American Capped Call Options with Constant Cap

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

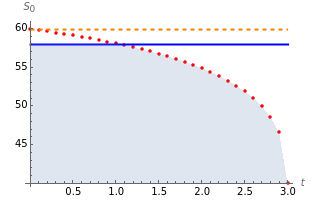

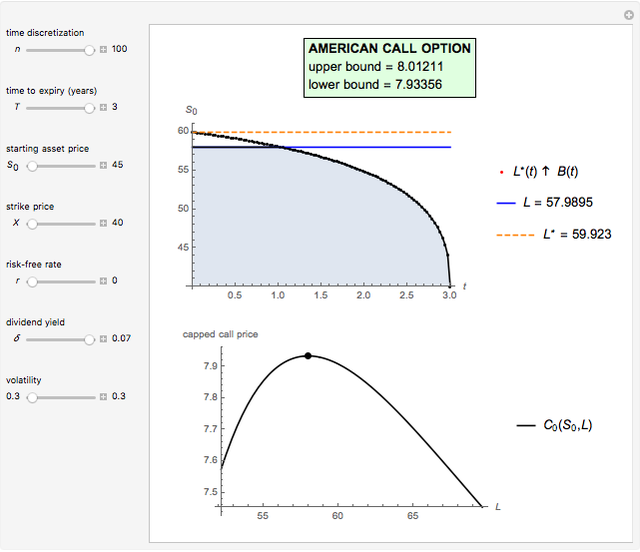

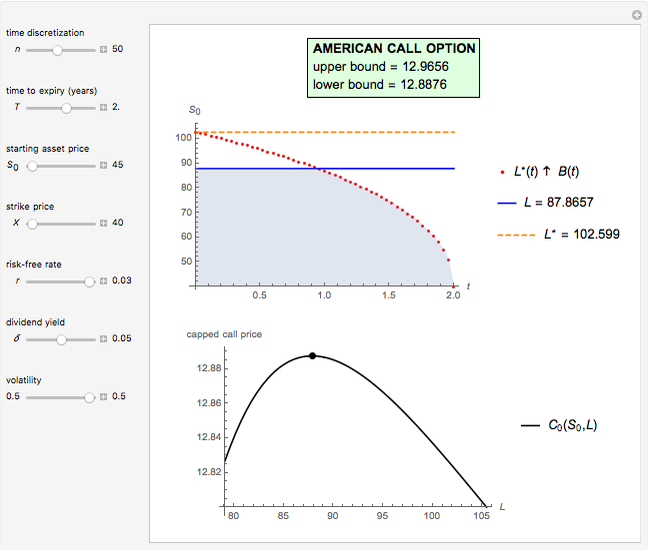

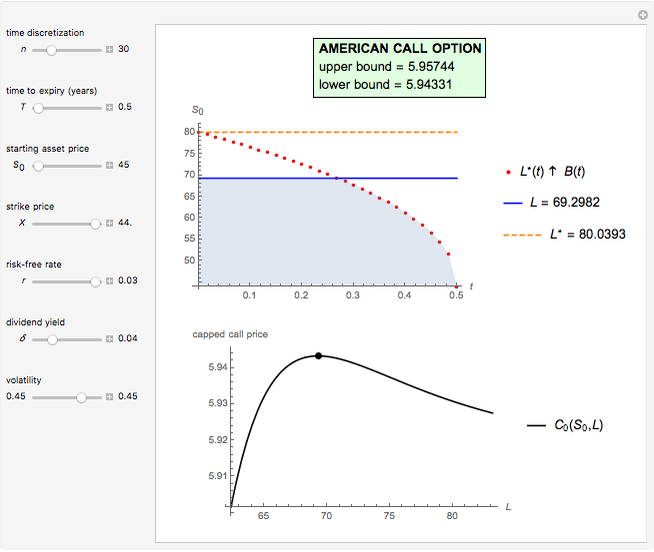

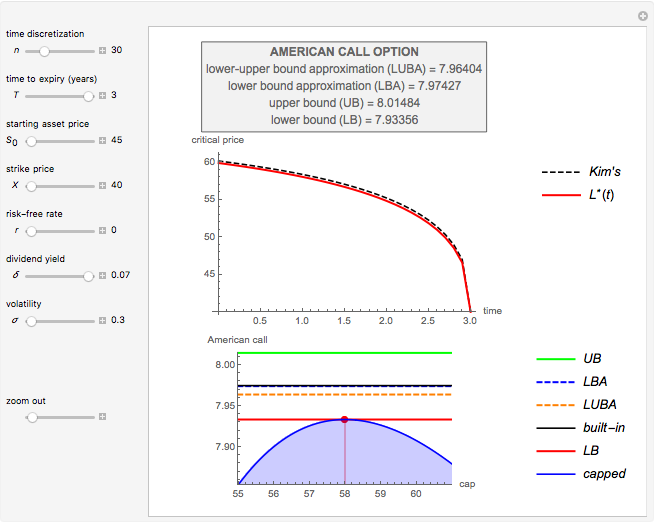

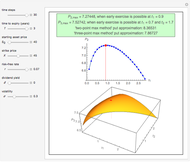

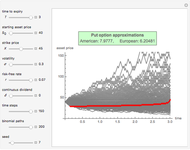

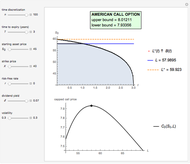

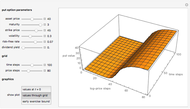

This Demonstration shows the maximization process of an American capped call option with a constant cap (or barrier). Because the capped call must be instantly exercised if the underlying asset price rises above a predetermined price  , which is called the "cap" or "cap price", its value never exceeds the value of the standard American call. Thus, identifying the cap that maximizes the capped call payoff function

, which is called the "cap" or "cap price", its value never exceeds the value of the standard American call. Thus, identifying the cap that maximizes the capped call payoff function  , we obtain a lower bound

, we obtain a lower bound  for the American call price. Moreover, the evaluation of the capped call payoff function derivative with respect to the cap, while the underlying asset price approaches the cap from below, provides a lower approach

for the American call price. Moreover, the evaluation of the capped call payoff function derivative with respect to the cap, while the underlying asset price approaches the cap from below, provides a lower approach  for the American call optimal exercise boundary

for the American call optimal exercise boundary  [1]. Finally, after replacing

[1]. Finally, after replacing  with

with  in Kim's integral equation [2], an upper bound

in Kim's integral equation [2], an upper bound  for the American call price is obtained. Thus the capped call option is really a tool used to bracket the pricing of the commonly traded American option.

for the American call price is obtained. Thus the capped call option is really a tool used to bracket the pricing of the commonly traded American option.

Contributed by: Michail Bozoudis (February 2016)

Suggested by: Michail Boutsikas

Open content licensed under CC BY-NC-SA

Snapshots

Details

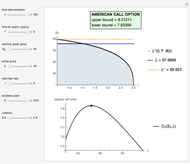

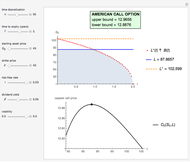

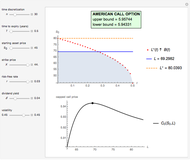

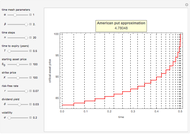

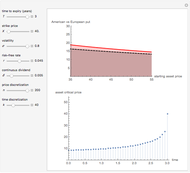

M. Broadie and J. Detemple [3] developed an analytical formula to estimate American capped call options. In order to approximate an American call payoff  , they use the value of a capped call written on the same asset [1]. If the price of the underlying asset is

, they use the value of a capped call written on the same asset [1]. If the price of the underlying asset is  , when

, when  the payoff of a capped call option is

the payoff of a capped call option is  , where

, where  is the strike price and is the cap. The payoff is the same as a standard American option, except that the cap limits the maximum possible payoff. Since the policy of exercising when the asset price reaches the constant cap is an admissible policy for the American option,

is the strike price and is the cap. The payoff is the same as a standard American option, except that the cap limits the maximum possible payoff. Since the policy of exercising when the asset price reaches the constant cap is an admissible policy for the American option,  for any .

for any .

Hence a lower bound  is still obtained after optimizing over :

is still obtained after optimizing over :

.

.

The determination of  is a simple univariate differentiable optimization problem for any given . In this Demonstration, Mathematica's built-in function NMaximize is applied.

is a simple univariate differentiable optimization problem for any given . In this Demonstration, Mathematica's built-in function NMaximize is applied.

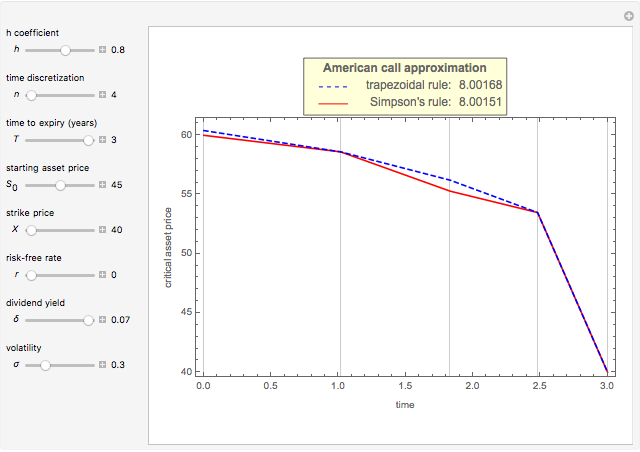

The evaluation of the capped call payoff function derivative with respect to the cap, while the underlying asset price approaches the cap from below, leads to an exercise boundary  , where is the American call optimal early exercise boundary at time

, where is the American call optimal early exercise boundary at time  . The boundary is the solution to the equation

. The boundary is the solution to the equation  , where

, where  .

.

In this Demonstration, the Newton–Raphson technique is applied to solve . Moreover, M. Broadie and J. Detemple [1] prove that an upper bound for the American call price is obtained, after replacing the optimal early exercise boundary function with in Kim's integral equation [2]. The integral in Kim's equation represents the early exercise premium and is approximated by Simpson's rule.

References

[1] M. Broadie and J. Detemple, "American Option Valuation: New Bounds, Approximations, and a Comparison of Existing Methods," The Review of Financial Studies, 9(4), 1996 pp. 1211–1250.

[2] I. J. Kim, “The Analytic Valuation of American Options,” The Review of Financial Studies, 3(4), 1990 pp. 547–572.

[3] M. Broadie and J. Detemple, "American Capped Call Options on Dividend Paying Assets," The Review of Financial Studies, 8(1), 1995 pp. 161–191.

Permanent Citation

American Capped Call Options with Exponential Cap

American Capped Call Options with Exponential Cap

Michail Bozoudis Pricing American Options with the Lower-Upper Bound Approximation (LUBA) Method

Pricing American Options with the Lower-Upper Bound Approximation (LUBA) Method

Michail Bozoudis American Options on Assets with Dividends Near Expiry

American Options on Assets with Dividends Near Expiry

Michail Bozoudis Kim's Method for Pricing American Options

Kim's Method for Pricing American Options

Michail Bozoudis A Canonical Optimal Stopping Problem for American Options

A Canonical Optimal Stopping Problem for American Options

Michail Bozoudis Kim's Method with Nonuniform Time Grid for Pricing American Options

Kim's Method with Nonuniform Time Grid for Pricing American Options

Michail Bozoudis Pricing American Options with the Two- and Three-Point Maximum Methods

Pricing American Options with the Two- and Three-Point Maximum Methods

Michail Bozoudis A Recursive Integration Method for Options Pricing

A Recursive Integration Method for Options Pricing

Michail Bozoudis Pricing Put Options with the Trinomial Method

Pricing Put Options with the Trinomial Method

Michail Bozoudis Pricing Put Options with the Binomial Method

Pricing Put Options with the Binomial Method

Michail Bozoudis

-

Fitting Times-to-Failure to a Weibull Distribution

Fitting Times-to-Failure to a Weibull Distribution

Michail Bozoudis -

A Canonical Optimal Stopping Problem for American Options

Michail Bozoudis -

A Recursive Integration Method for Options Pricing

Michail Bozoudis -

Adaptive Mesh Relocation-Refinement (AMrR) on Kim's Method for Options Pricing

Adaptive Mesh Relocation-Refinement (AMrR) on Kim's Method for Options Pricing

Michail Bozoudis -

Kim's Method with Nonuniform Time Grid for Pricing American Options

Michail Bozoudis -

Geometric Brownian Motion with Nonuniform Time Grid

Geometric Brownian Motion with Nonuniform Time Grid

Michail Bozoudis -

Kim's Method for Pricing American Options

Michail Bozoudis -

Simultaneous Confidence Interval for the Weibull Parameters

Simultaneous Confidence Interval for the Weibull Parameters

Michail Bozoudis -

Binomial Black-Scholes with Richardson Extrapolation (BBSR) Method

Binomial Black-Scholes with Richardson Extrapolation (BBSR) Method

Michail Bozoudis -

Pricing American Options with the Lower-Upper Bound Approximation (LUBA) Method

Michail Bozoudis -

American Options on Assets with Dividends Near Expiry

Michail Bozoudis -

Hold-or-Exercise for an American Put Option

Hold-or-Exercise for an American Put Option

Michail Bozoudis -

American Capped Call Options with Exponential Cap

Michail Bozoudis -

American Capped Call Options with Constant Cap

American Capped Call Options with Constant Cap

Michail Bozoudis -

Pricing Put Options with the Crank-Nicolson Method

Pricing Put Options with the Crank-Nicolson Method

Michail Bozoudis -

Pricing Put Options with the Implicit Finite-Difference Method

Pricing Put Options with the Implicit Finite-Difference Method

Michail Bozoudis -

Estimating a Distribution Function Subject to a Stochastic Order Restriction

Estimating a Distribution Function Subject to a Stochastic Order Restriction

Michail Bozoudis -

Maximizing a Bermudan Put with a Single Early-Exercise Temporal Point

Maximizing a Bermudan Put with a Single Early-Exercise Temporal Point

Michail Bozoudis -

Fitting Data to a Lognormal Distribution

Fitting Data to a Lognormal Distribution

Michail Bozoudis -

SARIMA Process Forecasting Model

SARIMA Process Forecasting Model

Michail Bozoudis