Estimating Loss Functions Using Exceedance Data and the Method of Moments

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

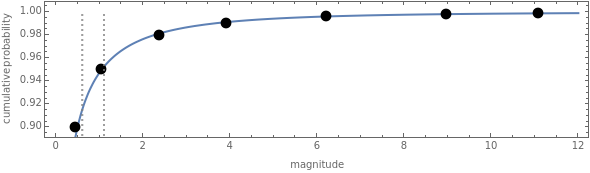

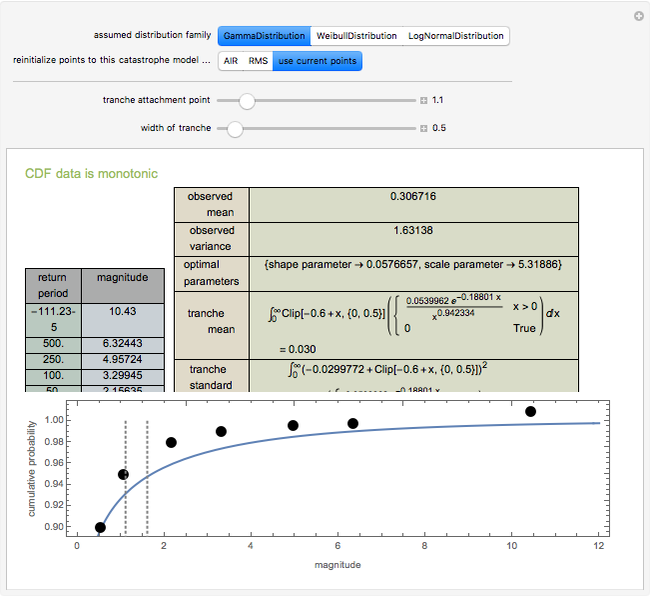

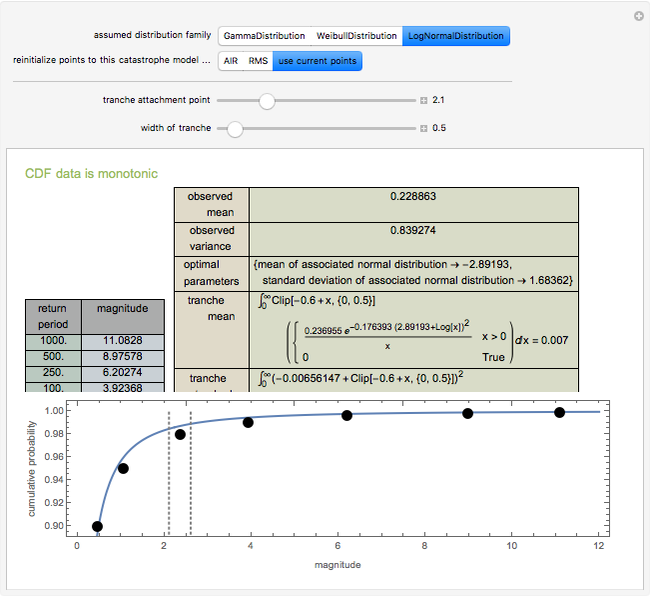

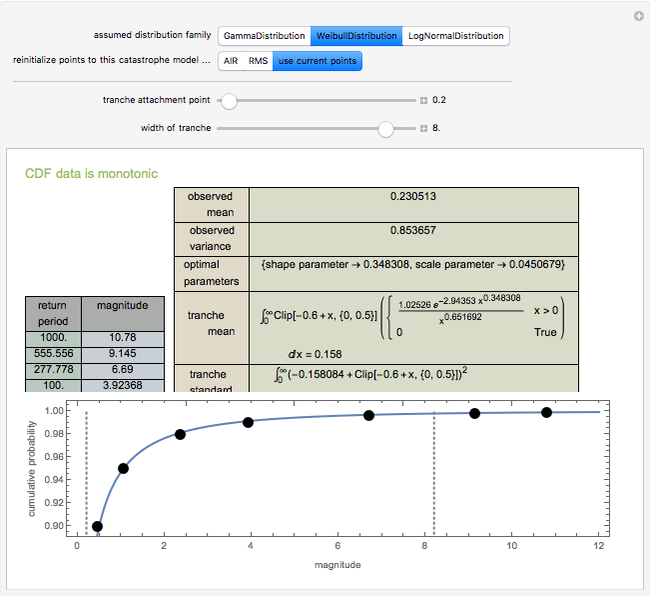

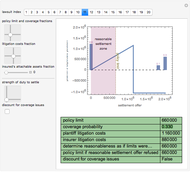

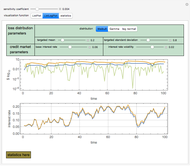

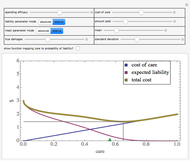

Data regarding the magnitude of catastrophes is often presented in an "exceedance table" that sets forth the number of years it would take for disasters exceeding various magnitudes to occur. This Demonstration shows how one can use exceedance data to generate a two-parameter probability distribution whose first two moments best match those observed from the data. You move locators to set a cumulative density function and determine the family of distributions for which parameters are to be estimated. The Demonstration responds by determining the parameters of that distribution whose first two moments match the observed values. A second part of the Demonstration lets you use the computed probability distribution. You move the sliders to establish a layer (or "tranche", as it is often known) for which an insurer has responsibility. An insurer might, for example, have to pay the difference between the insured's loss and 0.6, with that value clipped between zero and 0.5. In the trade, this would be called a "0.5 XS 0.6 policy". The Demonstration uses the computed probability distribution to determine the expected value and standard deviation of the payments an insurer writing such a tranche would face. These statistics are often relevant to the premium the insurer wishes to charge. A warning is provided if the cumulative density function violates monotonicity or if the algorithm for finding optimal parameters fails. You can also reinitialize the points to correspond with estimates provided by two catastrophe modelers, AIR Worldwide Corporation (AIR) and Risk Management Solutions, Inc. (RMS).

Contributed by: Seth J. Chandler (March 2011)

Open content licensed under CC BY-NC-SA

Snapshots

Details

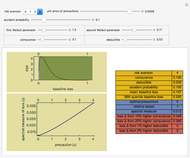

The default data is taken from work submitted by the Texas Windstorm Insurance Association (TWIA) to regulators in 2008 regarding the likely magnitude of insured damages caused by hurricanes striking the Texas coast during the forthcoming 2008-09 hurricane season. The data was originally generated by the catastrophe modeling firms AIR and RMS. All numbers are actually in billions of dollars.

Some research suggests that the premium an insurer will charge should be equal to the expected loss plus a coefficient times the standard deviation of the loss.

The method of moments has the virtue of being extremely fast; it is not, however, a maximum likelihood estimator.

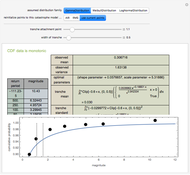

Snapshot 1: fitting the RMS data to a gamma distribution and examining a tranche between 1.1 and 1.6

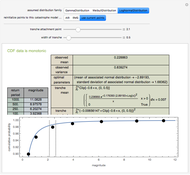

Snapshot 2: fitting the AIR data to a log normal distribution and examining a tranche between 2.1 and 2.6

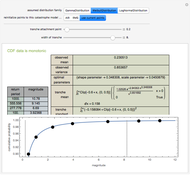

Snapshot 3: fitting user-modified data to a Weibull distribution and examining a large tranche between 0.2 and 8

Snapshot 4: how the system deals with non-monotonic cumulative distribution functions

Estimating Insurance Premiums Using Exceedance Data and the Method of Moments

Estimating Insurance Premiums Using Exceedance Data and the Method of Moments

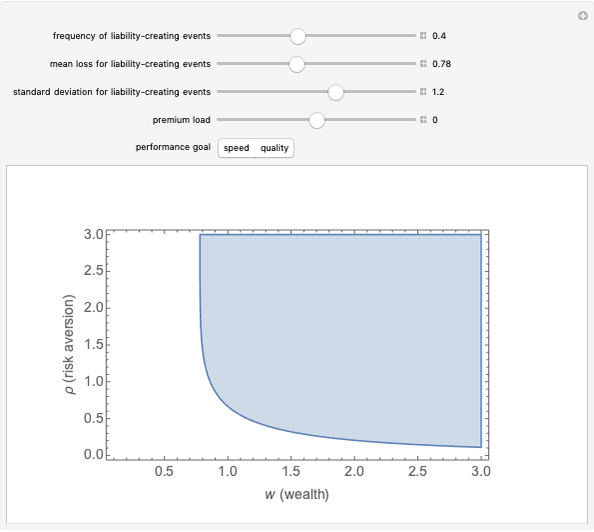

Seth J. Chandler Efficient Single Limit Liability Insurance

Efficient Single Limit Liability Insurance

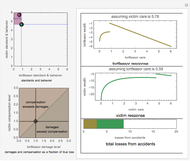

Seth J. Chandler The Duty to Settle

The Duty to Settle

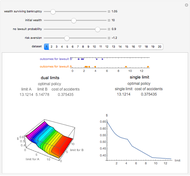

Seth J. Chandler The Efficient Dual-Limit Liability Insurance Contract

The Efficient Dual-Limit Liability Insurance Contract

Seth J. Chandler Property Coinsurance

Property Coinsurance

Seth J. Chandler Moral Hazard

Moral Hazard

Seth J. Chandler Certainty Equivalent Wealth

Certainty Equivalent Wealth

Seth J. Chandler Insurance Disclosures

Insurance Disclosures

Seth J. Chandler Bilateral Accident Model

Bilateral Accident Model

Seth J. Chandler Tax Rates and Tax Revenue

Tax Rates and Tax Revenue

Seth J. Chandler

-

Post-Event Bonding

Post-Event Bonding

Seth J. Chandler -

Emulating Land Use Evolution with a Cellular Automaton

Emulating Land Use Evolution with a Cellular Automaton

Seth J. Chandler -

General Assembly Resolution Viewer

General Assembly Resolution Viewer

Seth J. Chandler -

Random Acyclic Networks

Random Acyclic Networks

Seth J. Chandler -

A Theory of Insurance Lapses

A Theory of Insurance Lapses

Seth J. Chandler -

Asylum in the United States

Asylum in the United States

Seth J. Chandler -

Property Coinsurance

Seth J. Chandler -

The Persuasion Effect: A Traditional Two-Stage Jury Model

The Persuasion Effect: A Traditional Two-Stage Jury Model

Seth J. Chandler -

Cellular Automata with Global Control

Cellular Automata with Global Control

Seth J. Chandler -

Sports Seasons Based on Score Distributions

Sports Seasons Based on Score Distributions

Seth J. Chandler -

Evidentiary Uncertainty

Evidentiary Uncertainty

Seth J. Chandler -

Spectral Measures

Spectral Measures

Seth J. Chandler -

The Banzhaf Power Index of States for Presidential Candidates

The Banzhaf Power Index of States for Presidential Candidates

Seth J. Chandler -

Liability Insurance Desirability under Lognormal Loss Distributions

Liability Insurance Desirability under Lognormal Loss Distributions

Seth J. Chandler -

The Effects of Coinsurance and Deductibles on Optimal Precautions for Weibull-Distributed Loss

The Effects of Coinsurance and Deductibles on Optimal Precautions for Weibull-Distributed Loss

Seth J. Chandler -

Collocation by Chi Square

Collocation by Chi Square

Seth J. Chandler -

The Present Value of Future Gas Use

The Present Value of Future Gas Use

Seth J. Chandler -

Visualizing Legal Rules: A Homicide Case

Visualizing Legal Rules: A Homicide Case

Seth J. Chandler -

Communities of Nations Bridged by Language Similarity

Communities of Nations Bridged by Language Similarity

Seth J. Chandler