Three-Asset Efficient Frontier

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

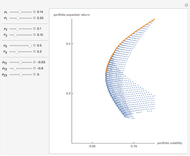

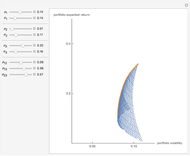

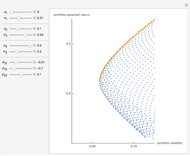

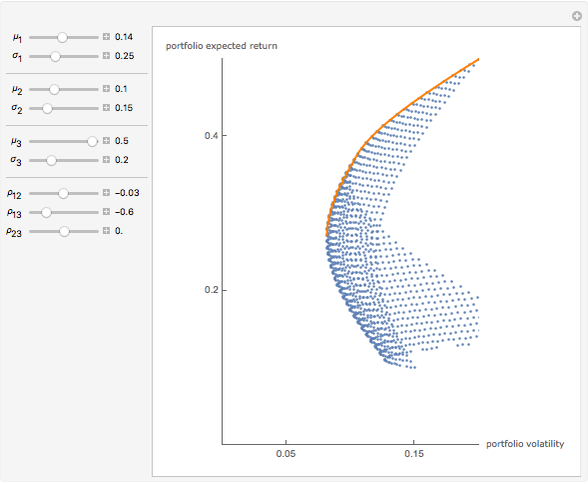

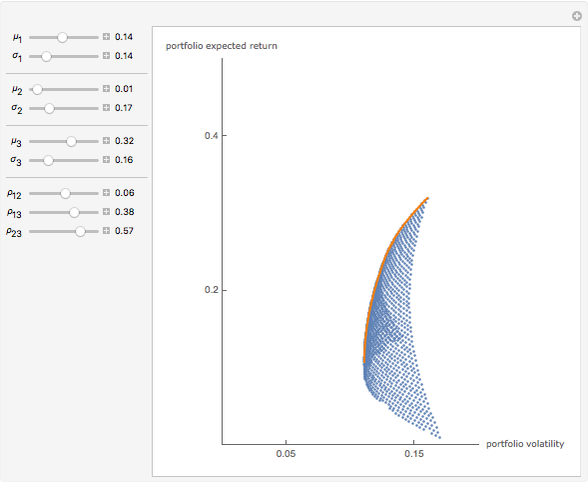

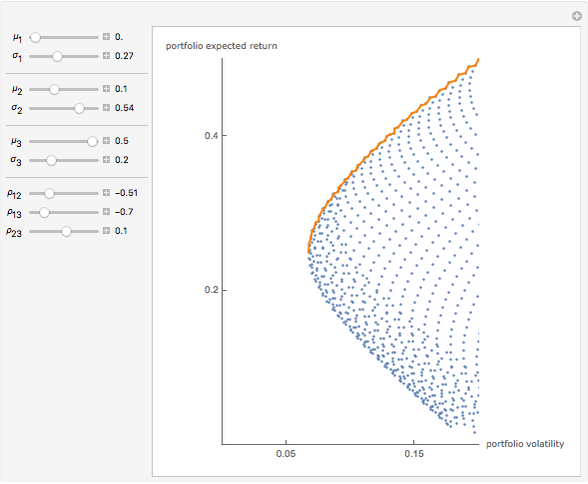

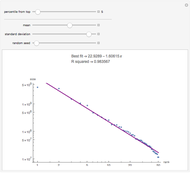

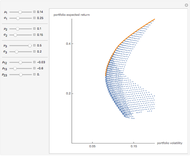

Consider three assets with expected returns  and standard deviations of returns

and standard deviations of returns  ; i = 1, 2, 3. Let the correlation coefficient between asset i and asset j be

; i = 1, 2, 3. Let the correlation coefficient between asset i and asset j be  . Each blue point represents the expected return and the standard deviation of return of a portfolio created by a specific combination of the three assets. The orange line, known as the efficient frontier, sketches out the portfolio combinations such that for any expected return, the volatility (or standard deviation of return) is the lowest; and for any level of volatility, the expected return is the highest.

. Each blue point represents the expected return and the standard deviation of return of a portfolio created by a specific combination of the three assets. The orange line, known as the efficient frontier, sketches out the portfolio combinations such that for any expected return, the volatility (or standard deviation of return) is the lowest; and for any level of volatility, the expected return is the highest.

Contributed by: Fiona Maclachlan (March 2011)

Open content licensed under CC BY-NC-SA

Snapshots

Details

detailSectionParagraphPermanent Citation

"Three-Asset Efficient Frontier"

http://demonstrations.wolfram.com/ThreeAssetEfficientFrontier/

Wolfram Demonstrations Project

Published: March 7 2011

Two-Asset Markowitz Feasible Set

Two-Asset Markowitz Feasible Set

Jim R Larkin Efficient Single Limit Liability Insurance

Efficient Single Limit Liability Insurance

Seth J. Chandler The Efficient Dual-Limit Liability Insurance Contract

The Efficient Dual-Limit Liability Insurance Contract

Seth J. Chandler Constant Risk Aversion Utility Functions

Constant Risk Aversion Utility Functions

Seth J. Chandler Profit Maximization in Perfect Competition

Profit Maximization in Perfect Competition

Fiona Maclachlan Macaulay Duration

Macaulay Duration

Fiona Maclachlan Gains from Trade

Gains from Trade

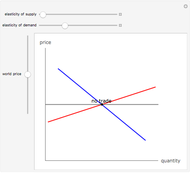

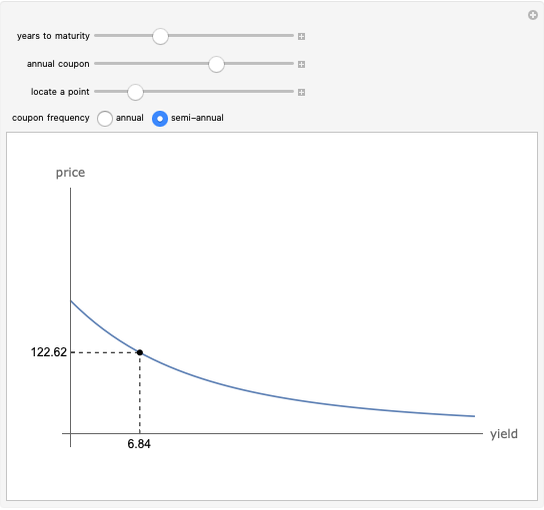

Fiona Maclachlan Price-Yield Curve

Price-Yield Curve

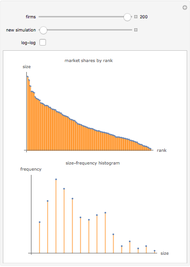

Fiona Maclachlan A Model of Market Shares II

A Model of Market Shares II

Fiona Maclachlan A Model of Market Shares I

A Model of Market Shares I

Fiona Maclachlan

-

Zipf's Law for U.S. Cities

Zipf's Law for U.S. Cities

Fiona Maclachlan -

How Continuous Innovation Affects Supply, Producer Surplus, and Consumer Surplus

How Continuous Innovation Affects Supply, Producer Surplus, and Consumer Surplus

Fiona Maclachlan -

Monopoly Model

Monopoly Model

Fiona Maclachlan -

Competitive Model

Competitive Model

Fiona Maclachlan -

Simple Solow Model

Simple Solow Model

Fiona Maclachlan -

Zipf's Law for Cities

Zipf's Law for Cities

Fiona Maclachlan -

Money Supply Process

Money Supply Process

Fiona Maclachlan -

A Model of Market Shares I

Fiona Maclachlan -

Macaulay Duration

Fiona Maclachlan -

Gains from Trade

Fiona Maclachlan -

Broken Stick Rule

Broken Stick Rule

Fiona Maclachlan -

Amortized Loan Interest and Principal

Amortized Loan Interest and Principal

Fiona Maclachlan -

Interest Rate Swap

Interest Rate Swap

Fiona Maclachlan -

Elasticity, Total Revenue, and the Linear Demand Curve

Elasticity, Total Revenue, and the Linear Demand Curve

Fiona Maclachlan -

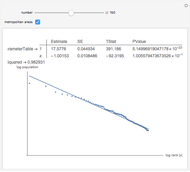

Power Law Tails in Log Normal Data

Power Law Tails in Log Normal Data

Fiona Maclachlan -

Concentric Circles

Concentric Circles

Fiona Maclachlan -

Long-Run Average Total Cost

Long-Run Average Total Cost

Fiona Maclachlan -

Purchasing Power Calculator

Purchasing Power Calculator

Fiona Maclachlan -

Three-Asset Efficient Frontier

Three-Asset Efficient Frontier

Fiona Maclachlan -

Beta Distribution

Beta Distribution

Fiona Maclachlan