Sports Arbitrage: Two-Agency, Two-Outcome Efficient Pricing Test

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

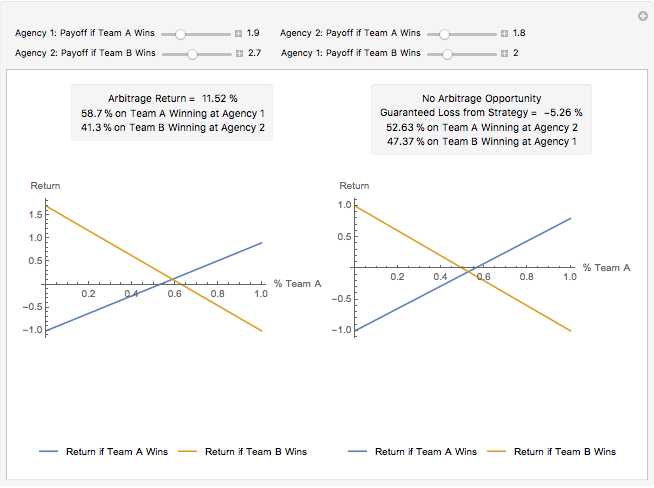

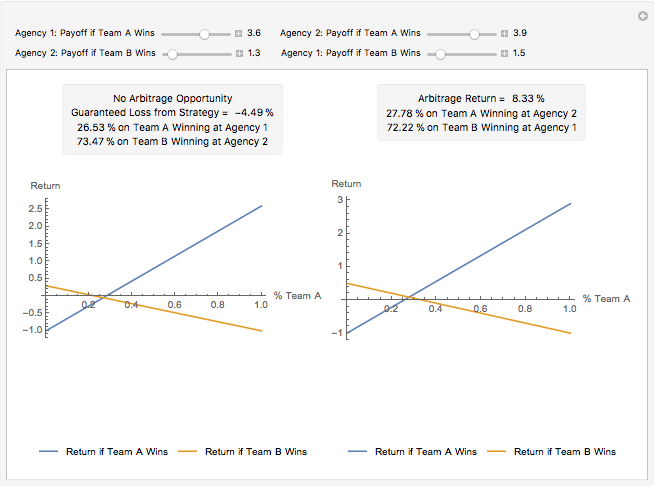

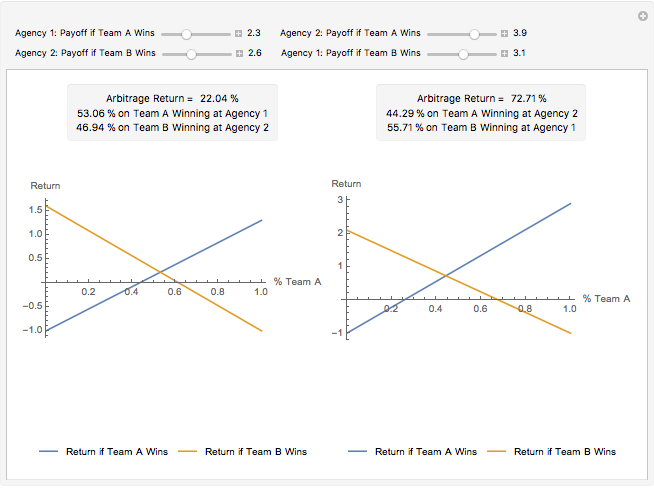

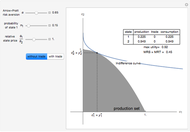

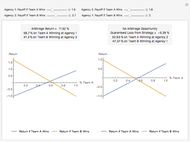

This Demonstration shows the opportunity that may be created if betting agencies do not agree on the odds of a match with two teams and no possibility for a draw. The graphs represent the payoffs of possible weighted portfolios of the two outcomes. The  axis represents the proportion

axis represents the proportion  of any bet in the portfolio on team A winning. If

of any bet in the portfolio on team A winning. If  , then the agent (bet placer) believes team B will win the game. If odds at the agency where the bet was placed are

, then the agent (bet placer) believes team B will win the game. If odds at the agency where the bet was placed are  that team B will win, the bet placer will receive the payoff from the agency minus their initial investment, making their return

that team B will win, the bet placer will receive the payoff from the agency minus their initial investment, making their return  if B does win. If B does not win, they will lose their initial investment (

if B does win. If B does not win, they will lose their initial investment ( ). Let

). Let  and

and  be the payoff from A winning and the payoff from B winning, respectively. The profit functions for a weighted portfolio of outcomes are therefore:

be the payoff from A winning and the payoff from B winning, respectively. The profit functions for a weighted portfolio of outcomes are therefore:

Contributed by: Tom Stannard (May 2015)

Open content licensed under CC BY-NC-SA

Snapshots

Details

References

[1] E. Franck, E. Verbeek, and S. Nüesch, "Inter-market Arbitrage in Betting," Economica, 80(318), 2013 pp. 300–325. doi:10.1111/ecca.12009.

[2] B. R. Marshall, "How Quickly Is Temporary Market Inefficiency Removed?," The Quarterly Review of Economics and Finance, 49(3), 2009 pp. 917–930. doi:10.1016/j.qref.2009.04.006.

Permanent Citation

Sports Scores

Sports Scores

Ted Sanders Run Expectancy Matrix in Baseball

Run Expectancy Matrix in Baseball

Ben Dilday Ratings of NFL Teams from 1985 to 2012

Ratings of NFL Teams from 1985 to 2012

Kevin O'Bryant Stock Price Probability with Stable Distributions

Stock Price Probability with Stable Distributions

Bob Rimmer Power Analysis for a Two-Sample t-Test

Power Analysis for a Two-Sample t-Test

Philip Bontrager Two Jump Diffusion Processes

Two Jump Diffusion Processes

Andrzej Kozlowski Two Dice with Histogram

Two Dice with Histogram

Abby Brown Sports Seasons Based on Score Distributions

Sports Seasons Based on Score Distributions

Seth J. Chandler Linear Dependence between Two Bernoulli Random Variables

Linear Dependence between Two Bernoulli Random Variables

Jeff Hamrick Two-Regime Threshold Autoregressive Model Simulation

Two-Regime Threshold Autoregressive Model Simulation

Jozef Barunik

-

General Equilibrium with Production: Robinson Crusoe with and without Trade

General Equilibrium with Production: Robinson Crusoe with and without Trade

Tom Stannard -

Convergence of Binomial Option Pricing under Nonconstant Volatility

Convergence of Binomial Option Pricing under Nonconstant Volatility

Tom Stannard -

European Binomial Option Pricing with Nonconstant Volatility

European Binomial Option Pricing with Nonconstant Volatility

Tom Stannard -

Sports Arbitrage: Two-Agency, Two-Outcome Efficient Pricing Test

Sports Arbitrage: Two-Agency, Two-Outcome Efficient Pricing Test

Tom Stannard