Simulating a Catastrophe Insurer

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

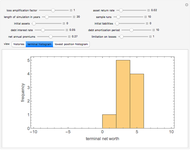

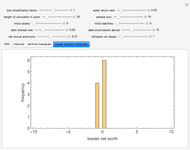

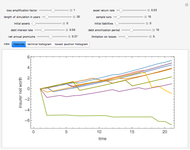

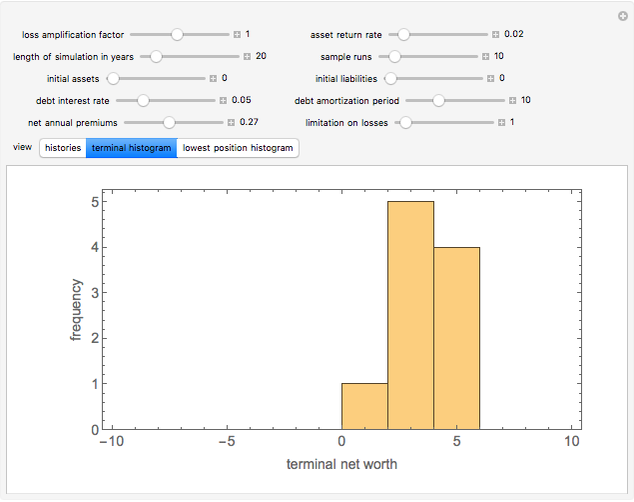

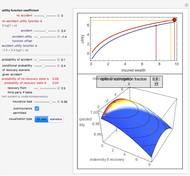

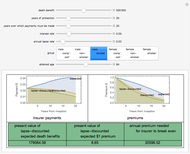

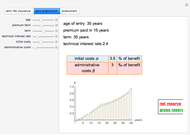

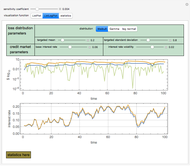

This Demonstration simulates the financial history of a catastrophe insurer. You select a variety of parameters that affect that financial history and the Demonstration responds with a graphic showing the annual net worth of the insurer for each of a user-chosen number of sample runs. You can also choose to display a histogram showing the distribution of the net worth of the insurer either at the end of the simulations or at its lowest annual value.

[more]

Contributed by: Seth J. Chandler (March 2011)

Open content licensed under CC BY-NC-SA

Snapshots

Details

The data from which the event sets are calculated is based on the projected losses of the Texas Windstorm Insurance Association from hurricanes as of 2007.

Snapshot 1: the distribution of the terminal net worth of the insurer using the default settings

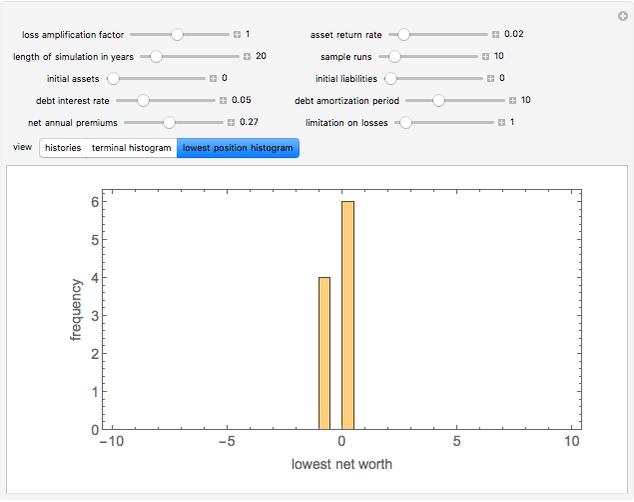

Snapshot 2: the distribution of the lowest annual net worth of the insurer using the default settings

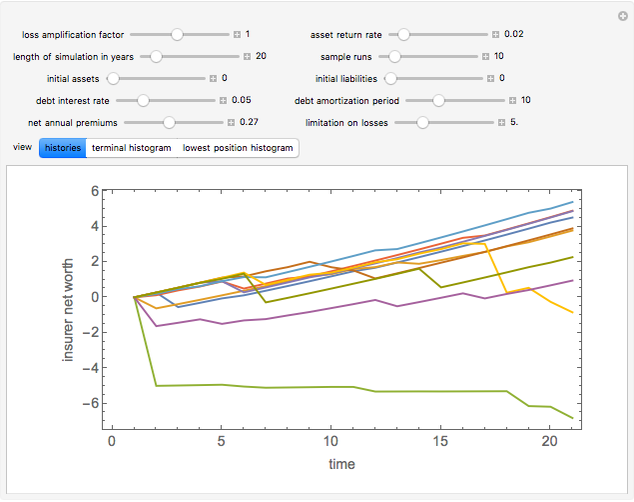

Snapshot 3: the financial history of the insurer if maximum losses are capped at 5 instead of the default value of 1

Snapshot 4: the financial history of the insurer if it has to borrow at 8% instead of the default value of 5%

Snapshot 5: the financial history of the insurer if losses are amplified by 50%

Snapshot 6: the financial history of the insurer if premiums are increased by about 50% over their default value

Snapshot 7: the financial history of the insurer using 50-year runs

Snapshot 8: the distribution of the lowest annual net worth of the insurer using 50-year runs

Permanent Citation

"Simulating a Catastrophe Insurer"

http://demonstrations.wolfram.com/SimulatingACatastropheInsurer/

Wolfram Demonstrations Project

Published: March 7 2011

Insurance Disclosures

Insurance Disclosures

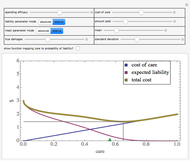

Seth J. Chandler Efficient Single Limit Liability Insurance

Efficient Single Limit Liability Insurance

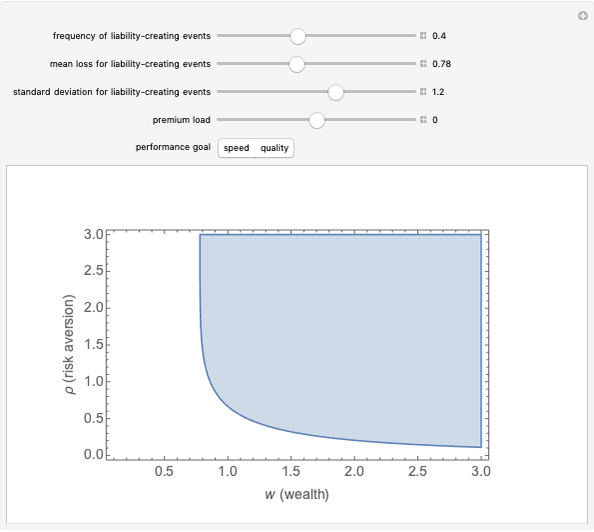

Seth J. Chandler Risk Aversion, Load, and Optimal Insurance

Risk Aversion, Load, and Optimal Insurance

Seth J. Chandler Subrogation

Subrogation

Seth J. Chandler Life Insurance Pricing

Life Insurance Pricing

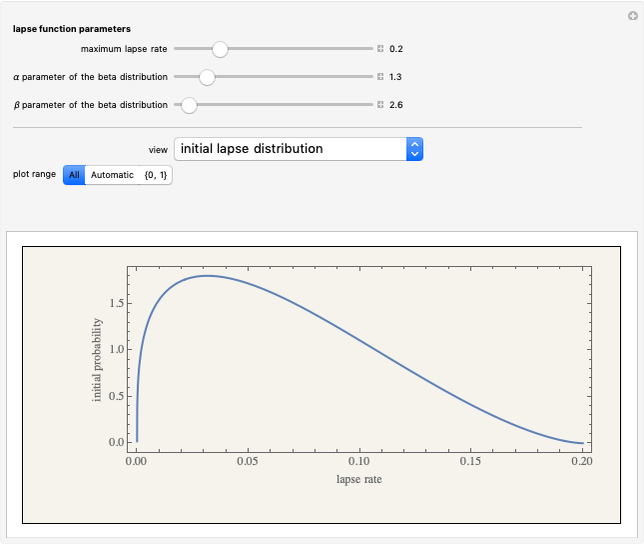

Seth J. Chandler A Theory of Insurance Lapses

A Theory of Insurance Lapses

Seth J. Chandler Net and Gross Reserve of Life Insurance

Net and Gross Reserve of Life Insurance

Gergely Nagy Individual Insurance Decisions under HR 3560 and HR 3962

Individual Insurance Decisions under HR 3560 and HR 3962

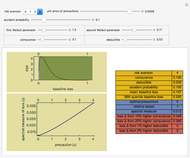

Seth J. Chandler Property Coinsurance

Property Coinsurance

Seth J. Chandler Premium Ratios with Capital Costs Included

Premium Ratios with Capital Costs Included

Seth J. Chandler

-

Post-Event Bonding

Post-Event Bonding

Seth J. Chandler -

Emulating Land Use Evolution with a Cellular Automaton

Emulating Land Use Evolution with a Cellular Automaton

Seth J. Chandler -

General Assembly Resolution Viewer

General Assembly Resolution Viewer

Seth J. Chandler -

Random Acyclic Networks

Random Acyclic Networks

Seth J. Chandler -

A Theory of Insurance Lapses

Seth J. Chandler -

Asylum in the United States

Asylum in the United States

Seth J. Chandler -

Property Coinsurance

Seth J. Chandler -

The Persuasion Effect: A Traditional Two-Stage Jury Model

The Persuasion Effect: A Traditional Two-Stage Jury Model

Seth J. Chandler -

Cellular Automata with Global Control

Cellular Automata with Global Control

Seth J. Chandler -

Sports Seasons Based on Score Distributions

Sports Seasons Based on Score Distributions

Seth J. Chandler -

Evidentiary Uncertainty

Evidentiary Uncertainty

Seth J. Chandler -

Spectral Measures

Spectral Measures

Seth J. Chandler -

The Banzhaf Power Index of States for Presidential Candidates

The Banzhaf Power Index of States for Presidential Candidates

Seth J. Chandler -

Liability Insurance Desirability under Lognormal Loss Distributions

Liability Insurance Desirability under Lognormal Loss Distributions

Seth J. Chandler -

The Effects of Coinsurance and Deductibles on Optimal Precautions for Weibull-Distributed Loss

The Effects of Coinsurance and Deductibles on Optimal Precautions for Weibull-Distributed Loss

Seth J. Chandler -

Collocation by Chi Square

Collocation by Chi Square

Seth J. Chandler -

The Present Value of Future Gas Use

The Present Value of Future Gas Use

Seth J. Chandler -

Visualizing Legal Rules: A Homicide Case

Visualizing Legal Rules: A Homicide Case

Seth J. Chandler -

Communities of Nations Bridged by Language Similarity

Communities of Nations Bridged by Language Similarity

Seth J. Chandler