Generalized Extreme Value Distributions: Application in Financial Risk Management

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

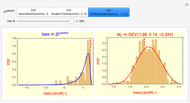

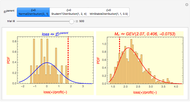

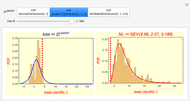

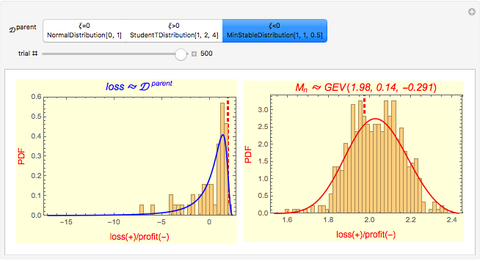

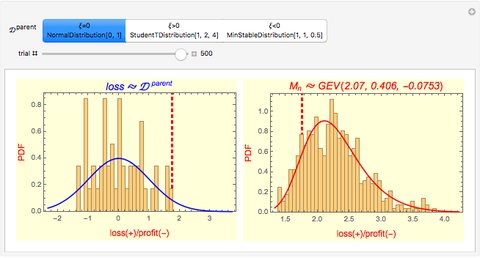

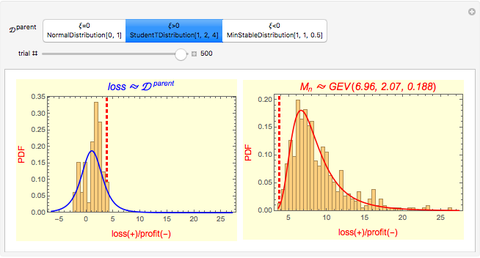

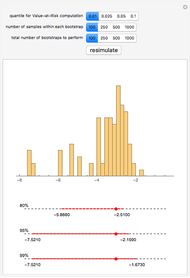

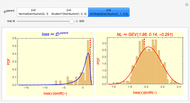

This Demonstration illustrates the Fisher–Tippett–Gnedenko theorem in the context of financial risk management. A sample of  observations is drawn from a parent distribution

observations is drawn from a parent distribution  that describes the probability of historical losses of a portfolio (left-hand plot). A number of draws (

that describes the probability of historical losses of a portfolio (left-hand plot). A number of draws ( ) are repeated to obtain a histogram of 500 maximal losses (

) are repeated to obtain a histogram of 500 maximal losses ( ), shown as a running cumulative in the right-hand plot. At each draw, the position of is marked by a red vertical dashed line.

), shown as a running cumulative in the right-hand plot. At each draw, the position of is marked by a red vertical dashed line.

Contributed by: Pichet Thiansathaporn (February 2013)

Open content licensed under CC BY-NC-SA

Snapshots

Details

Reference

[1] K. Dowd, Measuring Market Risk, 2nd ed., West Sussex, England: Wiley, 2005 pp. 190–194.

Permanent Citation

Principal Components Analysis: Application in Value at Risk and Expected Shortfall

Principal Components Analysis: Application in Value at Risk and Expected Shortfall

Pichet Thiansathaporn Earned Value Management

Earned Value Management

Hagen Lotze Modeling Return Distributions

Modeling Return Distributions

Jeff Hamrick Bootstrapping to Compute Value-at-Risk Standard Errors

Bootstrapping to Compute Value-at-Risk Standard Errors

Jeff Hamrick Attributing Portfolio Value at Risk: Relations with Component VaR, Marginal VaR, and Incremental VaR

Attributing Portfolio Value at Risk: Relations with Component VaR, Marginal VaR, and Incremental VaR

Pichet Thiansathaporn Financial Engineering of a Bond

Financial Engineering of a Bond

Thomas Lindner Risk, Ownership, and Control

Risk, Ownership, and Control

Roger J. Brown Present Value Calculator

Present Value Calculator

Craig Bauling Net Present Value

Net Present Value

Fiona Maclachlan Options: Time Value

Options: Time Value

Peter Falloon

-

Generalized Extreme Value Distributions: Application in Financial Risk Management

Generalized Extreme Value Distributions: Application in Financial Risk Management

Pichet Thiansathaporn -

Portfolio Diversification Benefit from Subadditive VaR

Portfolio Diversification Benefit from Subadditive VaR

Pichet Thiansathaporn -

Attributing Portfolio Value at Risk: Relations with Component VaR, Marginal VaR, and Incremental VaR

Pichet Thiansathaporn -

Principal Components Analysis: Application in Value at Risk and Expected Shortfall

Pichet Thiansathaporn -

Fisher-Tippett-Gnedenko Theorem: Generalizing Three Types of Extreme Value Distributions

Fisher-Tippett-Gnedenko Theorem: Generalizing Three Types of Extreme Value Distributions

Pichet Thiansathaporn