Chooser Options

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

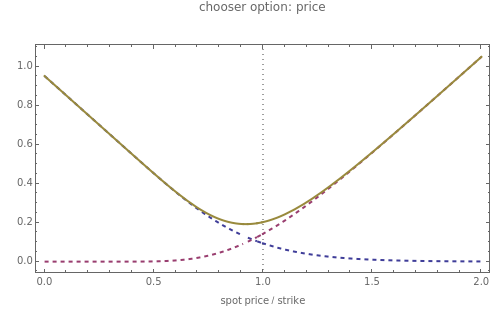

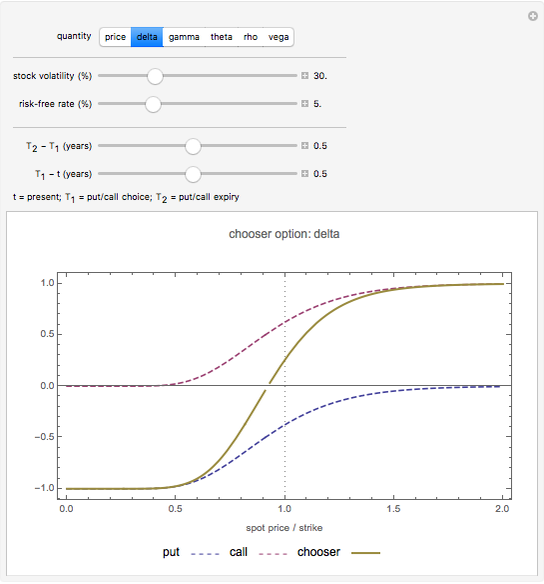

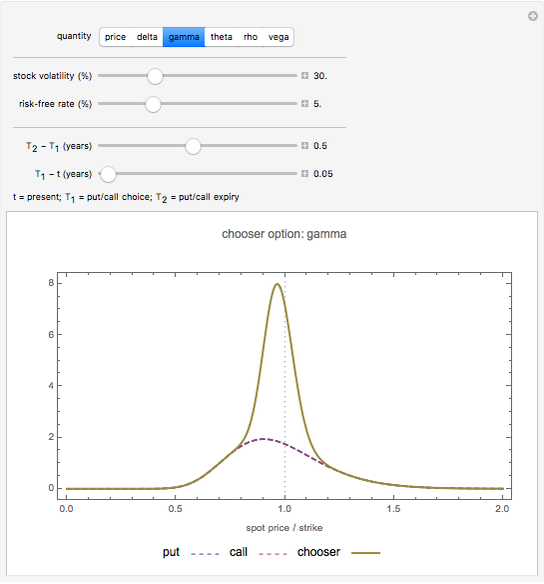

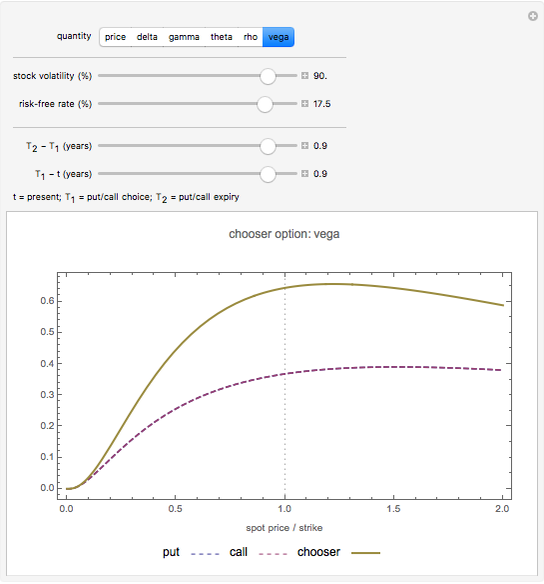

This Demonstration illustrates the price and "greeks" for chooser options in comparison to those for regular put and call options.

Contributed by: Peter Falloon (December 2008)

Open content licensed under CC BY-NC-SA

Snapshots

Details

Chooser options are a type of exotic option that, at some pre-specified time  in the future, can be converted into either a put or call option with expiry

in the future, can be converted into either a put or call option with expiry  and strike

and strike  . The price of a chooser option,

. The price of a chooser option,  , thus tends to be higher than that of the corresponding call or put,

, thus tends to be higher than that of the corresponding call or put,  or

or  . The amount of extra value depends on and

. The amount of extra value depends on and  : for

: for  , is approximately

, is approximately  . As tends to , tends to

. As tends to , tends to  .

.

It can be shown using general put-call parity considerations that, for  , a chooser option is equivalent to a portfolio comprising a call option with strike and expiry together with a put option with strike

, a chooser option is equivalent to a portfolio comprising a call option with strike and expiry together with a put option with strike  and expiry (assuming a constant interest rate

and expiry (assuming a constant interest rate  ). Within the Black–Scholes model, chooser options can therefore be priced using the solutions for call and put options.

). Within the Black–Scholes model, chooser options can therefore be priced using the solutions for call and put options.

In this Demonstration, the price of chooser options is explored, as well as the derivative of the value function  with respect to the various input parameters (the "greeks"): delta,

with respect to the various input parameters (the "greeks"): delta,  ; gamma,

; gamma,  ; theta,

; theta,  ; rho,

; rho,  ; and vega,

; and vega,  . For convenience, we assume zero dividends.

. For convenience, we assume zero dividends.

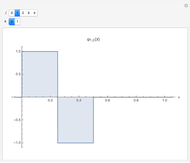

Snapshot 1: the "delta" of a chooser option can be either positive or negative, depending on whether the put or call is more valuable.

Snapshot 2: as  tends , the "gamma" of a chooser option becomes very large for a spot price close to the strike (i.e. "at the money"). This is because at , the chooser option will become either a put or call option, which will have roughly opposite deltas at the money. Therefore, the delta of the chooser option will tend to change very quickly around , and hence gamma is large.

tends , the "gamma" of a chooser option becomes very large for a spot price close to the strike (i.e. "at the money"). This is because at , the chooser option will become either a put or call option, which will have roughly opposite deltas at the money. Therefore, the delta of the chooser option will tend to change very quickly around , and hence gamma is large.

J. C. Hull, Options, Futures, and Other Derivatives, New Jersey: Prentice Hall, 2006.

E. G. Haug, The Complete Guide to Option Pricing Formulas, 2nd ed., New York: McGraw-Hill, 2007.

Permanent Citation

Options: Time Value

Options: Time Value

Peter Falloon Pricing Power Options in the Black-Scholes Model

Pricing Power Options in the Black-Scholes Model

Peter Falloon Basic Option Trading Strategies

Basic Option Trading Strategies

Peter Falloon Options Board Using Black-Scholes Prices

Options Board Using Black-Scholes Prices

Peter Falloon Barrier Option Pricing within the Black-Scholes Model

Barrier Option Pricing within the Black-Scholes Model

Peter Falloon Option Prices in Merton's Jump Diffusion Model

Option Prices in Merton's Jump Diffusion Model

Peter Falloon Real Options

Real Options

Roger J. Brown American Call and Put Option

American Call and Put Option

Andrzej Kozlowski Distribution of Returns from Merton's Jump Diffusion Model

Distribution of Returns from Merton's Jump Diffusion Model

Peter Falloon Implied Volatility in Merton's Jump Diffusion Model

Implied Volatility in Merton's Jump Diffusion Model

Peter Falloon

-

Option Prices in Merton's Jump Diffusion Model

Peter Falloon -

Chooser Options

Chooser Options

Peter Falloon -

Binary Options: Pricing and Greeks

Binary Options: Pricing and Greeks

Peter Falloon -

Angular Spheroidal Functions as a Function of Spheroidicity

Angular Spheroidal Functions as a Function of Spheroidicity

Peter Falloon -

Hyperbolic Distribution

Hyperbolic Distribution

Peter Falloon -

Variance-Gamma Distribution

Variance-Gamma Distribution

Peter Falloon -

Options Board Using Black-Scholes Prices

Peter Falloon -

Properties of a Simple Random Walk with Boundaries

Properties of a Simple Random Walk with Boundaries

Peter Falloon -

Visualizing Superellipses

Visualizing Superellipses

Peter Falloon -

Haar Functions

Haar Functions

Peter Falloon -

Barrier Option Pricing within the Black-Scholes Model

Peter Falloon -

Clebsch-Gordan Coefficients

Clebsch-Gordan Coefficients

Peter Falloon -

Constant Coordinate Curves for Elliptic Coordinates

Constant Coordinate Curves for Elliptic Coordinates

Peter Falloon -

Chi-Squared Distribution and the Central Limit Theorem

Chi-Squared Distribution and the Central Limit Theorem

Peter Falloon -

Multiple Slit Diffraction Pattern

Multiple Slit Diffraction Pattern

Peter Falloon -

Constant Coordinate Curves for Parabolic and Polar Coordinates

Constant Coordinate Curves for Parabolic and Polar Coordinates

Peter Falloon -

Distribution of Returns from Merton's Jump Diffusion Model

Peter Falloon -

Pricing Power Options in the Black-Scholes Model

Peter Falloon -

Implied Volatility in Merton's Jump Diffusion Model

Peter Falloon -

Game Clock

Game Clock

Peter Falloon