Yield, Spot, and Forward Curves

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

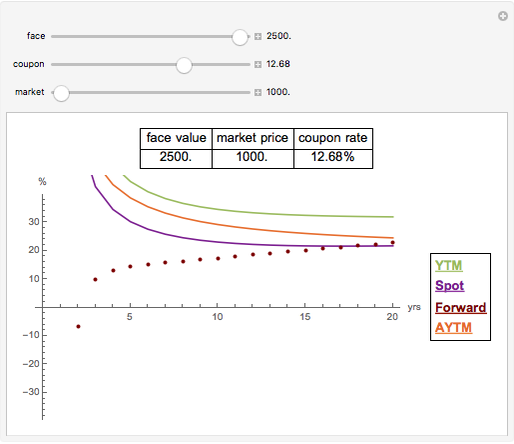

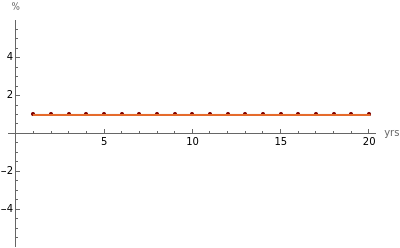

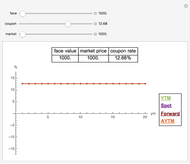

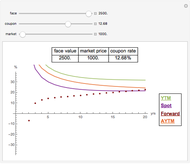

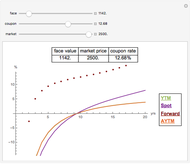

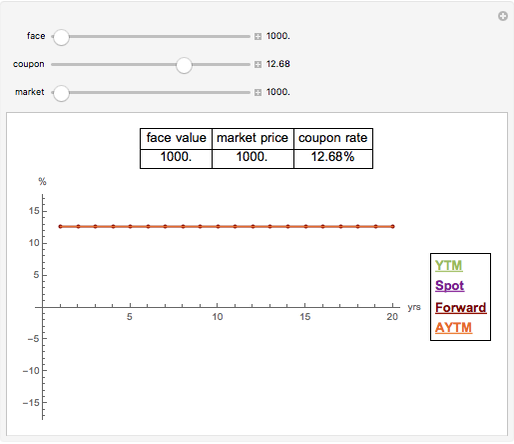

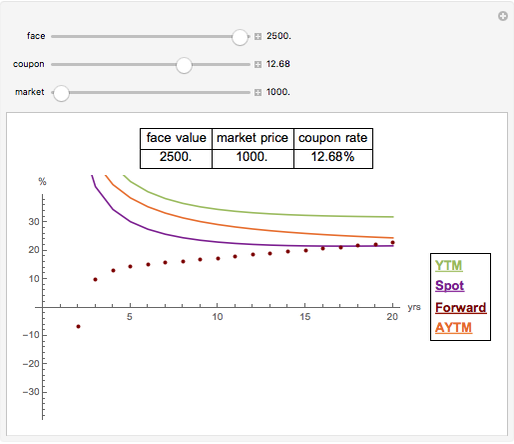

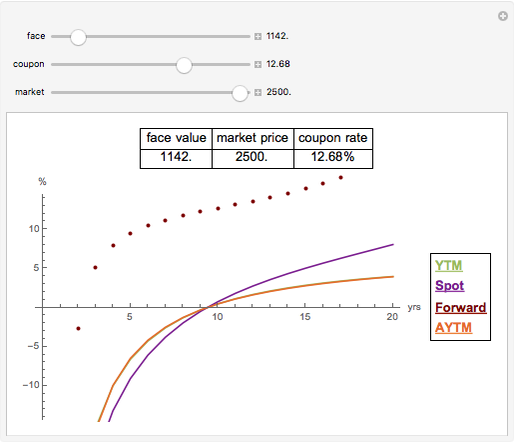

This Demonstration shows the yield, spot, and forward curves for a coupon bond with yearly coupons, purchased for the market price with no other costs and with the face value repaid at the end of the maturity. In addition, it shows the approximate yield to maturity curve, which is also known as Hawawini–Vora yield to maturity.

Contributed by: Gergely Nagy (March 2011)

Open content licensed under CC BY-NC-SA

Snapshots

Details

Snapshot 1: for the bond priced at par, the yield equals the coupon rate

Snapshot 2: for the bond with higher face value than price, the yield curve is decreasing

Snapshot 3: the opposite situation implies an increasing yield curve,

the Hawawini–Vora approximation:

Permanent Citation

"Yield, Spot, and Forward Curves"

http://demonstrations.wolfram.com/YieldSpotAndForwardCurves/

Wolfram Demonstrations Project

Published: March 7 2011

Price-Yield Curve

Price-Yield Curve

Fiona Maclachlan Inflation-Adjusted Yield

Inflation-Adjusted Yield

Roger J. Brown Spotting a Liquidity Trap

Spotting a Liquidity Trap

Samuel G. Chen Revenue and Costs Curves Analysis

Revenue and Costs Curves Analysis

Timur Gareev Short-Run Cost Curves

Short-Run Cost Curves

William J. Polley Short-Run Production and Cost Curves

Short-Run Production and Cost Curves

Tom Creahan Shifts in the Demand Curve

Shifts in the Demand Curve

Sarah Lichtblau No Supply Curve in a Monopolistic Market

No Supply Curve in a Monopolistic Market

Samuel G. Chen Analysis of Cumulative Triangles with the Chain-Ladder Method

Analysis of Cumulative Triangles with the Chain-Ladder Method

Gergely Nagy Net and Gross Reserve of Life Insurance

Net and Gross Reserve of Life Insurance

Gergely Nagy