Bootstrapping to Compute Value-at-Risk Standard Errors

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

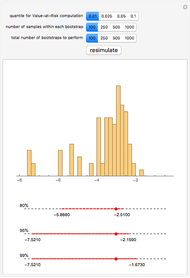

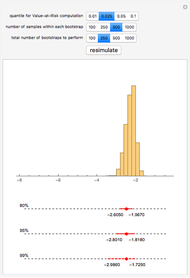

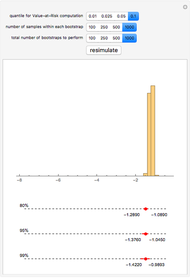

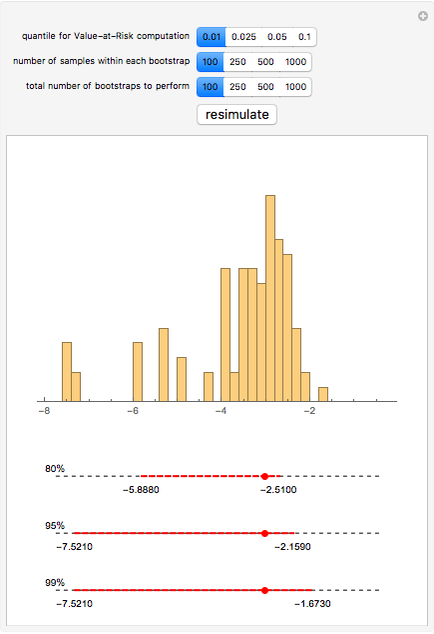

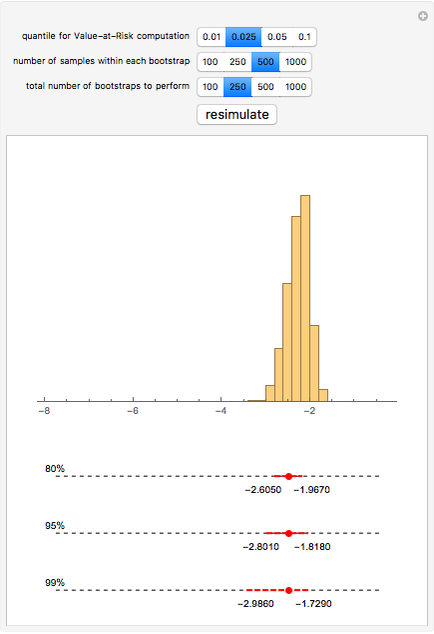

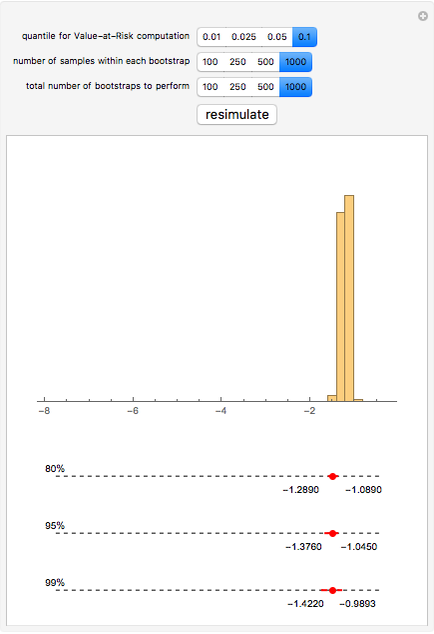

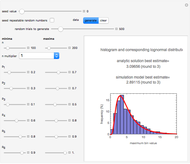

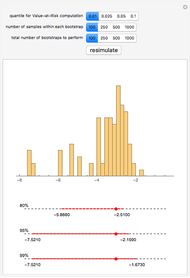

We obtain daily log-return data for the S&P 500 (with dividends reinvested) for the past twenty years, bootstrap low quantiles of the data, and then construct various confidence intervals around those estimated low quantiles. These low quantiles are related to a measure of risk called Value-at-Risk (VaR).

[more]

Contributed by: Jeff Hamrick (March 2011)

Open content licensed under CC BY-NC-SA

Snapshots

Details

In some cases, VaR can be computed analytically—for example, if the portfolio's future value is assumed to be a log-normal random variable. The computation of VaR from historical data is equivalent to calculating a low quantile of the historical data (multiplied, perhaps, against a particular portfolio value to obtain a dollar value rather than a percentage loss figure). The resulting value is taken as an estimate of the true underlying VaR. Unfortunately, the standard errors of such an estimate depend on the underlying (and unknown) distribution of the returns. Bootstrapping is one methodology that is useful for estimating those standard errors.

We show the following output: a histogram of the bootstrapped VaR values for a given input from the user. Additionally, we give 80%, 95%, and 99% bootstrapped confidence intervals around the point estimate of the VaR—the sample quantile of the daily log-return data for the S&P 500. This point estimate is shown as a large red dot.

Permanent Citation

"Bootstrapping to Compute Value-at-Risk Standard Errors"

http://demonstrations.wolfram.com/BootstrappingToComputeValueAtRiskStandardErrors/

Wolfram Demonstrations Project

Published: March 7 2011

Bootstrapping Credit Default Swap Data

Bootstrapping Credit Default Swap Data

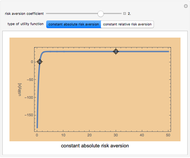

Jeff Hamrick Constant Risk Aversion Utility Functions

Constant Risk Aversion Utility Functions

Seth J. Chandler Risk, Ownership, and Control

Risk, Ownership, and Control

Roger J. Brown Expanded Fermi Solution for Risk Assessment

Expanded Fermi Solution for Risk Assessment

Mark D. Normand, Micha Peleg and Joseph Horowitz Present Value Calculator

Present Value Calculator

Craig Bauling Net Present Value

Net Present Value

Fiona Maclachlan Options: Time Value

Options: Time Value

Peter Falloon Value Added Growth Model

Value Added Growth Model

Roger J. Brown The Value of Tax Deferral

The Value of Tax Deferral

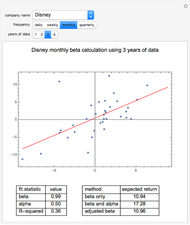

Seth J. Chandler Expected Returns of the Dow Industrials, Fama-French Model

Expected Returns of the Dow Industrials, Fama-French Model

Jeff Hamrick and Jason Cawley

-

Expected Returns of the Dow Industrials, Beta Model

Expected Returns of the Dow Industrials, Beta Model

Jeff Hamrick -

Exploring Measures of Association

Exploring Measures of Association

Jeff Hamrick -

Bootstrapping Credit Default Swap Data

Jeff Hamrick -

Linear Dependence between Two Bernoulli Random Variables

Linear Dependence between Two Bernoulli Random Variables

Jeff Hamrick -

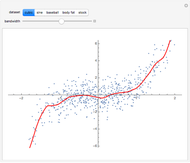

Estimating the Local Mean Function

Estimating the Local Mean Function

Jeff Hamrick -

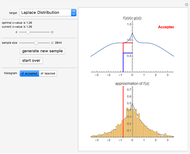

Acceptance/Rejection Sampling

Acceptance/Rejection Sampling

Jeff Hamrick -

Simulating the 2008 U.S. Presidential Election

Simulating the 2008 U.S. Presidential Election

Jeff Hamrick -

The Method of Inverse Transforms

The Method of Inverse Transforms

Jeff Hamrick -

The Perturbed Rat

The Perturbed Rat

Jeff Hamrick -

Modeling Return Distributions

Modeling Return Distributions

Jeff Hamrick -

Pricing a European-Style Arithmetic Asian Option: Comparing Bootstrapping and Simulation Approaches

Pricing a European-Style Arithmetic Asian Option: Comparing Bootstrapping and Simulation Approaches

Jeff Hamrick -

The Method of Common Random Numbers: An Example

The Method of Common Random Numbers: An Example

Jeff Hamrick -

The Envelope Theorem: Numerical Examples

The Envelope Theorem: Numerical Examples

Jeff Hamrick -

Bootstrapping to Compute Value-at-Risk Standard Errors

Bootstrapping to Compute Value-at-Risk Standard Errors

Jeff Hamrick -

Expected Returns of the Dow Industrials, Fama-French Model

Jeff Hamrick -

Kernel Density Estimation

Kernel Density Estimation

Jeff Hamrick -

Simulating Asset Prices with a GARCH(1,1) Model

Simulating Asset Prices with a GARCH(1,1) Model

Jeff Hamrick