Liability Insurance Desirability When "Diminution" Is Unlawful

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

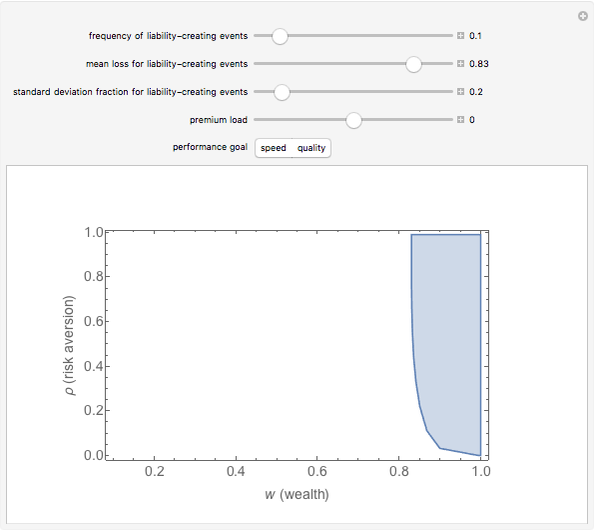

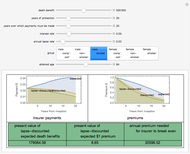

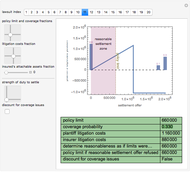

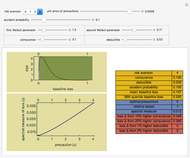

Consider an entity facing potential liability that has purchased a liability insurance contract providing that it will pay a third party up to an amount  if a judgment is rendered. If the insured could act selfishly, it would prefer an insurance contract that would "diminish": it would specify that in the event a judgment against the insured would, even with the existence of the liability insurance, bankrupt the insured, the insurer should pay nothing. This is so because payments to a third party in such a setting do essentially nothing to help the insured, but drive up the cost of premiums because the insurer must pay. Either as the result of regulation or custom, however, such "diminution" provisions are generally unlawful. This is so because diminution might otherwise prevent victims from being compensated more fully when individuals with liability insurance injure them. This restriction on freedom of contract means, however, that there are some settings in which insureds, even though they might like to transfer risk, find it undesirable to do so.

if a judgment is rendered. If the insured could act selfishly, it would prefer an insurance contract that would "diminish": it would specify that in the event a judgment against the insured would, even with the existence of the liability insurance, bankrupt the insured, the insurer should pay nothing. This is so because payments to a third party in such a setting do essentially nothing to help the insured, but drive up the cost of premiums because the insurer must pay. Either as the result of regulation or custom, however, such "diminution" provisions are generally unlawful. This is so because diminution might otherwise prevent victims from being compensated more fully when individuals with liability insurance injure them. This restriction on freedom of contract means, however, that there are some settings in which insureds, even though they might like to transfer risk, find it undesirable to do so.

Contributed by: Seth J. Chandler (December 2012)

Open content licensed under CC BY-NC-SA

Snapshots

Details

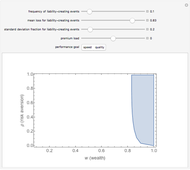

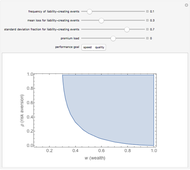

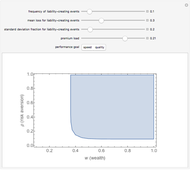

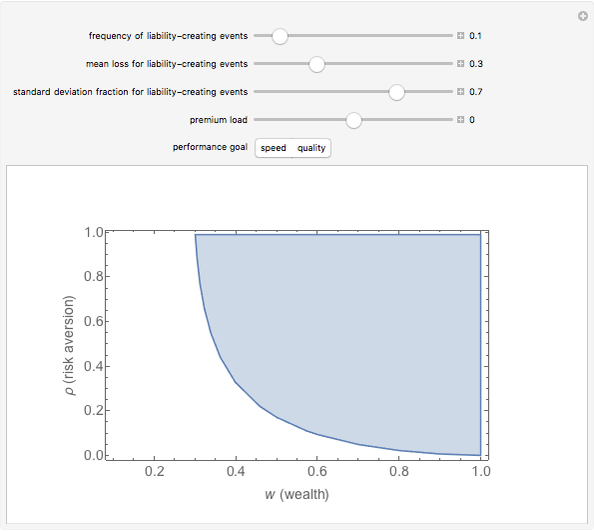

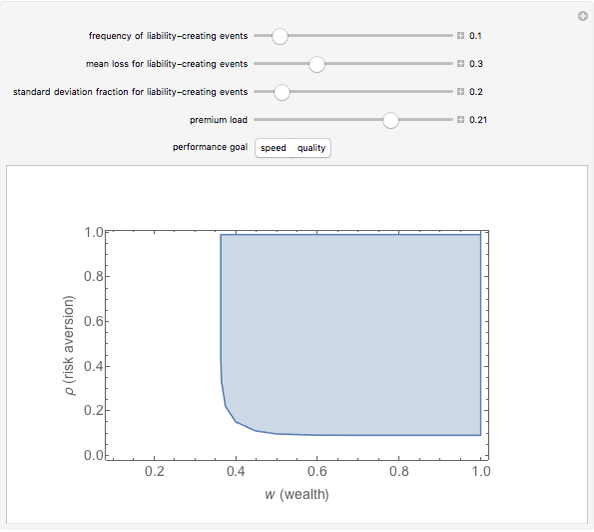

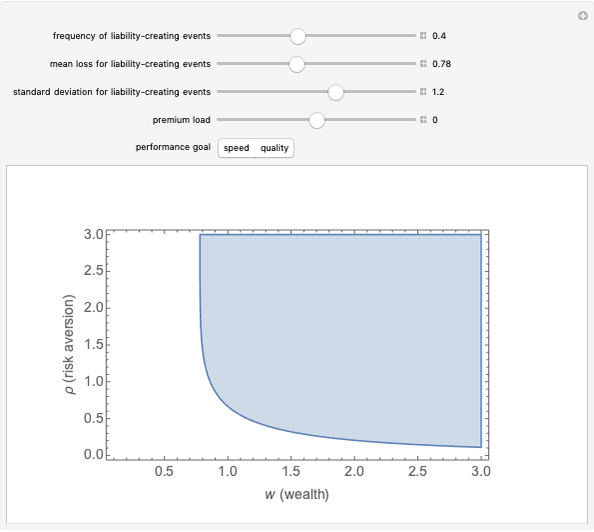

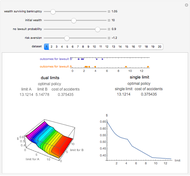

The combinations of wealth and risk aversion that result in full insurance shrink when:

Snapshot 1: mean losses are larger

Snapshot 2: the standard deviation of losses is larger

Snapshot 3: the premium load is greater

This Demonstration makes use of the Mathematica compiler to achieve additional speed.

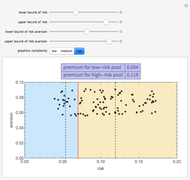

The method of parameterizing risk aversion used in this Demonstration is somewhat unorthodox, but has been the only one discovered by the author to date that yields a closed-form solution. The idea is basically to treat risk aversion as if you were drawing from a distribution shaped similarly to the original distribution but with a higher mean. Here, in computing risk, we draw from a distribution with mean  , which collapses to

, which collapses to  if risk aversion

if risk aversion  is zero, to 1 if risk aversion is 1, and otherwise takes on values between and 1 that increase with . The idea derives from the concept of spectral measures which, as discussed by the author here, is similar to drawing from an

is zero, to 1 if risk aversion is 1, and otherwise takes on values between and 1 that increase with . The idea derives from the concept of spectral measures which, as discussed by the author here, is similar to drawing from an  -order distribution of

-order distribution of  observations of a loss distribution. Such an order distribution generally results in higher draws than the original distribution. Thus, drawing from an order distribution is similar to drawing from a distribution that is shaped similarly but has a higher mean. It is thus a reasonable way of simulating risk aversion.

observations of a loss distribution. Such an order distribution generally results in higher draws than the original distribution. Thus, drawing from an order distribution is similar to drawing from a distribution that is shaped similarly but has a higher mean. It is thus a reasonable way of simulating risk aversion.

A beta distribution is used here because (a) it can readily simulate distributions with large and small variances; and (b) it results in a closed-form solution to the problem at hand when used in conjunction with the method described above for risk aversion. The principles shown in this Demonstration are likely to be applicable, however, to a broader class of loss distributions. The key is to be able to scale the wealth of the insured available for execution to some metric of the distribution, such as the upper bound of its domain, or some high quantile of the distribution.

The beta distribution employed in the code here has been reparameterized to permit more direct representation of mean and standard deviation.

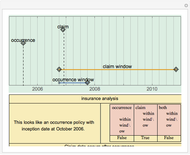

Although most liability insurance contracts contain a clause prohibiting the insurer from reducing the amount it pays a third party based on their insured's insolvency, some insurance contracts do not. Notably, reinsurance contracts sometimes do not have such a clause nor do some maritime insurance policies.

References

[1] S. Shavell, "The Judgment Proof Problem," International Review of Law and Economics 6, 1986 pp. 45–58.

[2] S. Chandler, "A 'Genetically Modified' Liability Insurance Contract," University of Connecticut Insurance Law Journal, 13(2), 2007 pp. 203–265. insurancejournal.org/wp-content/uploads/2011/07/15.pdf.

Permanent Citation

Liability Insurance Desirability under Lognormal Loss Distributions

Liability Insurance Desirability under Lognormal Loss Distributions

Seth J. Chandler Efficient Single Limit Liability Insurance

Efficient Single Limit Liability Insurance

Seth J. Chandler The Efficient Dual-Limit Liability Insurance Contract

The Efficient Dual-Limit Liability Insurance Contract

Seth J. Chandler Insurance Disclosures

Insurance Disclosures

Seth J. Chandler Life Insurance Pricing

Life Insurance Pricing

Seth J. Chandler Coordination of Insurance Policies

Coordination of Insurance Policies

Seth J. Chandler Occurrence versus Claims-Made Insurance Policies

Occurrence versus Claims-Made Insurance Policies

Seth J. Chandler A Conceptual Model of Lapse Financed Life Insurance

A Conceptual Model of Lapse Financed Life Insurance

Seth J. Chandler The Duty to Settle

The Duty to Settle

Seth J. Chandler Adverse Selection

Adverse Selection

Seth J. Chandler

-

Post-Event Bonding

Post-Event Bonding

Seth J. Chandler -

Emulating Land Use Evolution with a Cellular Automaton

Emulating Land Use Evolution with a Cellular Automaton

Seth J. Chandler -

General Assembly Resolution Viewer

General Assembly Resolution Viewer

Seth J. Chandler -

Random Acyclic Networks

Random Acyclic Networks

Seth J. Chandler -

A Theory of Insurance Lapses

A Theory of Insurance Lapses

Seth J. Chandler -

Asylum in the United States

Asylum in the United States

Seth J. Chandler -

Property Coinsurance

Property Coinsurance

Seth J. Chandler -

The Persuasion Effect: A Traditional Two-Stage Jury Model

The Persuasion Effect: A Traditional Two-Stage Jury Model

Seth J. Chandler -

Cellular Automata with Global Control

Cellular Automata with Global Control

Seth J. Chandler -

Sports Seasons Based on Score Distributions

Sports Seasons Based on Score Distributions

Seth J. Chandler -

Evidentiary Uncertainty

Evidentiary Uncertainty

Seth J. Chandler -

Spectral Measures

Spectral Measures

Seth J. Chandler -

The Banzhaf Power Index of States for Presidential Candidates

The Banzhaf Power Index of States for Presidential Candidates

Seth J. Chandler -

Liability Insurance Desirability under Lognormal Loss Distributions

Seth J. Chandler -

The Effects of Coinsurance and Deductibles on Optimal Precautions for Weibull-Distributed Loss

The Effects of Coinsurance and Deductibles on Optimal Precautions for Weibull-Distributed Loss

Seth J. Chandler -

Collocation by Chi Square

Collocation by Chi Square

Seth J. Chandler -

The Present Value of Future Gas Use

The Present Value of Future Gas Use

Seth J. Chandler -

Visualizing Legal Rules: A Homicide Case

Visualizing Legal Rules: A Homicide Case

Seth J. Chandler -

Communities of Nations Bridged by Language Similarity

Communities of Nations Bridged by Language Similarity

Seth J. Chandler