Portfolio Diversification Benefit from Subadditive VaR

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

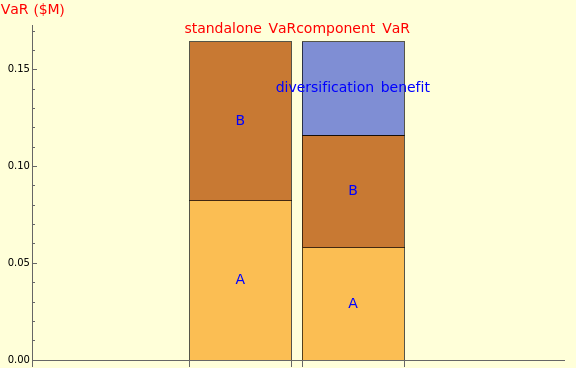

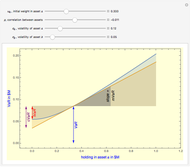

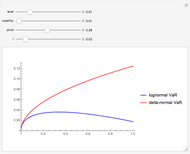

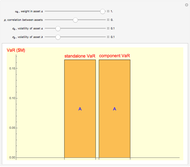

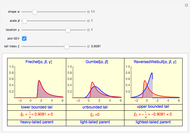

Portfolio diversification benefit derives from investing in various assets whose values do not rise and fall in perfect harmony. Because of this imperfect correlation, the risk of a diversified portfolio is smaller than the weighted average risk of its constituent assets. In term of Value at Risk (VaR), portfolio VaR is smaller than the sum of its constituent VaRs because VaR is a subadditive risk measure:  .

.

Contributed by: Pichet Thiansathaporn (July 2012)

Open content licensed under CC BY-NC-SA

Snapshots

Details

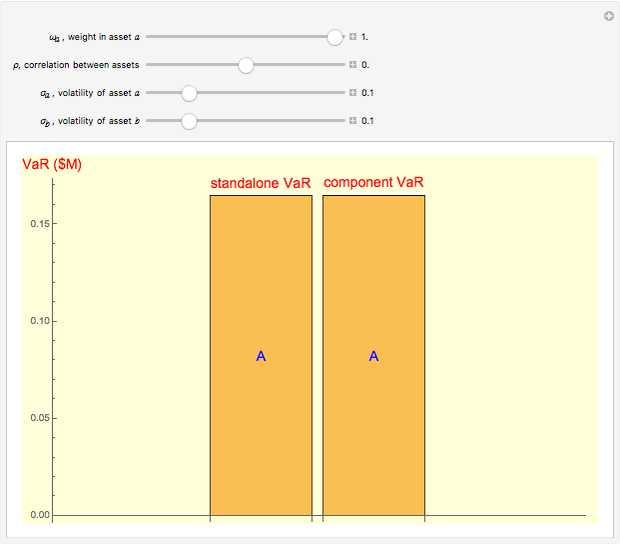

Snapshot 1: when assets are perfectly correlated ( ), there is no diversification benefit and

), there is no diversification benefit and

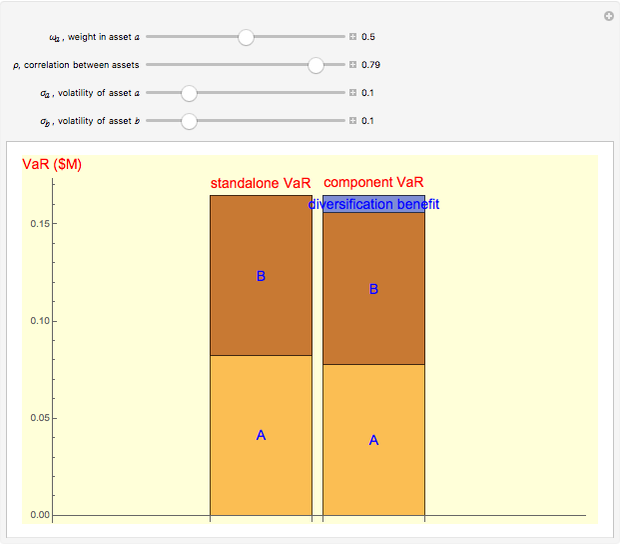

Snapshot 2: when assets are less than perfectly correlated ( ), there is some diversification benefit and

), there is some diversification benefit and

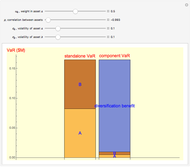

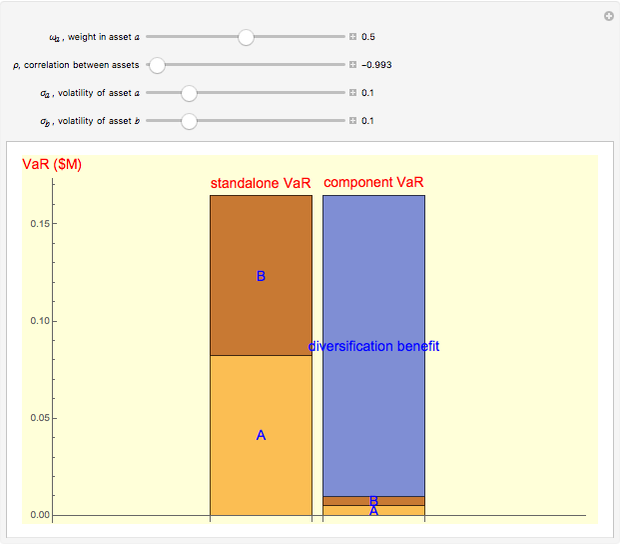

Snapshot 3: when assets are perfectly contrarian ( ), the diversification benefit is maximized

), the diversification benefit is maximized

Snapshot 4: when assets are over concentrated ( or

or  ), the diversification benefit is reduced

), the diversification benefit is reduced

Snapshot 5: assets that are negatively correlated with other assets in the portfolio can serve as a natural hedge, since they contribute negatively to portfolio VaR (i.e. their component VaRs are negative)

Reference

[1] Kevin Dowd, Measuring Market Risk, 2nd ed., West Sussex, England: Wiley, 2005 pp. 271–274.

Permanent Citation

Attributing Portfolio Value at Risk: Relations with Component VaR, Marginal VaR, and Incremental VaR

Attributing Portfolio Value at Risk: Relations with Component VaR, Marginal VaR, and Incremental VaR

Pichet Thiansathaporn VaR Methods

VaR Methods

Dimos Karaflos Using Tensors to Analyze a Large Portfolio of Stocks

Using Tensors to Analyze a Large Portfolio of Stocks

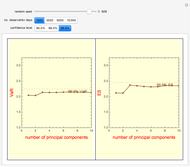

Rick Carey Principal Components Analysis: Application in Value at Risk and Expected Shortfall

Principal Components Analysis: Application in Value at Risk and Expected Shortfall

Pichet Thiansathaporn Estimating the Time between Mishaps from Quality Control Data

Estimating the Time between Mishaps from Quality Control Data

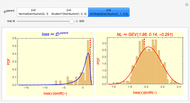

Mark D. Normand and Micha Peleg Generalized Extreme Value Distributions: Application in Financial Risk Management

Generalized Extreme Value Distributions: Application in Financial Risk Management

Pichet Thiansathaporn Kelly Portfolio Analysis

Kelly Portfolio Analysis

Stephen Schulist Krugman's Cost Benefit Analysis for Austerity Cuts in Government Spending

Krugman's Cost Benefit Analysis for Austerity Cuts in Government Spending

Michael Kelly (Finance Consultant) Three-Asset Efficient Frontier

Three-Asset Efficient Frontier

Fiona Maclachlan Gains from Trade

Gains from Trade

Fiona Maclachlan

-

Generalized Extreme Value Distributions: Application in Financial Risk Management

Pichet Thiansathaporn -

Portfolio Diversification Benefit from Subadditive VaR

Portfolio Diversification Benefit from Subadditive VaR

Pichet Thiansathaporn -

Attributing Portfolio Value at Risk: Relations with Component VaR, Marginal VaR, and Incremental VaR

Pichet Thiansathaporn -

Principal Components Analysis: Application in Value at Risk and Expected Shortfall

Pichet Thiansathaporn -

Fisher-Tippett-Gnedenko Theorem: Generalizing Three Types of Extreme Value Distributions

Fisher-Tippett-Gnedenko Theorem: Generalizing Three Types of Extreme Value Distributions

Pichet Thiansathaporn