Expected Returns of the Dow Industrials, Beta Model

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

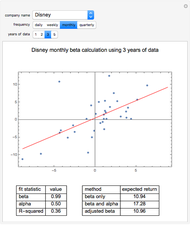

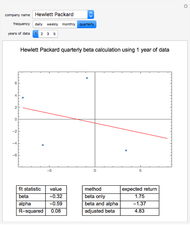

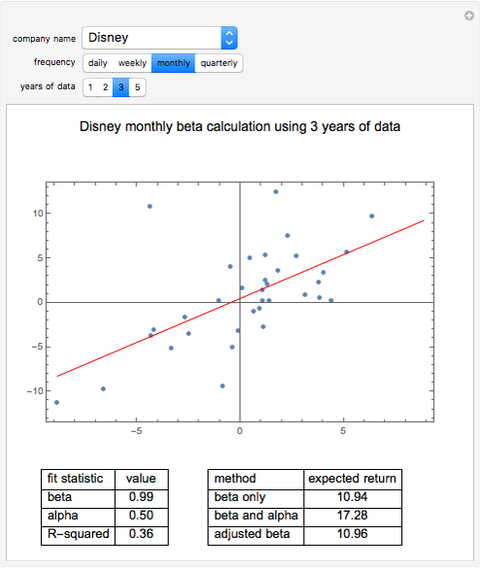

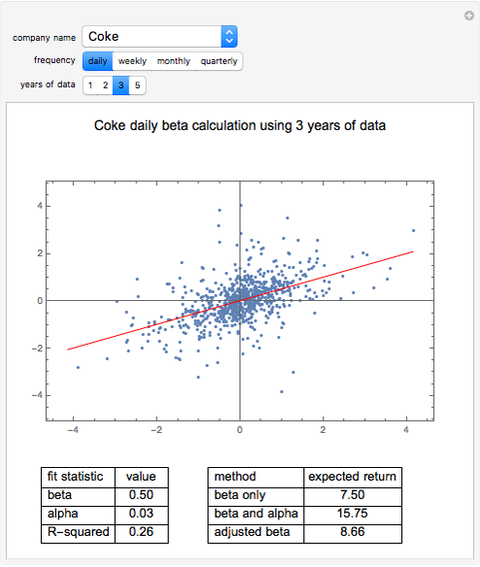

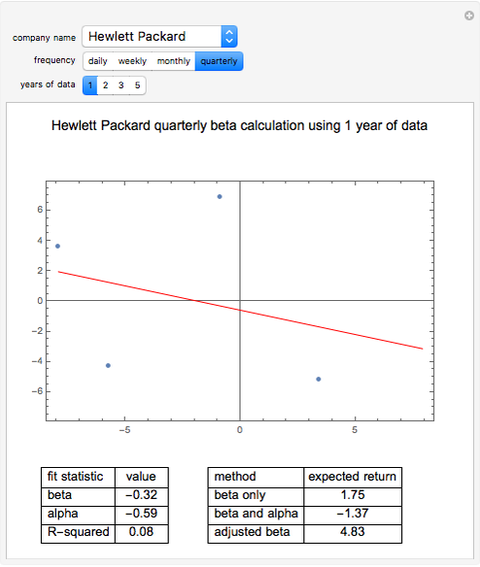

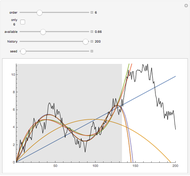

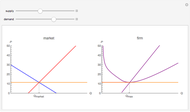

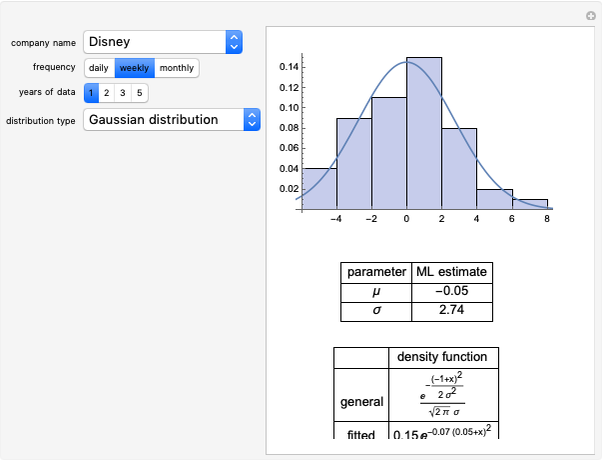

In this Demonstration, we model the expected annual returns of the components of the Dow Jones 30 using the capital asset pricing model (CAPM). We proxy the market returns using the S&P 500 (with dividends reinvested). For the specified return frequency, we display the S&P 500 returns on the  axis and the stock's returns on the

axis and the stock's returns on the  axis and show the best linear fit. The slope of this line is the beta coefficient, and the intercept is the stock's alpha (with respect to the return frequency).

axis and show the best linear fit. The slope of this line is the beta coefficient, and the intercept is the stock's alpha (with respect to the return frequency).

Contributed by: Jeff Hamrick and Jason Cawley (August 2008)

Open content licensed under CC BY-NC-SA

Snapshots

Details

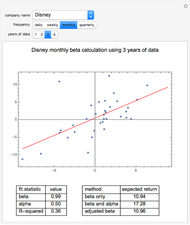

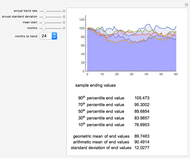

We compute three possible expected returns and display the results in the lower right-hand portion. The expected return computed with beta coefficient only is computed

according to the rule  , where

, where  is the risk-free rate,

is the risk-free rate,  is the sample beta coefficient of stock

is the sample beta coefficient of stock  with respect to the market, and

with respect to the market, and  is the expected future annual return of the market. We assume that the expected future return in the market will be 11%, which has been the long-term average return of the S&P 500. We use a risk-free rate of 4%.

is the expected future annual return of the market. We assume that the expected future return in the market will be 11%, which has been the long-term average return of the S&P 500. We use a risk-free rate of 4%.

To compute the expected return "believing both beta and alpha", we use the rule  , where in this case

, where in this case  is the annualized alpha of the stock . In our analytical framework, a positive

is the annualized alpha of the stock . In our analytical framework, a positive  is generally obtained if the stock outperformed the market over the chosen time period. It is negative if the stock underperformed the market during the chosen time period. If the user partially believes the stock's recent alpha, the user could linearly interpolate the "beta only" and "beta and alpha" results to obtain a partial alpha of sorts.

is generally obtained if the stock outperformed the market over the chosen time period. It is negative if the stock underperformed the market during the chosen time period. If the user partially believes the stock's recent alpha, the user could linearly interpolate the "beta only" and "beta and alpha" results to obtain a partial alpha of sorts.

Sample beta coefficients are notorious for being unstable with respect to: (a) the return frequency used in the analysis; and (b) the particular time window of data used in the analysis. This Demonstration illustrates that instability fairly clearly. Because of this instability, some financial analysts argue that future beta coefficients should be expected to regress to the mean beta coefficient (the beta coefficient of the market with respect to itself, which is one). They instead use an adjusted beta coefficient in their analysis, determined by  , where

, where  is the adjusted beta coefficient of stock and again, is the unadjusted beta coefficient of stock . We then compute another possible expected return according to the rule

is the adjusted beta coefficient of stock and again, is the unadjusted beta coefficient of stock . We then compute another possible expected return according to the rule  .

.

Permanent Citation

Bilateral Accident Model

Bilateral Accident Model

Seth J. Chandler Expected Returns of the Dow Industrials, Fama-French Model

Expected Returns of the Dow Industrials, Fama-French Model

Jeff Hamrick and Jason Cawley A Model of Market Shares II

A Model of Market Shares II

Fiona Maclachlan A Model of Market Shares I

A Model of Market Shares I

Fiona Maclachlan Short-Run Production and Cost Curves

Short-Run Production and Cost Curves

Tom Creahan Investment Leverage Effect

Investment Leverage Effect

Michael Schreiber Polynomial Fits of Random Walks

Polynomial Fits of Random Walks

Michael Schreiber How Much Should I Reinvest in a Business?

How Much Should I Reinvest in a Business?

Lucas Tsui Monopoly Profit-Maximization with Quadratic Marginal Cost

Monopoly Profit-Maximization with Quadratic Marginal Cost

Thomas Mitchell Profit Maximization in Perfect Competition

Profit Maximization in Perfect Competition

Fiona Maclachlan

-

Expected Returns of the Dow Industrials, Beta Model

Expected Returns of the Dow Industrials, Beta Model

Jason Cawley -

Comparing Data on Countries

Comparing Data on Countries

Jason Cawley -

Rank Plots for Countries

Rank Plots for Countries

Jason Cawley -

Country Groups

Country Groups

Jason Cawley -

Country Data and Benford's Law

Country Data and Benford's Law

Jason Cawley -

Cellular Automata with Global Control

Cellular Automata with Global Control

Jason Cawley -

Simulating the 2008 U.S. Presidential Election

Simulating the 2008 U.S. Presidential Election

Jason Cawley -

Exploring Social Choice Theory

Exploring Social Choice Theory

Jason Cawley -

Fully Random, Five-Rule Interactive Cellular Automata (ICA)

Fully Random, Five-Rule Interactive Cellular Automata (ICA)

Jason Cawley -

Algorithmic Architecture with Cellular Automata

Algorithmic Architecture with Cellular Automata

Jason Cawley -

Modeling Return Distributions

Modeling Return Distributions

Jason Cawley -

Expected Returns of the Dow Industrials, Fama-French Model

Jason Cawley -

Credit Risk

Credit Risk

Jason Cawley -

Highlighting Patterns in Cellular Automata

Highlighting Patterns in Cellular Automata

Jason Cawley -

Markov Volatility Random Walks

Markov Volatility Random Walks

Jason Cawley -

Asset Allocation

Asset Allocation

Jason Cawley -

Mean-Reverting Random Walks

Mean-Reverting Random Walks

Jason Cawley -

An Amoeba Problem

An Amoeba Problem

Jason Cawley -

Totalistic K3 R 1/2 Cellular Automata

Totalistic K3 R 1/2 Cellular Automata

Jason Cawley -

Cellular Automaton Model of Pine Savanna Dynamics in Response to Fire and Hurricanes

Cellular Automaton Model of Pine Savanna Dynamics in Response to Fire and Hurricanes

Jason Cawley