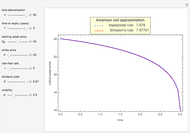

Kim's Method for Pricing American Options

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

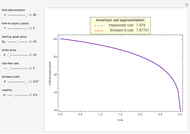

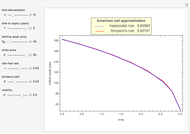

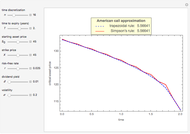

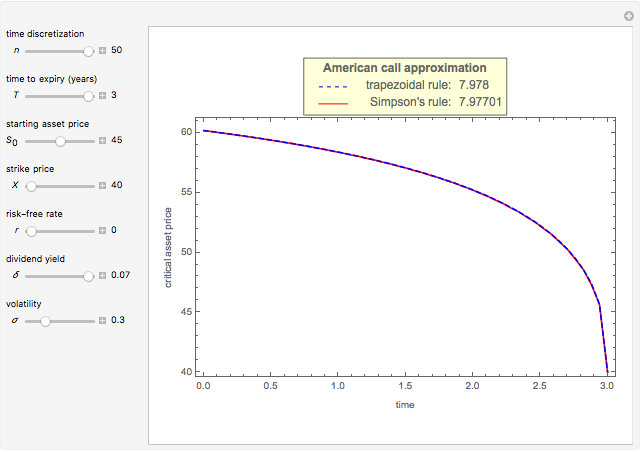

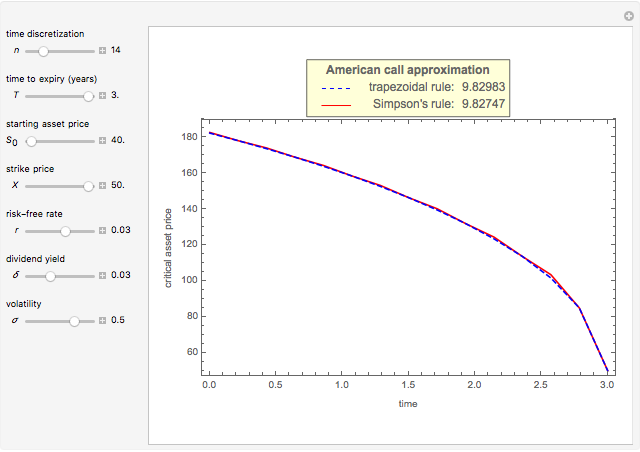

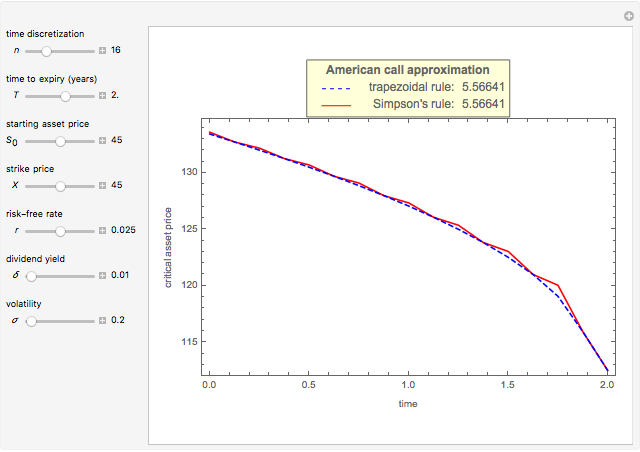

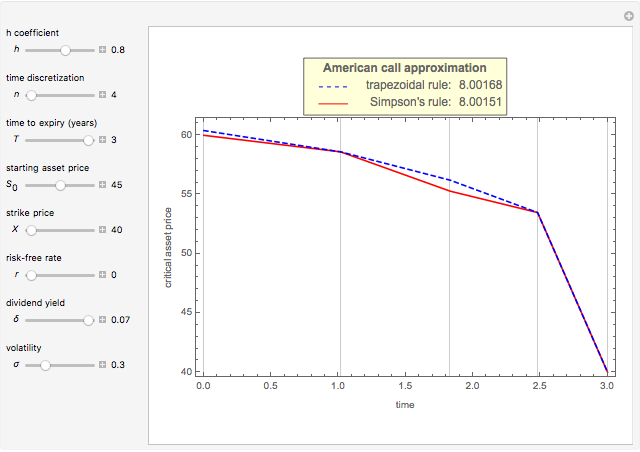

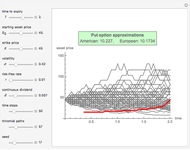

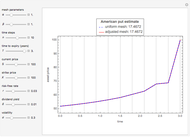

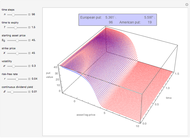

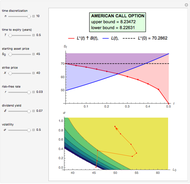

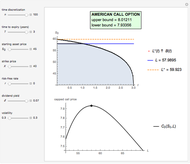

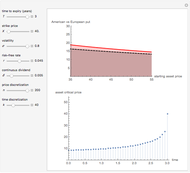

This Demonstration shows Kim's method [1] for pricing American options. A European financial option is an instrument that allows its holder the right to buy or sell an equity at a future maturity date for a fixed price called the "strike price." An American option allows its holder to exercise the contract at any time up to the maturity date, and because of this it is worth more than the European option, by an amount called the "early exercise premium." For the American call's holder, the early exercise becomes optimal when the underlying asset price exceeds a critical boundary  , above which the intrinsic value of the option becomes greater than its holding value.

, above which the intrinsic value of the option becomes greater than its holding value.

Contributed by: Michail Bozoudis (May 2016)

Suggested by: Michail Boutsikas

Open content licensed under CC BY-NC-SA

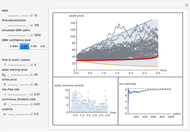

Snapshots

Details

In this detailed description, the symbols have the following meanings:  : current time;

: current time;  : maturity date;

: maturity date;  : stock price at time ;

: stock price at time ;  : strike price;

: strike price;  : stock dividend yield;

: stock dividend yield;  : risk-free interest rate;

: risk-free interest rate;  : stock volatility;

: stock volatility;  : the cumulative distribution function of the standard normal distribution;

: the cumulative distribution function of the standard normal distribution;  : the moving free boundary; : the optimal boundary.

: the moving free boundary; : the optimal boundary.

Consider the class of contracts consisting of a European call option and a sure flow of payments that are paid at the rate

for

for  ,

,

where

,

,

,

,

and  is a non-negative continuous function of time. Each member of the class of contracts is parametrized by . The value of the contract at time is

is a non-negative continuous function of time. Each member of the class of contracts is parametrized by . The value of the contract at time is

,

,

where  denotes the value at time of a European call option on

denotes the value at time of a European call option on  with strike price and maturity . The optimal exercise boundary for the American call option is obtained by solving the "value matching condition":

with strike price and maturity . The optimal exercise boundary for the American call option is obtained by solving the "value matching condition":

, for

, for  for all .

for all .

The value of the American call option  is then given by

is then given by  .

.

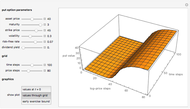

Subject to the "value matching condition," the critical asset price at time can be numerically approximated by a computationally intensive recursive procedure. This method requires solving  integral equations, where is the number of time steps. Each time the integral equation is solved, either the trapezoidal rule (Wolfram MathWorld) or Simpson's rule (Wolfram MathWorld) is employed to approximate the integral.

integral equations, where is the number of time steps. Each time the integral equation is solved, either the trapezoidal rule (Wolfram MathWorld) or Simpson's rule (Wolfram MathWorld) is employed to approximate the integral.

References

[1] I. J. Kim, “The Analytic Valuation of American Options,” Review of Financial Studies, 3(4), 1990 pp. 547–572. www.jstor.org/stable/2962115.

[2] M. Broadie and J. Detemple, "American Option Valuation: New Bounds, Approximations, and a Comparison of Existing Methods," The Review of Financial Studies, 9(4), 1996 pp. 1211–1250. doi:10.1093/rfs/9.4.1211.

Permanent Citation

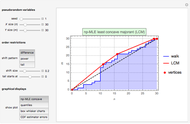

Kim's Method with Nonuniform Time Grid for Pricing American Options

Kim's Method with Nonuniform Time Grid for Pricing American Options

Michail Bozoudis Adaptive Mesh Relocation-Refinement (AMrR) on Kim's Method for Options Pricing

Adaptive Mesh Relocation-Refinement (AMrR) on Kim's Method for Options Pricing

Michail Bozoudis Pricing American Options with the Lower-Upper Bound Approximation (LUBA) Method

Pricing American Options with the Lower-Upper Bound Approximation (LUBA) Method

Michail Bozoudis A Recursive Integration Method for Options Pricing

A Recursive Integration Method for Options Pricing

Michail Bozoudis Pricing American Options with the Two- and Three-Point Maximum Methods

Pricing American Options with the Two- and Three-Point Maximum Methods

Michail Bozoudis Pricing Put Options with the Binomial Method

Pricing Put Options with the Binomial Method

Michail Bozoudis Pricing Put Options with the Trinomial Method

Pricing Put Options with the Trinomial Method

Michail Bozoudis Pricing Put Options with the Crank-Nicolson Method

Pricing Put Options with the Crank-Nicolson Method

Michail Bozoudis A Canonical Optimal Stopping Problem for American Options

A Canonical Optimal Stopping Problem for American Options

Michail Bozoudis Pricing Put Options with the Explicit Finite-Difference Method

Pricing Put Options with the Explicit Finite-Difference Method

Michail Bozoudis

-

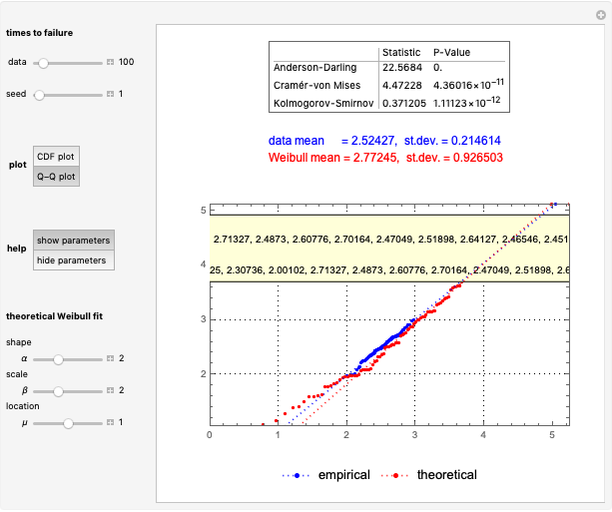

Fitting Times-to-Failure to a Weibull Distribution

Fitting Times-to-Failure to a Weibull Distribution

Michail Bozoudis -

A Canonical Optimal Stopping Problem for American Options

Michail Bozoudis -

A Recursive Integration Method for Options Pricing

Michail Bozoudis -

Adaptive Mesh Relocation-Refinement (AMrR) on Kim's Method for Options Pricing

Michail Bozoudis -

Kim's Method with Nonuniform Time Grid for Pricing American Options

Michail Bozoudis -

Geometric Brownian Motion with Nonuniform Time Grid

Geometric Brownian Motion with Nonuniform Time Grid

Michail Bozoudis -

Kim's Method for Pricing American Options

Kim's Method for Pricing American Options

Michail Bozoudis -

Simultaneous Confidence Interval for the Weibull Parameters

Simultaneous Confidence Interval for the Weibull Parameters

Michail Bozoudis -

Binomial Black-Scholes with Richardson Extrapolation (BBSR) Method

Binomial Black-Scholes with Richardson Extrapolation (BBSR) Method

Michail Bozoudis -

Pricing American Options with the Lower-Upper Bound Approximation (LUBA) Method

Michail Bozoudis -

American Options on Assets with Dividends Near Expiry

American Options on Assets with Dividends Near Expiry

Michail Bozoudis -

Hold-or-Exercise for an American Put Option

Hold-or-Exercise for an American Put Option

Michail Bozoudis -

American Capped Call Options with Exponential Cap

American Capped Call Options with Exponential Cap

Michail Bozoudis -

American Capped Call Options with Constant Cap

American Capped Call Options with Constant Cap

Michail Bozoudis -

Pricing Put Options with the Crank-Nicolson Method

Michail Bozoudis -

Pricing Put Options with the Implicit Finite-Difference Method

Pricing Put Options with the Implicit Finite-Difference Method

Michail Bozoudis -

Estimating a Distribution Function Subject to a Stochastic Order Restriction

Estimating a Distribution Function Subject to a Stochastic Order Restriction

Michail Bozoudis -

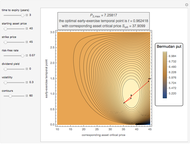

Maximizing a Bermudan Put with a Single Early-Exercise Temporal Point

Maximizing a Bermudan Put with a Single Early-Exercise Temporal Point

Michail Bozoudis -

Fitting Data to a Lognormal Distribution

Fitting Data to a Lognormal Distribution

Michail Bozoudis -

SARIMA Process Forecasting Model

SARIMA Process Forecasting Model

Michail Bozoudis