American Call and Put Option

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

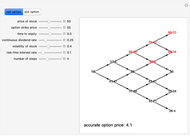

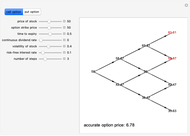

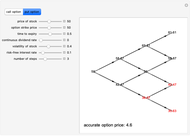

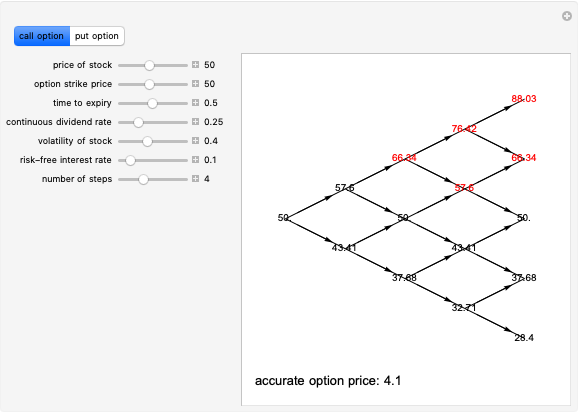

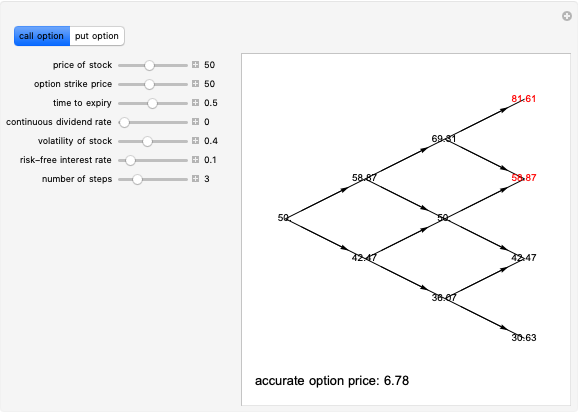

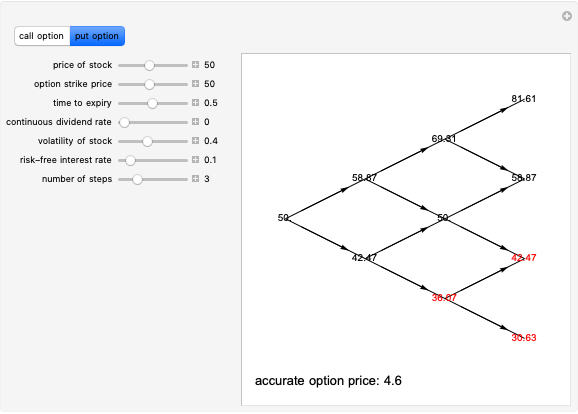

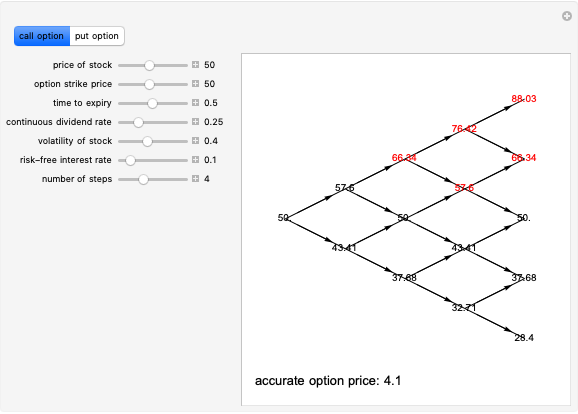

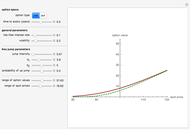

This illustrates the Cox–Ross–Rubenstein binomial tree method of computing the value of a standard American call and put option. Values at the tree nodes show the stock price. Red denotes nodes where it is optimal to exercise the option. A more accurate option value (using 100 time steps) is shown in the bottom left corner.

[more]

Contributed by: Andrzej Kozlowski (March 2011)

Open content licensed under CC BY-NC-SA

Snapshots

Details

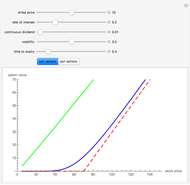

A call option on an asset (usually stock) gives its holder the right to buy the asset at a prescribed price at or before the time of expiry of the option. A put option on an asset gives its holder the right to sell the asset at a prescribed price at or before the time of expiry of the option. A European option (call or put) can be exercised only at the time of expiry; an American option can be exercised on or before the time of expiry. In the case of European options, under the assumption that the stock price process is an exponential Brownian motion with drift, there is a famous explicit formula (the Black–Scholes formula) that gives the value of the option in terms of several parameters. In the case of American options there is no such explicit formula and numerical methods have to be used. One of the most popular is the lattice or "binomial tree" method, as shown here. This method, due to Cox–Ross–Rubenstein, uses a random walk approximation to the Black–Scholes model of stock price motion. For each moment in time and each stock price, the stock price can go either up or down by a certain amount and with a certain probability. The possible values of the stock price are shown at the nodes of the binomial tree, representing the random walk performed by the stock price. The value of the option at this particular node is shown when the pointer is moved to this node. Red-colored nodes represent situations when it is optimal to exercise the option early rather than wait until expiration. Red-colored nodes at expiry mean that the option expires with positive value.

Note that it is customary to measure time to expiry in years, which means that in general, if the volatility is set to, say, 0.4, that means that the random variable  has standard deviation 0.4, where

has standard deviation 0.4, where  is the initial value of stock and

is the initial value of stock and  the value at the end of the first year.

the value at the end of the first year.

Note also that it is well known that for an American call option with no dividend, exercise before expiry is never optimal. This means that the value of an American call with zero dividend is the same as that of the European call with the same parameters. Thus the accuracy of the model can be estimated by comparing these values with those obtained from the Black–Scholes formula. For more details see J. C. Hull, Options, Futures and Other Derivatives,  ed., Upper Saddle River, NJ: Prentice Hall, 2003 pp. 392–406.

ed., Upper Saddle River, NJ: Prentice Hall, 2003 pp. 392–406.

The author is grateful to Michael Trott for help with the interface.

Permanent Citation

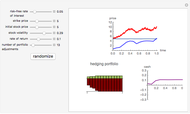

Hedging the European Put Option

Hedging the European Put Option

Andrzej Kozlowski Hedging the Black-Scholes Call Option

Hedging the Black-Scholes Call Option

Andrzej Kozlowski The Price of a Call Option on Electrical Power

The Price of a Call Option on Electrical Power

Andrzej Kozlowski Standard American and European Options

Standard American and European Options

Andrzej Kozlowski Early Exercise of American Options

Early Exercise of American Options

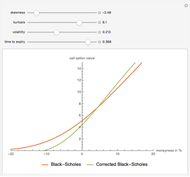

Andrzej Kozlowski The Black-Scholes European Call Option Formula Corrected Using the Gram-Charlier Expansion

The Black-Scholes European Call Option Formula Corrected Using the Gram-Charlier Expansion

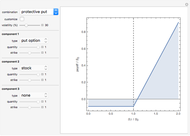

Andrzej Kozlowski Basic Option Trading Strategies

Basic Option Trading Strategies

Peter Falloon The Russian Option: Reduced Regret

The Russian Option: Reduced Regret

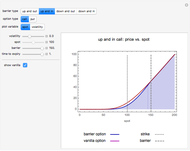

Andrzej Kozlowski Barrier Option Pricing within the Black-Scholes Model

Barrier Option Pricing within the Black-Scholes Model

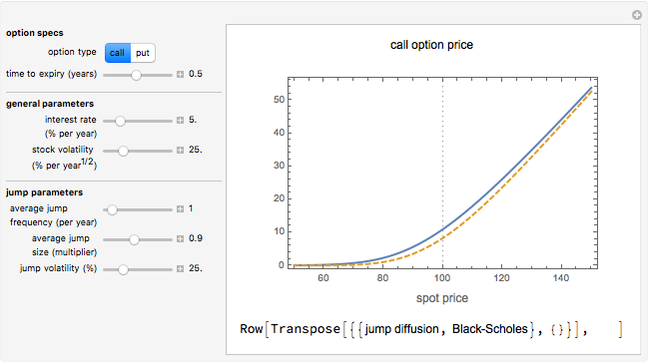

Peter Falloon Option Prices in Merton's Jump Diffusion Model

Option Prices in Merton's Jump Diffusion Model

Peter Falloon

-

American Call and Put Option

American Call and Put Option

Andrzej Kozlowski -

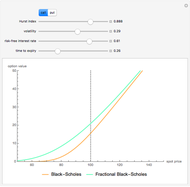

Option Prices under the Fractional Black-Scholes Model

Option Prices under the Fractional Black-Scholes Model

Andrzej Kozlowski -

The Variance Gamma Process

The Variance Gamma Process

Andrzej Kozlowski -

The Black-Scholes European Call Option Formula Corrected Using the Gram-Charlier Expansion

Andrzej Kozlowski -

Option Prices in the Kou Jump Diffusion Model

Option Prices in the Kou Jump Diffusion Model

Andrzej Kozlowski -

The Polar and Bipolar of a Convex Polytope

The Polar and Bipolar of a Convex Polytope

Andrzej Kozlowski -

Two Jump Diffusion Processes

Two Jump Diffusion Processes

Andrzej Kozlowski -

The Vieta Mapping for the Coxeter Group A_2

The Vieta Mapping for the Coxeter Group A_2

Andrzej Kozlowski -

The Bifurcation Set of the Space of Smooth Real Functions

The Bifurcation Set of the Space of Smooth Real Functions

Andrzej Kozlowski -

The Swallowtail Singularity

The Swallowtail Singularity

Andrzej Kozlowski -

Singularities of an Ellipsoidal Wave Front

Singularities of an Ellipsoidal Wave Front

Andrzej Kozlowski -

Nonuniqueness of Option Pricing Under the Meixner Model

Nonuniqueness of Option Pricing Under the Meixner Model

Andrzej Kozlowski -

Coin Machine

Coin Machine

Andrzej Kozlowski -

A Mean-Reverting Jump Diffusion Process

A Mean-Reverting Jump Diffusion Process

Andrzej Kozlowski -

Standard American and European Options

Andrzej Kozlowski -

Density of the Kou Jump Diffusion Process

Density of the Kou Jump Diffusion Process

Andrzej Kozlowski -

The Meixner Process

The Meixner Process

Andrzej Kozlowski -

Fitting the Meixner Distribution to S&P 500 Returns

Fitting the Meixner Distribution to S&P 500 Returns

Andrzej Kozlowski -

Simple Graphs and Their Binomial Edge Ideals

Simple Graphs and Their Binomial Edge Ideals

Andrzej Kozlowski -

The Eneström-Kakeya Bounds for Roots of a Polynomial with Positive Coefficients

The Eneström-Kakeya Bounds for Roots of a Polynomial with Positive Coefficients

Andrzej Kozlowski