Expected Utility: Optimal Asset Investment

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

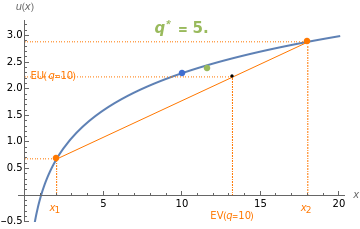

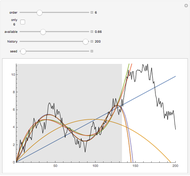

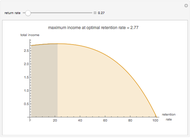

An investor begins with 10 units of wealth that can be invested in a risky asset, or maintained as cash with no return. Assume the risky asset yields a rate of return of  or

or  with probabilities

with probabilities  and

and  , respectively, and let

, respectively, and let  be the number of units of wealth that the investor decides to invest in the asset. The value of the investor's portfolio at the end of the period will be

be the number of units of wealth that the investor decides to invest in the asset. The value of the investor's portfolio at the end of the period will be  . Let the two possible end-of-period values of the portfolio be

. Let the two possible end-of-period values of the portfolio be  and

and  , shown above along the horizontal axis. The Bernoulli logarithmic utility function of wealth (constant relative risk aversion, CRRA) is plotted in blue. The orange line is a plot of the expected value and the corresponding expected utility of the portfolio for different values of

, shown above along the horizontal axis. The Bernoulli logarithmic utility function of wealth (constant relative risk aversion, CRRA) is plotted in blue. The orange line is a plot of the expected value and the corresponding expected utility of the portfolio for different values of  . The optimal portfolio is the one for which the expected utility is a maximum, as shown by the green dot.

. The optimal portfolio is the one for which the expected utility is a maximum, as shown by the green dot.

Contributed by: Loreto Llorente (March 2011)

Open content licensed under CC BY-NC-SA

Snapshots

Details

detailSectionParagraphPermanent Citation

"Expected Utility: Optimal Asset Investment"

http://demonstrations.wolfram.com/ExpectedUtilityOptimalAssetInvestment/

Wolfram Demonstrations Project

Published: March 7 2011

Expected Utility: Optimal Insurance

Expected Utility: Optimal Insurance

Loreto Llorente Investment Leverage Effect

Investment Leverage Effect

Michael Schreiber Constant Risk Aversion Utility Functions

Constant Risk Aversion Utility Functions

Seth J. Chandler Expected Returns of the Dow Industrials, Beta Model

Expected Returns of the Dow Industrials, Beta Model

Jeff Hamrick and Jason Cawley Polynomial Fits of Random Walks

Polynomial Fits of Random Walks

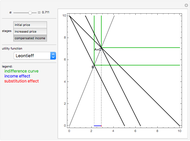

Michael Schreiber Income and Substitution Effects with Different Utility Functions

Income and Substitution Effects with Different Utility Functions

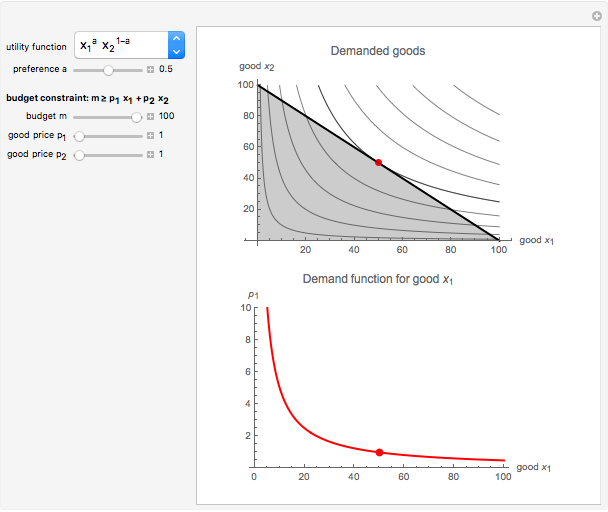

Massimiliano Landi Consumer Demand

Consumer Demand

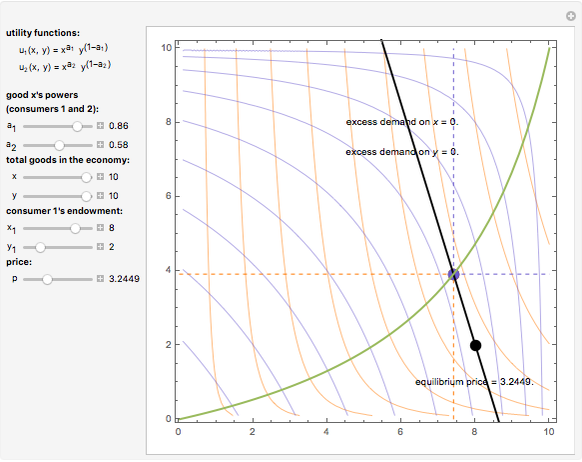

Loreto Llorente Walrasian Equilibrium or Disequilibrium

Walrasian Equilibrium or Disequilibrium

Loreto Llorente How Much Should I Reinvest in a Business?

How Much Should I Reinvest in a Business?

Lucas Tsui Short-Run Production and Cost Curves

Short-Run Production and Cost Curves

Tom Creahan

-

Price Competition

Price Competition

Loreto Llorente -

Principal Becomes an Agent

Principal Becomes an Agent

Loreto Llorente -

Consumer Demand

Loreto Llorente -

Logarithmic Spiral

Logarithmic Spiral

Loreto Llorente -

Expected Utility: Optimal Asset Investment

Expected Utility: Optimal Asset Investment

Loreto Llorente -

Expected Utility: Optimal Insurance

Loreto Llorente -

Walrasian Equilibrium or Disequilibrium

Loreto Llorente