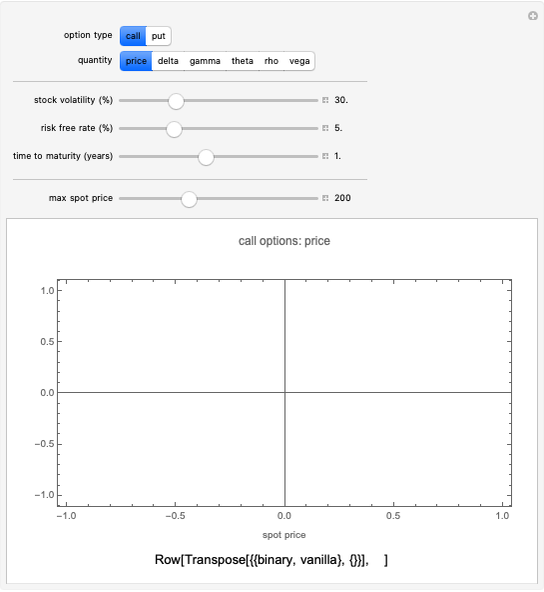

Binary Options: Pricing and Greeks

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

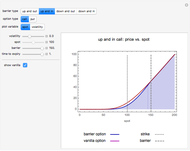

This Demonstration shows the price and "Greeks" for binary call and put options together with the corresponding vanilla European option as a function of underlying spot price (the option strike price  is set to 100). The controls let you explore the effect of the model's input parameters.

is set to 100). The controls let you explore the effect of the model's input parameters.

Contributed by: Peter Falloon (July 2009)

Open content licensed under CC BY-NC-SA

Snapshots

Details

Binary options are a type of exotic option for which the payoff is determined by whether the final stock price  is greater or less than the strike price . A binary call option pays out if

is greater or less than the strike price . A binary call option pays out if  , while a binary put option pays out for

, while a binary put option pays out for  . In this Demonstration we set the payoff amount to be the strike price .

. In this Demonstration we set the payoff amount to be the strike price .

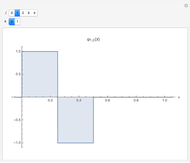

As this Demonstration shows, the price of binary options—and its derivative with respect to the various model inputs—displays some interesting differences compared to the more well-known behavior of European options. For example, the "delta" of at-the-money binary options becomes very large close to expiry, which in practice makes such options difficult to hedge (Snapshot 1).

Another example is the "theta" of binary calls, which can be positive when the option is "in the money" (that is, when spot  strike); by contrast, the theta of European options is always negative (Snapshot 2).

strike); by contrast, the theta of European options is always negative (Snapshot 2).

J. C. Hull, Options, Futures, and Other Derivatives, Upper Saddle Creek, NY: Prentice Hall, 2006.

Permanent Citation

European Option Greeks

European Option Greeks

Michael Kelly (Stuart GSB, Illinois Institute of Technology) Binomial Option Pricing Model

Binomial Option Pricing Model

Fiona Maclachlan Black-Scholes Option Model

Black-Scholes Option Model

Michael Kelly (Stuart GSB, Illinois Institute of Technology) The Minimal Model of the Complexity of Financial Security Prices

The Minimal Model of the Complexity of Financial Security Prices

Philip Maymin Exploring Minimal Models of the Complexity of Security Prices

Exploring Minimal Models of the Complexity of Security Prices

Philip Maymin Minimal Model of Simulating Prices of Financial Securities Using an Iterated Finite Automaton

Minimal Model of Simulating Prices of Financial Securities Using an Iterated Finite Automaton

Philip Maymin Pricing Power Options in the Black-Scholes Model

Pricing Power Options in the Black-Scholes Model

Peter Falloon Life Insurance Pricing

Life Insurance Pricing

Seth J. Chandler Binomial Tree

Binomial Tree

Fiona Maclachlan Stock Price Envelopes

Stock Price Envelopes

Seth J. Chandler

-

Option Prices in Merton's Jump Diffusion Model

Option Prices in Merton's Jump Diffusion Model

Peter Falloon -

Chooser Options

Chooser Options

Peter Falloon -

Binary Options: Pricing and Greeks

Binary Options: Pricing and Greeks

Peter Falloon -

Angular Spheroidal Functions as a Function of Spheroidicity

Angular Spheroidal Functions as a Function of Spheroidicity

Peter Falloon -

Hyperbolic Distribution

Hyperbolic Distribution

Peter Falloon -

Variance-Gamma Distribution

Variance-Gamma Distribution

Peter Falloon -

Options Board Using Black-Scholes Prices

Options Board Using Black-Scholes Prices

Peter Falloon -

Properties of a Simple Random Walk with Boundaries

Properties of a Simple Random Walk with Boundaries

Peter Falloon -

Visualizing Superellipses

Visualizing Superellipses

Peter Falloon -

Haar Functions

Haar Functions

Peter Falloon -

Barrier Option Pricing within the Black-Scholes Model

Barrier Option Pricing within the Black-Scholes Model

Peter Falloon -

Clebsch-Gordan Coefficients

Clebsch-Gordan Coefficients

Peter Falloon -

Constant Coordinate Curves for Elliptic Coordinates

Constant Coordinate Curves for Elliptic Coordinates

Peter Falloon -

Chi-Squared Distribution and the Central Limit Theorem

Chi-Squared Distribution and the Central Limit Theorem

Peter Falloon -

Multiple Slit Diffraction Pattern

Multiple Slit Diffraction Pattern

Peter Falloon -

Constant Coordinate Curves for Parabolic and Polar Coordinates

Constant Coordinate Curves for Parabolic and Polar Coordinates

Peter Falloon -

Distribution of Returns from Merton's Jump Diffusion Model

Distribution of Returns from Merton's Jump Diffusion Model

Peter Falloon -

Pricing Power Options in the Black-Scholes Model

Peter Falloon -

Implied Volatility in Merton's Jump Diffusion Model

Implied Volatility in Merton's Jump Diffusion Model

Peter Falloon -

Game Clock

Game Clock

Peter Falloon