Post-Event Bonding

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

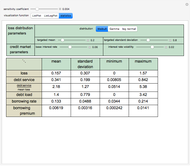

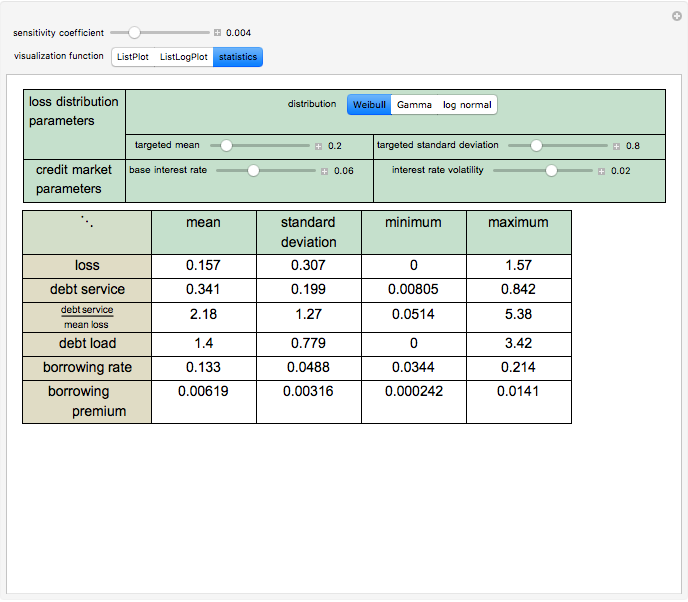

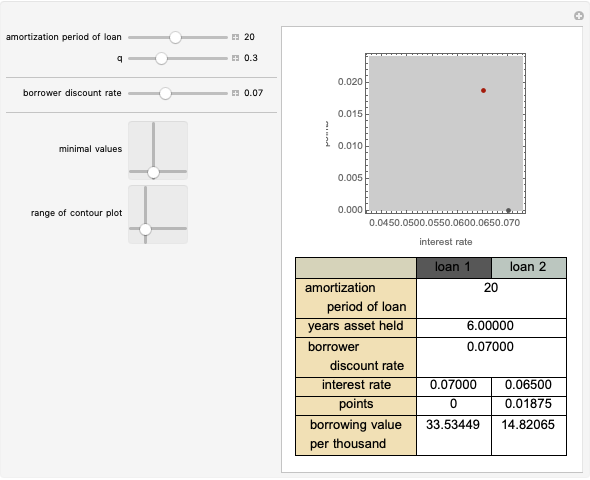

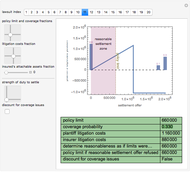

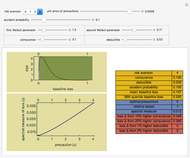

A "post-event bond" is an alternative vehicle for intertemporal spreading of the risk of catastrophic loss. When a loss occurs, an entity such as a government arranges with those in a pool subject to catastrophic loss to issue a bond with a face amount equal to the amount of the loss. The interest rate and amortization period of the bond are likely to depend on the spot market for credit at the time, the size of the loss, and the pre-existing debt load of the borrower. The proceeds from the bond issue are used to pay the losses of the members of the pool. Someone, perhaps the members of the pool, perhaps taxpayers, perhaps others, or some combination of these then pays to amortize the bonds. This Demonstration simulates for 100 years the finances of an entity that annually issues post-event bonds. Each year, a loss is chosen from a random distribution that you specify.

[more]

Contributed by: Seth J. Chandler (March 2011)

Open content licensed under CC BY-NC-SA

Snapshots

Details

Market interest rates follow a random walk in which the starting value is set by the base interest rate and the annual change is normally distributed with the standard deviation you select. The interest rate is clipped to lie between 0.01 and 0.2.

The amortization period of the bonds is determined by the size of the bond issued according to the relationship  , where

, where  is the amortization period and nb is the size of the issue. The code underlying this Demonstration permits you to change this assumption.

is the amortization period and nb is the size of the issue. The code underlying this Demonstration permits you to change this assumption.

The loss distribution function is derived from the mean and standard deviation parameters you provide by using interpolation of precomputed values to deduce the associated scale and shape parameters for the Weibull and Gamma distributions and the associated mean and standard deviation parameters for the lognormal distribution.

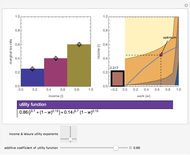

Post-event bonds essentially permit those subject to catastrophe to avoid having to stockpile large amounts of costly capital in order to pay for losses when they occur. This stockpiling can result in high capital costs and thus a high ratio between annual losses and premiums. On the other hand, however, post-event bonds subject those subject to catastrophe to significant interest rate risk. If—either because of prior borrowings to pay for losses or because of market conditions at the time—the post-event bond must be issued, interest rates can be extremely high, again resulting in a high ratio between debt service and annual losses. Careful attention should thus be paid to the volatility and maximum levels of the debt service resulting from the parameters you select. High values for these statistics may, in the real world, create a crushing burden on those who have to pay off the bonds, suggesting the limitations of financing risk with this method.

Snapshot 1: ListLogPlot mode

Snapshot 2: statistics mode

Snapshot 3: high sensitivity of interest rates to the outstanding principal balance on existing bonds

Permanent Citation

"Post-Event Bonding"

http://demonstrations.wolfram.com/PostEventBonding/

Wolfram Demonstrations Project

Published: March 7 2011

Valuation and Management of Bonds

Valuation and Management of Bonds

Charles N. Bagley (University of Massachusetts at Amherst) Efficient Single Limit Liability Insurance

Efficient Single Limit Liability Insurance

Seth J. Chandler The Efficient Dual-Limit Liability Insurance Contract

The Efficient Dual-Limit Liability Insurance Contract

Seth J. Chandler Property Coinsurance

Property Coinsurance

Seth J. Chandler Moral Hazard

Moral Hazard

Seth J. Chandler Certainty Equivalent Wealth

Certainty Equivalent Wealth

Seth J. Chandler Insurance Disclosures

Insurance Disclosures

Seth J. Chandler Pay the Points?

Pay the Points?

Seth J. Chandler The Duty to Settle

The Duty to Settle

Seth J. Chandler Tax Rates and Tax Revenue

Tax Rates and Tax Revenue

Seth J. Chandler

-

Post-Event Bonding

Post-Event Bonding

Seth J. Chandler -

Emulating Land Use Evolution with a Cellular Automaton

Emulating Land Use Evolution with a Cellular Automaton

Seth J. Chandler -

General Assembly Resolution Viewer

General Assembly Resolution Viewer

Seth J. Chandler -

Random Acyclic Networks

Random Acyclic Networks

Seth J. Chandler -

A Theory of Insurance Lapses

A Theory of Insurance Lapses

Seth J. Chandler -

Asylum in the United States

Asylum in the United States

Seth J. Chandler -

Property Coinsurance

Seth J. Chandler -

The Persuasion Effect: A Traditional Two-Stage Jury Model

The Persuasion Effect: A Traditional Two-Stage Jury Model

Seth J. Chandler -

Cellular Automata with Global Control

Cellular Automata with Global Control

Seth J. Chandler -

Sports Seasons Based on Score Distributions

Sports Seasons Based on Score Distributions

Seth J. Chandler -

Evidentiary Uncertainty

Evidentiary Uncertainty

Seth J. Chandler -

Spectral Measures

Spectral Measures

Seth J. Chandler -

The Banzhaf Power Index of States for Presidential Candidates

The Banzhaf Power Index of States for Presidential Candidates

Seth J. Chandler -

Liability Insurance Desirability under Lognormal Loss Distributions

Liability Insurance Desirability under Lognormal Loss Distributions

Seth J. Chandler -

The Effects of Coinsurance and Deductibles on Optimal Precautions for Weibull-Distributed Loss

The Effects of Coinsurance and Deductibles on Optimal Precautions for Weibull-Distributed Loss

Seth J. Chandler -

Collocation by Chi Square

Collocation by Chi Square

Seth J. Chandler -

The Present Value of Future Gas Use

The Present Value of Future Gas Use

Seth J. Chandler -

Visualizing Legal Rules: A Homicide Case

Visualizing Legal Rules: A Homicide Case

Seth J. Chandler -

Communities of Nations Bridged by Language Similarity

Communities of Nations Bridged by Language Similarity

Seth J. Chandler