Principal Components Analysis: Application in Value at Risk and Expected Shortfall

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

Principal Component Analysis (PCA) is used in financial risk management to reduce the dimensionality of a multivariate problem, thus creating a simpler representation of the risk factors in the dataset. Only a few judiciously chosen hypothetical variables are needed to explain a large proportion of the variability in the data. These principal components are obtained through the singular value decomposition of the return series.

[more]

Contributed by: Pichet Thiansathaporn (July 2012)

Open content licensed under CC BY-NC-SA

Snapshots

Details

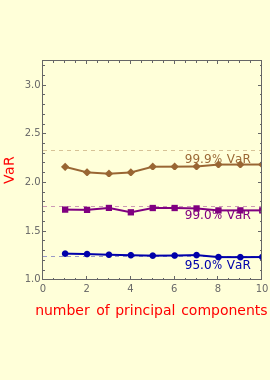

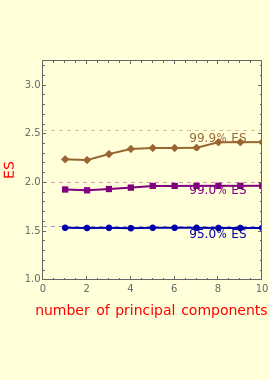

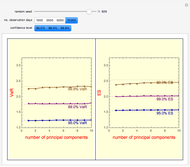

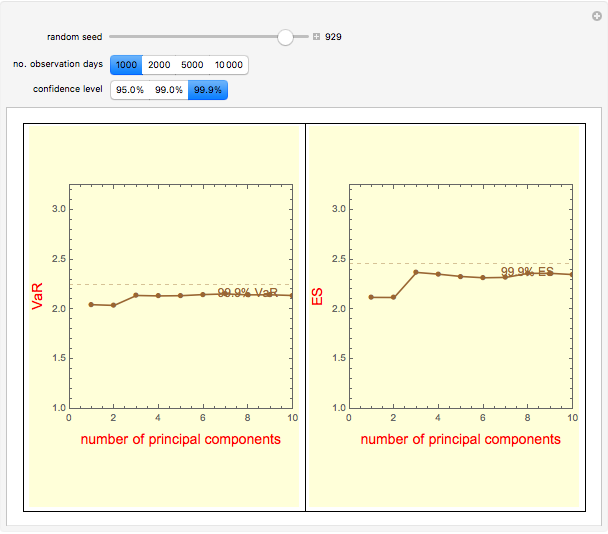

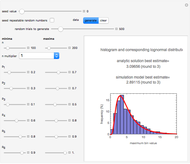

Snapshot 1: PCA VaR stabilizes when the number of principal components exceeds three

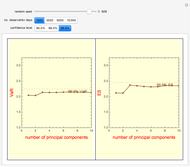

Snapshot 2: divergence of PCA VaR (plotted points) from the "true" asymptotic VaR (dashed horizontal lines) is more pronounced: (1) toward the tail of the distribution (higher confidence level); and (2) with a small number of data points (1,000 observation days)

Snapshot 3: divergence decreases with a larger number of data points (10-fold increase from Snapshot 2)

Reference

[1] Kevin Dowd, Measuring Market Risk, 2nd ed., West Sussex, England: Wiley, 2005 pp. 118–125.

Permanent Citation

Generalized Extreme Value Distributions: Application in Financial Risk Management

Generalized Extreme Value Distributions: Application in Financial Risk Management

Pichet Thiansathaporn Attributing Portfolio Value at Risk: Relations with Component VaR, Marginal VaR, and Incremental VaR

Attributing Portfolio Value at Risk: Relations with Component VaR, Marginal VaR, and Incremental VaR

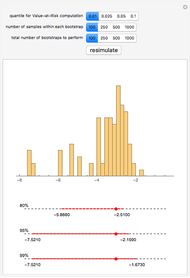

Pichet Thiansathaporn Bootstrapping to Compute Value-at-Risk Standard Errors

Bootstrapping to Compute Value-at-Risk Standard Errors

Jeff Hamrick Amortized Loan Interest and Principal

Amortized Loan Interest and Principal

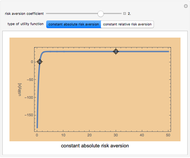

Fiona Maclachlan Constant Risk Aversion Utility Functions

Constant Risk Aversion Utility Functions

Seth J. Chandler Earned Value Management

Earned Value Management

Hagen Lotze Risk, Ownership, and Control

Risk, Ownership, and Control

Roger J. Brown Expected Returns of the Dow Industrials, Fama-French Model

Expected Returns of the Dow Industrials, Fama-French Model

Jeff Hamrick and Jason Cawley Expanded Fermi Solution for Risk Assessment

Expanded Fermi Solution for Risk Assessment

Mark D. Normand, Micha Peleg and Joseph Horowitz Present Value Calculator

Present Value Calculator

Craig Bauling

-

Generalized Extreme Value Distributions: Application in Financial Risk Management

Pichet Thiansathaporn -

Portfolio Diversification Benefit from Subadditive VaR

Portfolio Diversification Benefit from Subadditive VaR

Pichet Thiansathaporn -

Attributing Portfolio Value at Risk: Relations with Component VaR, Marginal VaR, and Incremental VaR

Pichet Thiansathaporn -

Principal Components Analysis: Application in Value at Risk and Expected Shortfall

Principal Components Analysis: Application in Value at Risk and Expected Shortfall

Pichet Thiansathaporn -

Fisher-Tippett-Gnedenko Theorem: Generalizing Three Types of Extreme Value Distributions

Fisher-Tippett-Gnedenko Theorem: Generalizing Three Types of Extreme Value Distributions

Pichet Thiansathaporn