Current versus Cohort Life Tables and the Regulation of Life Insurance

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

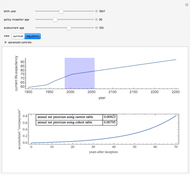

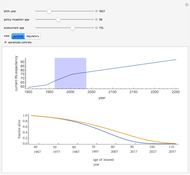

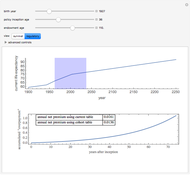

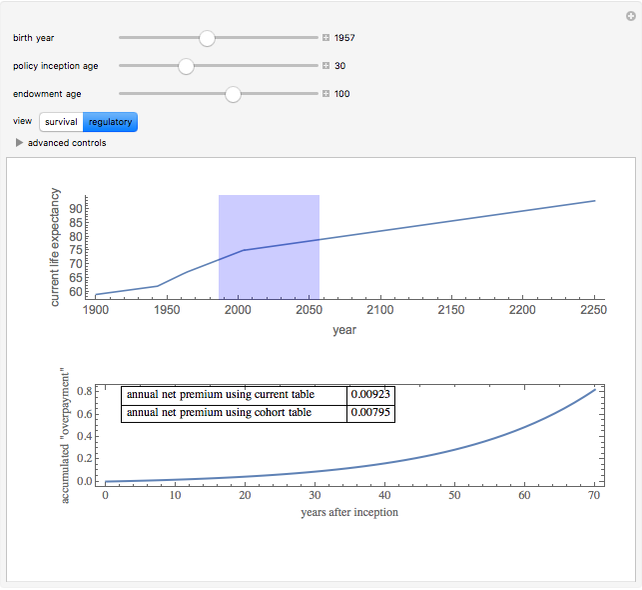

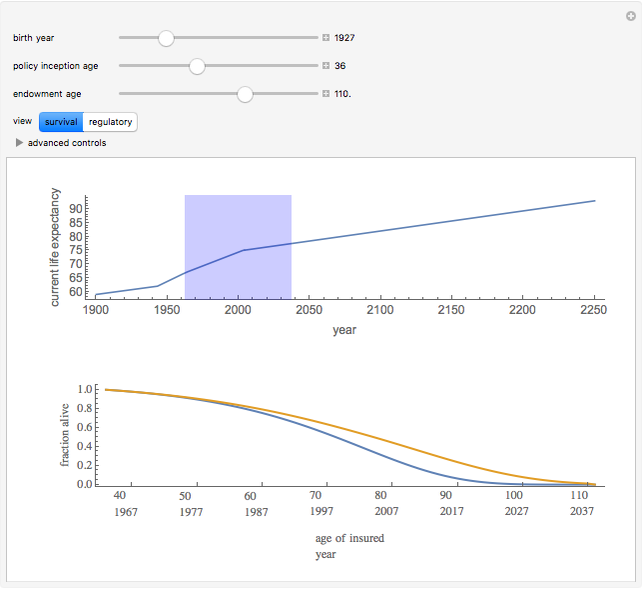

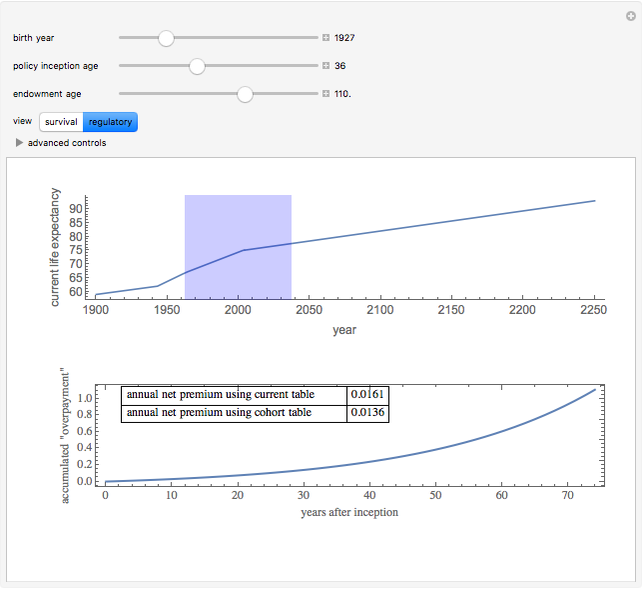

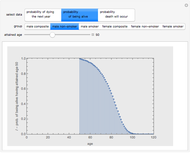

Mortality tables generally used in life insurance regulation and many life insurance computations are what are called "current tables": they show the rates of death for each age at some point in time, such as 1980 or 2003. Individuals do not go through their lives, however, as if it were always 1980 or 2003. Thus, an individual born in 1957 dies at the rate for 53-year-olds set forth by 2010 current mortality tables, dies at the rate for 63-year-olds set forth by 2020 current mortality tables, and dies at the rate for 73-year-olds set forth by 2030 current mortality tables. The death rates that this individual thus experiences can be recapitulated in what is known as a "cohort life table."

[more]

Contributed by: Seth J. Chandler (March 2011)

Open content licensed under CC BY-NC-SA

Snapshots

Details

So long as life expectancy increases over time, the premiums derived using a current table will be higher than those using a cohort table. Insurers adopt different contractual rules and policies within constraints provided by regulations regarding how the difference between the accumulated premiums that result is allocated among insurer and insureds. The insurer, for example, may pay a dividend to insureds to compensate them for mortality better than that predicted by current tables.

This Demonstration assumes a two-parameter Gompertz–Makeham hazard function in which the second parameter remains constant and life expectancy is changed through alteration of the first parameter. You can change the second parameter of the distribution with the advanced controls. A second advanced control lets you change the interest rate used by the insurer in computing premiums and the future value of the difference between premiums under a cohort life table and a current life table.

To permit free movement of the locators but ensure the amount of data necessary to perform the computations required by this Demonstration, you are barred from having fewer than two locators, and it is additionally assumed that life expectancy was 30 in the year 0 and will be 100 in the year 5000.

For simplicity, it is assumed that policies incept on January 1st of each year. Nothing material would change in the outputs of this Demonstration were this assumption relaxed.

A true cohort life table cannot be fully constructed until all the persons born in some cohort die.

An excellent treatment of the mathematics of life insurance, including the "commutation functions" used in the code for this Demonstration, may be found in H. U. Gerber, Life Insurance Mathematics, 3rd ed., New York: Springer, 1997.

Life Insurance Pricing

Life Insurance Pricing

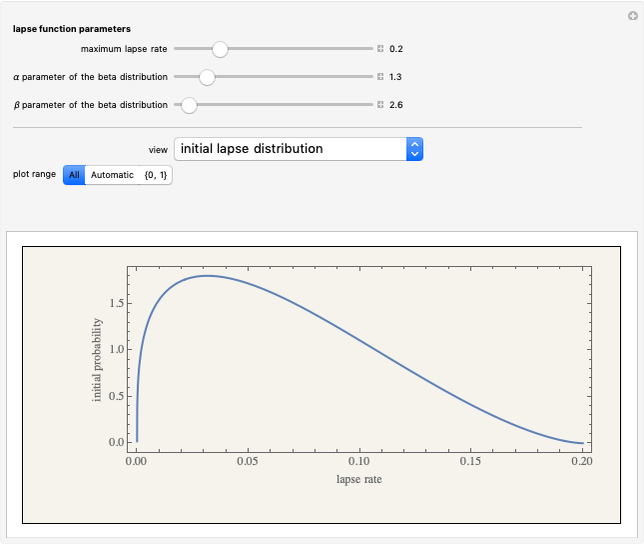

Seth J. Chandler A Conceptual Model of Lapse Financed Life Insurance

A Conceptual Model of Lapse Financed Life Insurance

Seth J. Chandler The 2001 CSO Mortality Tables

The 2001 CSO Mortality Tables

Seth J. Chandler Insurance Disclosures

Insurance Disclosures

Seth J. Chandler A Theory of Insurance Lapses

A Theory of Insurance Lapses

Seth J. Chandler Efficient Single Limit Liability Insurance

Efficient Single Limit Liability Insurance

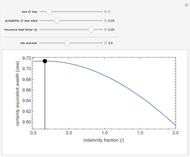

Seth J. Chandler Risk Aversion, Load, and Optimal Insurance

Risk Aversion, Load, and Optimal Insurance

Seth J. Chandler Coordination of Insurance Policies

Coordination of Insurance Policies

Seth J. Chandler Employer Health Insurance Choices under H.R.3590 and H.R.3962

Employer Health Insurance Choices under H.R.3590 and H.R.3962

Seth J. Chandler Individual Insurance Decisions under HR 3560 and HR 3962

Individual Insurance Decisions under HR 3560 and HR 3962

Seth J. Chandler

-

Post-Event Bonding

Post-Event Bonding

Seth J. Chandler -

Emulating Land Use Evolution with a Cellular Automaton

Emulating Land Use Evolution with a Cellular Automaton

Seth J. Chandler -

General Assembly Resolution Viewer

General Assembly Resolution Viewer

Seth J. Chandler -

Random Acyclic Networks

Random Acyclic Networks

Seth J. Chandler -

A Theory of Insurance Lapses

Seth J. Chandler -

Asylum in the United States

Asylum in the United States

Seth J. Chandler -

Property Coinsurance

Property Coinsurance

Seth J. Chandler -

The Persuasion Effect: A Traditional Two-Stage Jury Model

The Persuasion Effect: A Traditional Two-Stage Jury Model

Seth J. Chandler -

Cellular Automata with Global Control

Cellular Automata with Global Control

Seth J. Chandler -

Sports Seasons Based on Score Distributions

Sports Seasons Based on Score Distributions

Seth J. Chandler -

Evidentiary Uncertainty

Evidentiary Uncertainty

Seth J. Chandler -

Spectral Measures

Spectral Measures

Seth J. Chandler -

The Banzhaf Power Index of States for Presidential Candidates

The Banzhaf Power Index of States for Presidential Candidates

Seth J. Chandler -

Liability Insurance Desirability under Lognormal Loss Distributions

Liability Insurance Desirability under Lognormal Loss Distributions

Seth J. Chandler -

The Effects of Coinsurance and Deductibles on Optimal Precautions for Weibull-Distributed Loss

The Effects of Coinsurance and Deductibles on Optimal Precautions for Weibull-Distributed Loss

Seth J. Chandler -

Collocation by Chi Square

Collocation by Chi Square

Seth J. Chandler -

The Present Value of Future Gas Use

The Present Value of Future Gas Use

Seth J. Chandler -

Visualizing Legal Rules: A Homicide Case

Visualizing Legal Rules: A Homicide Case

Seth J. Chandler -

Communities of Nations Bridged by Language Similarity

Communities of Nations Bridged by Language Similarity

Seth J. Chandler