A Conceptual Model of Lapse Financed Life Insurance

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

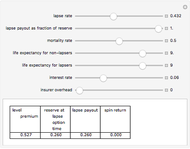

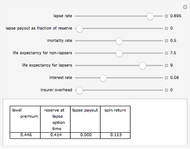

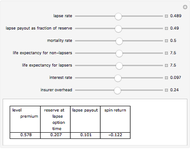

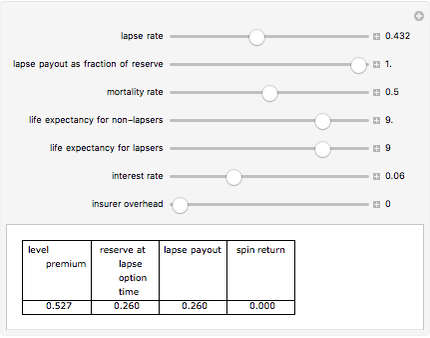

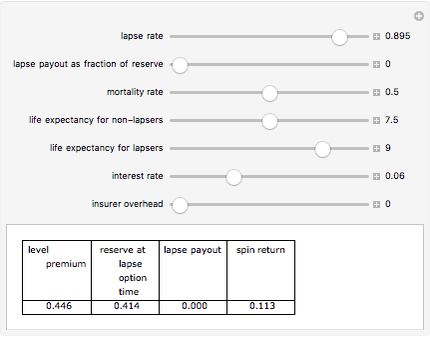

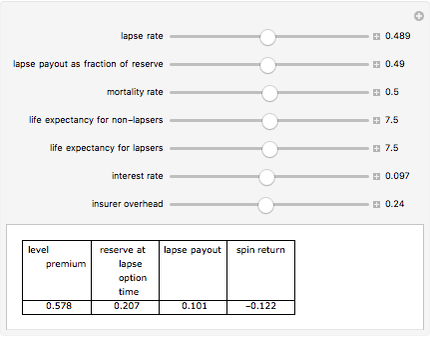

Life insurance premiums on multi-premium policies that provide policyholders an option of lapsing without recourse can be reduced if insurers fail to give lapsing policyholders 100% of the "reserve" for that policy —the excess of the expected present value of future death benefits over the expected present value of future premiums. A failure to provide the full reserve value means that, absent transaction costs, owners of life insurance who know to a certainty that they will not let the policy lapse can actually make a potentially large expected profit. They – rather than their estate – can realize a portion of this expected profit by trading ownership of the policy for cash to investors who diversify much of the risk away through similar transactions and whose greater liquidity may reduce the risk of lapse. This variant of a "life settlement" is known as "Spin Life." This Demonstration illustrates conceptually the relationship among premiums, mortality rates, and anticipated interest rates in long-term life insurance. It further shows the profits theoretically available through "Spin Life." The Demonstration allows users to set expected lifespans among lapsing and non-lapsing policyholders, as well as overhead charges on the purchase of insurance.

Contributed by: Seth J. Chandler (March 2011)

Open content licensed under CC BY-NC-SA

Snapshots

Details

The Demonstration is based on a two-step model in which some policyholders die during the first period and the remaining policyholders either lapse or live for some time thereafter. The expected life span varies depending on whether the policyholder lapses or not: in the real world, lapsing policyholders tend to have longer expected life spans than non-lapsing policyholders. Mathematica computes the premium needed to break even based on the user's choices as to the lapse rate, the fraction of the reserve paid to lapsing policyholders, the percentage of policyholders dying during the first period, the expected life span of lapsers and non-lapsers, the interest (discount) rate, and the overhead of running the insurance system as a percentage of premium. The Demonstration calculates the level premium needed for the insurer to break even, the size of the reserve at the time living policyholders have the option to lapse, the payout upon lapse, and the return a spin investor could expect to see, i.e., someone purchasing a policy during the first period knowing for sure that, so long as the insured survived, they would not lapse.

When there is no life expectancy differential among lapsers and non-lapsers, spin life fails to make money. Lower payments on lapses coupled with lower overhead can result in low premiums and make spin life very profitable.

Permanent Citation

"A Conceptual Model of Lapse Financed Life Insurance"

http://demonstrations.wolfram.com/AConceptualModelOfLapseFinancedLifeInsurance/

Wolfram Demonstrations Project

Published: March 7 2011

Life Insurance Pricing

Life Insurance Pricing

Seth J. Chandler Efficient Single Limit Liability Insurance

Efficient Single Limit Liability Insurance

Seth J. Chandler Insurance Disclosures

Insurance Disclosures

Seth J. Chandler Coordination of Insurance Policies

Coordination of Insurance Policies

Seth J. Chandler Bilateral Accident Model

Bilateral Accident Model

Seth J. Chandler Property Coinsurance

Property Coinsurance

Seth J. Chandler The 2001 CSO Mortality Tables

The 2001 CSO Mortality Tables

Seth J. Chandler Adverse Selection

Adverse Selection

Seth J. Chandler The Duty to Settle

The Duty to Settle

Seth J. Chandler The Efficient Dual-Limit Liability Insurance Contract

The Efficient Dual-Limit Liability Insurance Contract

Seth J. Chandler

-

Post-Event Bonding

Post-Event Bonding

Seth J. Chandler -

Emulating Land Use Evolution with a Cellular Automaton

Emulating Land Use Evolution with a Cellular Automaton

Seth J. Chandler -

General Assembly Resolution Viewer

General Assembly Resolution Viewer

Seth J. Chandler -

Random Acyclic Networks

Random Acyclic Networks

Seth J. Chandler -

A Theory of Insurance Lapses

A Theory of Insurance Lapses

Seth J. Chandler -

Asylum in the United States

Asylum in the United States

Seth J. Chandler -

Property Coinsurance

Seth J. Chandler -

The Persuasion Effect: A Traditional Two-Stage Jury Model

The Persuasion Effect: A Traditional Two-Stage Jury Model

Seth J. Chandler -

Cellular Automata with Global Control

Cellular Automata with Global Control

Seth J. Chandler -

Sports Seasons Based on Score Distributions

Sports Seasons Based on Score Distributions

Seth J. Chandler -

Evidentiary Uncertainty

Evidentiary Uncertainty

Seth J. Chandler -

Spectral Measures

Spectral Measures

Seth J. Chandler -

The Banzhaf Power Index of States for Presidential Candidates

The Banzhaf Power Index of States for Presidential Candidates

Seth J. Chandler -

Liability Insurance Desirability under Lognormal Loss Distributions

Liability Insurance Desirability under Lognormal Loss Distributions

Seth J. Chandler -

The Effects of Coinsurance and Deductibles on Optimal Precautions for Weibull-Distributed Loss

The Effects of Coinsurance and Deductibles on Optimal Precautions for Weibull-Distributed Loss

Seth J. Chandler -

Collocation by Chi Square

Collocation by Chi Square

Seth J. Chandler -

The Present Value of Future Gas Use

The Present Value of Future Gas Use

Seth J. Chandler -

Visualizing Legal Rules: A Homicide Case

Visualizing Legal Rules: A Homicide Case

Seth J. Chandler -

Communities of Nations Bridged by Language Similarity

Communities of Nations Bridged by Language Similarity

Seth J. Chandler