Estimating Insurance Premiums Using Exceedance Data and the Method of Moments

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

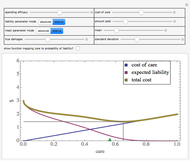

Some experts in finance theorize that the "fair" price for a layer of insurance is a linear combination of (1) the expected losses of that layer; and (2) the increment to the insurer's standard deviation of losses in its portfolio caused by assumption of that layer of insurance. This Demonstration explores the implications of this theory by letting you set the cumulative density function for some risk, the layer of losses that will be insured, and the linear combination of expected loss and standard deviation of loss that predict the premium.

[more]

Contributed by: Seth J. Chandler (March 2011)

Open content licensed under CC BY-NC-SA

Snapshots

Details

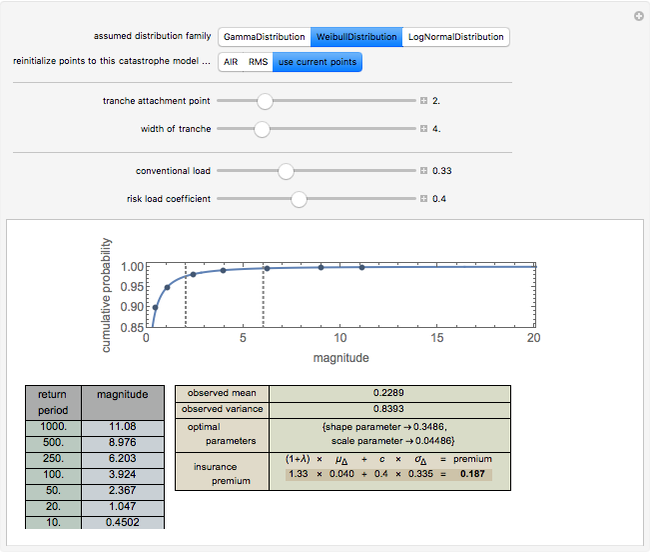

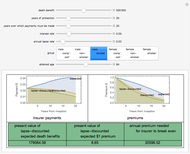

The default data is taken from work submitted by the Texas Windstorm Insurance Association (TWIA) to regulators in 2008 regarding the likely magnitude of insured damages caused by hurricanes striking the Texas coast during the forthcoming 2008-09 hurricane season. The data was originally generated by the catastrophe modeling firms AIR Worldwide Corporation (AIR) and Risk Management Solutions, Inc. (RMS). You can reinitialize the points to correspond with these estimates. All numbers are actually in billions of dollars.

The method of moments has the virtue of being extremely fast; it is not, however, a maximum likelihood estimator.

Snapshot 1: Using the AIR data and a Weibull distribution, conventional load of 0.33, and a risk load of 0.4, the premium for a 4 XS 2 tranche is 0.187.

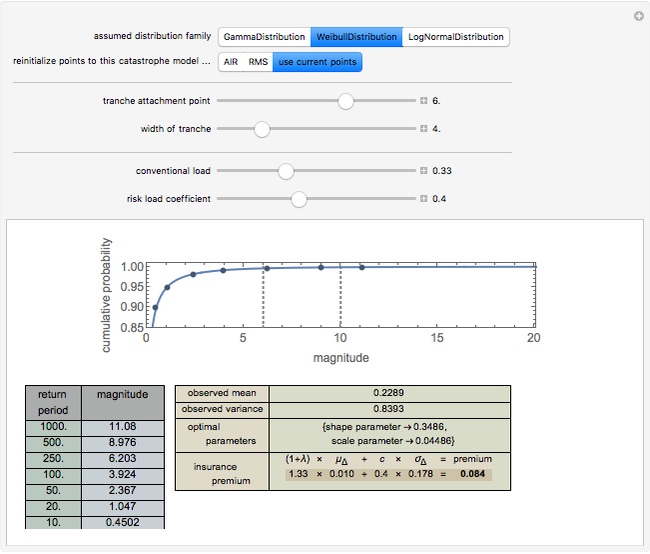

Snapshot 2: Using the AIR data and a Weibull distribution, conventional load of 0.33, and a risk load of 0.4, the premium for a 4 XS 6 tranche is 0.084.

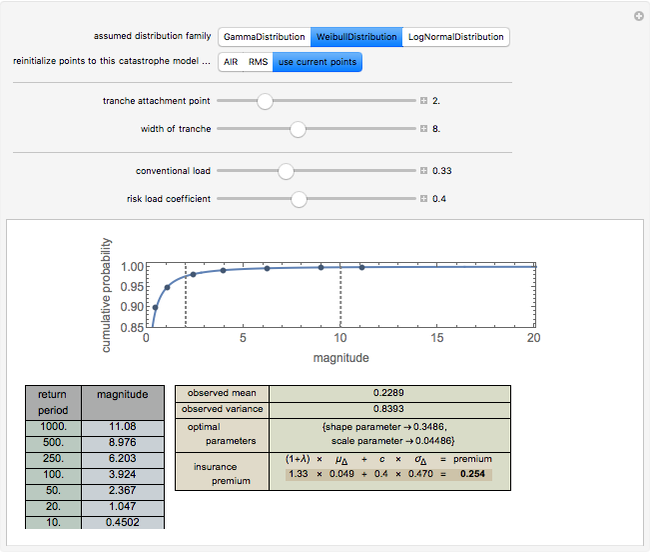

Snapshot 3: Using the AIR data and a Weibull distribution, conventional load of 0.33, and a risk load of 0.4, the premium for an 8 XS 2 tranche is 0.254.

A comparison of snapshot 3 with snapshots 1 and 2 shows that the linear combination model has the "feature" that the premium for a set of layers is not equal to the sum of the premiums for the layers. This distressing failure of "conservation" may be a result of the use of an approximation in this implementation of the model. The original proponents of the model argue that one should use not the standard deviation of the risk but the increment to the standard deviation of a portfolio of risks caused by the assumption of the particular risk. This Demonstration approximates the correct statistic by in effect taking the standard deviation of the particular risk and then multiplying by a lower coefficient. While this approximation probably works tolerably in many settings, it can lead to problematic consequences.

Snapshot 4: Using the RMS data and a Weibull distribution, conventional load of 0.33, and a risk load of 0.4, the premium for an 8 XS 2 tranche is 0.203. The selection of a dataset can thus have a significant effect on estimated premiums.

Snapshot 5: Using the RMS data and a gamma distribution, conventional load of 0.33 and a risk load of 0.4, the premium for an 8 XS 2 tranche is 0.108. The selection of a distribution family can thus have a significant effect on estimated premiums.

Snapshot 6: A non-monotonic cumulative distribution function leads to various error messages.

Estimating Loss Functions Using Exceedance Data and the Method of Moments

Estimating Loss Functions Using Exceedance Data and the Method of Moments

Seth J. Chandler Insurance Disclosures

Insurance Disclosures

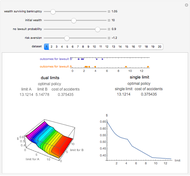

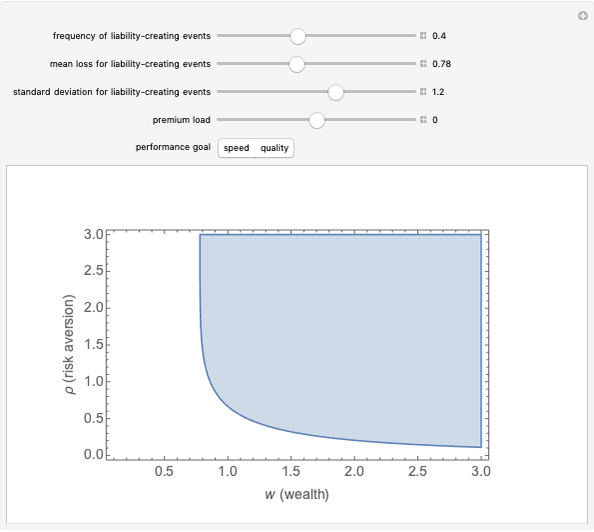

Seth J. Chandler Efficient Single Limit Liability Insurance

Efficient Single Limit Liability Insurance

Seth J. Chandler The Efficient Dual-Limit Liability Insurance Contract

The Efficient Dual-Limit Liability Insurance Contract

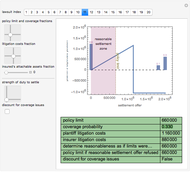

Seth J. Chandler The Duty to Settle

The Duty to Settle

Seth J. Chandler Property Coinsurance

Property Coinsurance

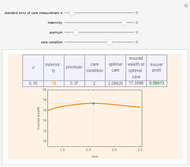

Seth J. Chandler Moral Hazard

Moral Hazard

Seth J. Chandler Certainty Equivalent Wealth

Certainty Equivalent Wealth

Seth J. Chandler Life Insurance Pricing

Life Insurance Pricing

Seth J. Chandler Coordination of Insurance Policies

Coordination of Insurance Policies

Seth J. Chandler

-

Post-Event Bonding

Post-Event Bonding

Seth J. Chandler -

Emulating Land Use Evolution with a Cellular Automaton

Emulating Land Use Evolution with a Cellular Automaton

Seth J. Chandler -

General Assembly Resolution Viewer

General Assembly Resolution Viewer

Seth J. Chandler -

Random Acyclic Networks

Random Acyclic Networks

Seth J. Chandler -

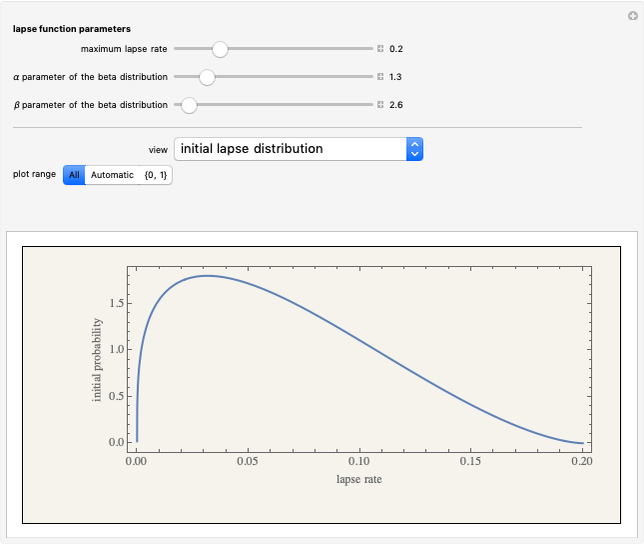

A Theory of Insurance Lapses

A Theory of Insurance Lapses

Seth J. Chandler -

Asylum in the United States

Asylum in the United States

Seth J. Chandler -

Property Coinsurance

Seth J. Chandler -

The Persuasion Effect: A Traditional Two-Stage Jury Model

The Persuasion Effect: A Traditional Two-Stage Jury Model

Seth J. Chandler -

Cellular Automata with Global Control

Cellular Automata with Global Control

Seth J. Chandler -

Sports Seasons Based on Score Distributions

Sports Seasons Based on Score Distributions

Seth J. Chandler -

Evidentiary Uncertainty

Evidentiary Uncertainty

Seth J. Chandler -

Spectral Measures

Spectral Measures

Seth J. Chandler -

The Banzhaf Power Index of States for Presidential Candidates

The Banzhaf Power Index of States for Presidential Candidates

Seth J. Chandler -

Liability Insurance Desirability under Lognormal Loss Distributions

Liability Insurance Desirability under Lognormal Loss Distributions

Seth J. Chandler -

The Effects of Coinsurance and Deductibles on Optimal Precautions for Weibull-Distributed Loss

The Effects of Coinsurance and Deductibles on Optimal Precautions for Weibull-Distributed Loss

Seth J. Chandler -

Collocation by Chi Square

Collocation by Chi Square

Seth J. Chandler -

The Present Value of Future Gas Use

The Present Value of Future Gas Use

Seth J. Chandler -

Visualizing Legal Rules: A Homicide Case

Visualizing Legal Rules: A Homicide Case

Seth J. Chandler -

Communities of Nations Bridged by Language Similarity

Communities of Nations Bridged by Language Similarity

Seth J. Chandler