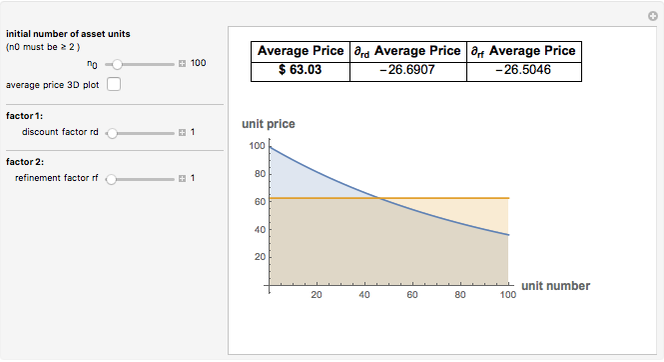

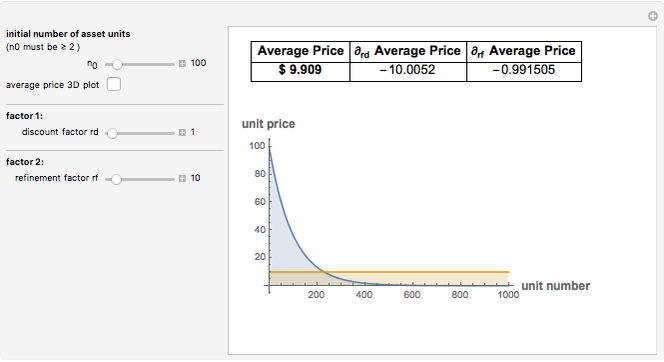

This Demonstration illustrates the influence of the parameters  and

and  on the fair pricing of illiquid assets in a market‐making approach.

on the fair pricing of illiquid assets in a market‐making approach.

Contributed by: Phil Kongtcheu (March 2009)

Open content licensed under CC BY-NC-SA

Snapshots

Details

Related article available at: Fair Value Pricing, Government Market Making and PPIP.

Permanent Citation

Related Demonstrations

More by Author

Asset Allocation

Asset Allocation

Jason Cawley Barrier Option Pricing within the Black-Scholes Model

Barrier Option Pricing within the Black-Scholes Model

Peter Falloon Bond Pricing

Bond Pricing

Frederic Erler Minimal Model of Simulating Prices of Financial Securities Using an Iterated Finite Automaton

Minimal Model of Simulating Prices of Financial Securities Using an Iterated Finite Automaton

Philip Maymin Exploring Minimal Models of the Complexity of Security Prices

Exploring Minimal Models of the Complexity of Security Prices

Philip Maymin Expected Returns of the Dow Industrials, Beta Model

Expected Returns of the Dow Industrials, Beta Model

Jeff Hamrick and Jason Cawley Expected Returns of the Dow Industrials, Fama-French Model

Expected Returns of the Dow Industrials, Fama-French Model

Jeff Hamrick and Jason Cawley Cobweb Model

Cobweb Model

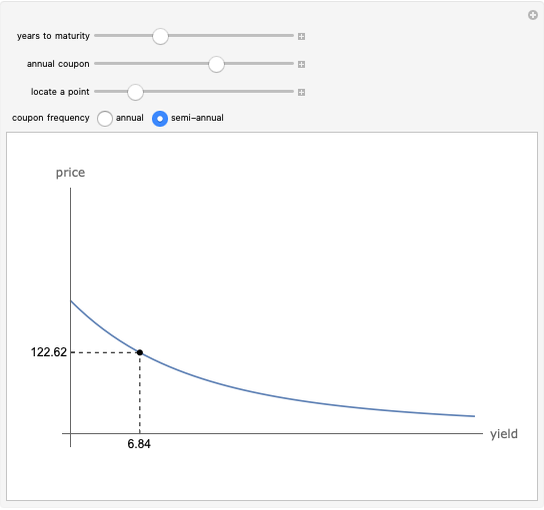

Samuel G. Chen Price-Yield Curve

Price-Yield Curve

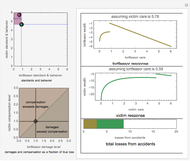

Fiona Maclachlan Bilateral Accident Model

Bilateral Accident Model

Seth J. Chandler