Value at Risk

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

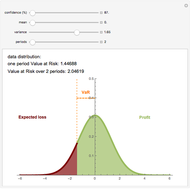

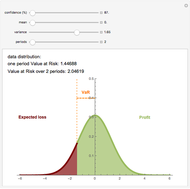

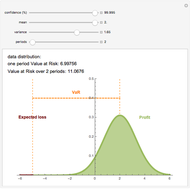

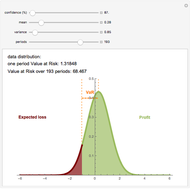

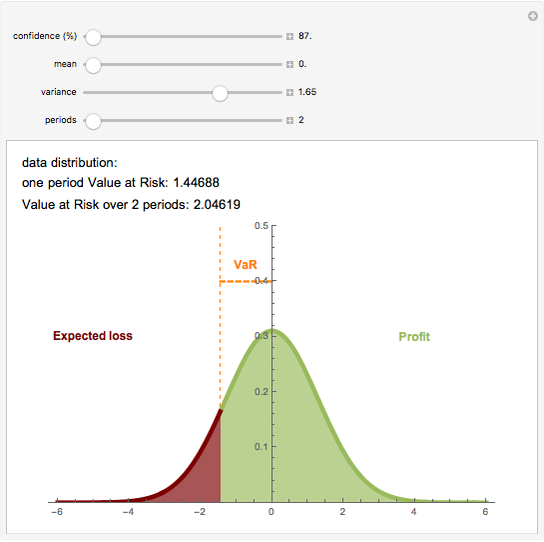

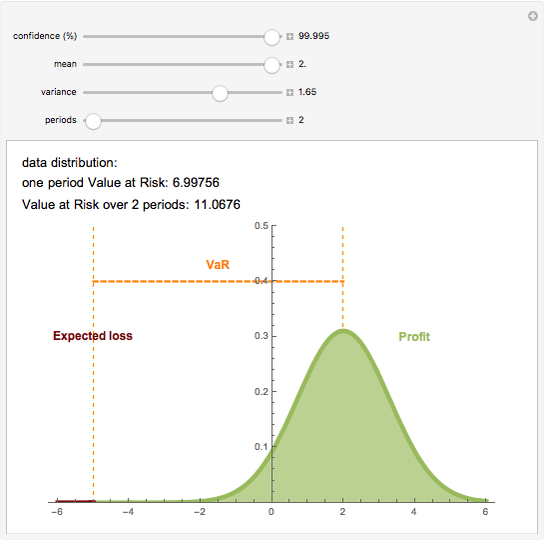

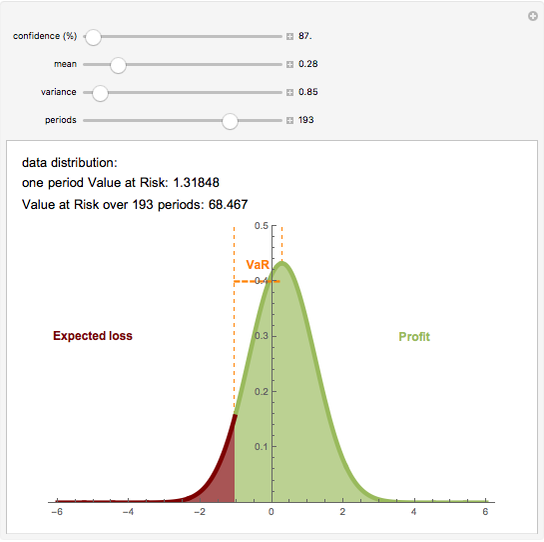

Value at Risk (VaR) and volatility are the most commonly used risk measurements. VaR is easy to calculate and can be used in many fields. VaR is defined as the sum of the data mean and the product of data volatility and an appropriate quantile of  distribution. This quantile indicates the confidence level of the result. This interpretation of VaR assumes that the data is normally distributed; however the calculation works in any setting.

distribution. This quantile indicates the confidence level of the result. This interpretation of VaR assumes that the data is normally distributed; however the calculation works in any setting.

Contributed by: Gergely Nagy (March 2011)

Open content licensed under CC BY-NC-SA

Snapshots

Details

Interpretation of VaR

Suppose the VaR over a one-day holding period is 1000 (the VaR is expressed as an absolute number amount) at a confidence level of 99%. That means that 99% of the time (i.e., 99 out of 100 trading days), a maximum loss of 1000 is expected once and the second largest loss in 100 days is expected to be no more than 1000. For the worst 1% of days the minimum loss of 1000 is expected.

The VaR for a  -long period (e.g. days) is calculated as the product of one period VaR (with mean zero) and

-long period (e.g. days) is calculated as the product of one period VaR (with mean zero) and  , where

, where  is the data mean.

is the data mean.

Permanent Citation

Bootstrapping to Compute Value-at-Risk Standard Errors

Bootstrapping to Compute Value-at-Risk Standard Errors

Jeff Hamrick Risk Premiums

Risk Premiums

John Horton Risk, Ownership, and Control

Risk, Ownership, and Control

Roger J. Brown Constant Risk Aversion Utility Functions

Constant Risk Aversion Utility Functions

Seth J. Chandler Present Value Calculator

Present Value Calculator

Craig Bauling Options: Time Value

Options: Time Value

Peter Falloon Future Value Calculator

Future Value Calculator

Sarah Lichtblau Net Present Value

Net Present Value

Fiona Maclachlan Discounted Present Value

Discounted Present Value

Jason Cawley Expanded Fermi Solution for Risk Assessment

Expanded Fermi Solution for Risk Assessment

Mark D. Normand, Micha Peleg and Joseph Horowitz