Efficient Single Limit Liability Insurance

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

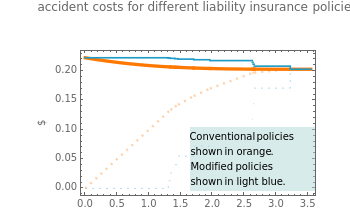

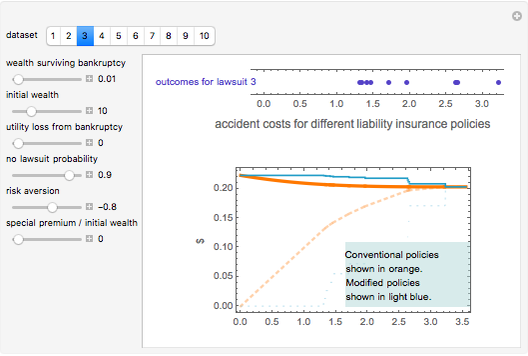

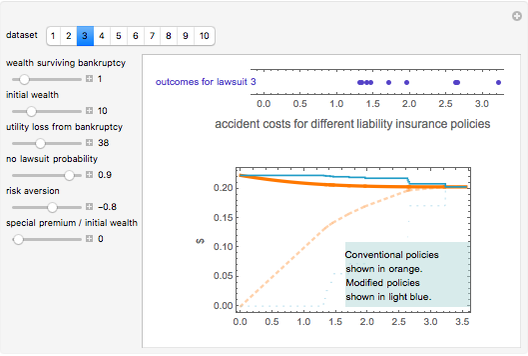

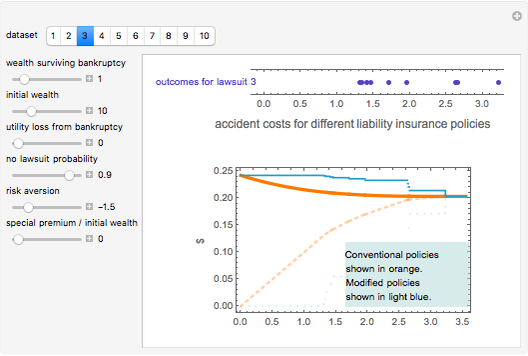

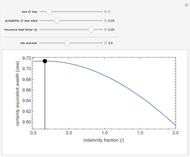

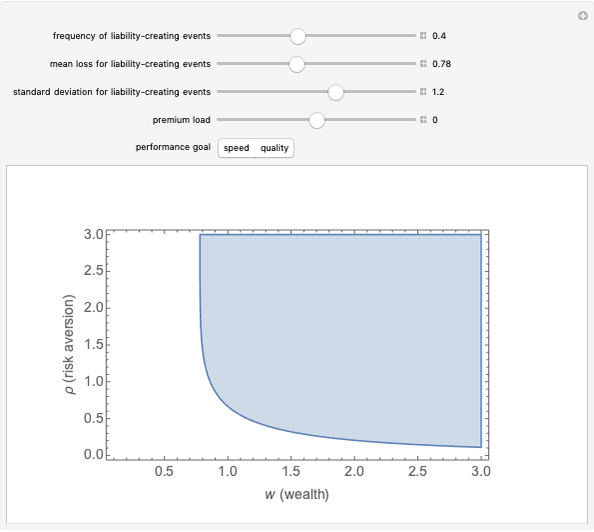

In a conventional liability insurance policy, the insurer pays a victim the lesser of (a) the damages assessed in a covered lawsuit and (b) a "per occurrence limit." If it were lawful to do so, you could write a modified liability insurance policy; however, in which the insurer would pay the victim the damages assessed in a covered lawsuit unless those damages exceeded some limit, in which event the insurer would pay the victim nothing and the insured would pay the insurer an additional special premium. This Demonstration examines premiums in a competitive market and the expected accident costs (premiums + monetized residual risk). The premiums are shown as dashed lines and the expected accident costs are shown as solid lines. As can be seen, the modified insurance policy will frequently be more advantageous to the insured, although it may be an unlawful insurance policy. The user can choose from among 10 different datasets regarding potential lawsuits and can select the wealth that the insured will be left with if it is bankrupted, any additional utility loss from having been bankrupted, the initial wealth of the insured, the probability that no lawsuit will be filed against the insured, the relative risk aversion of the insured, and the amount of any special premium for modified policies.

Contributed by: Seth J. Chandler (March 2011)

Open content licensed under CC BY-NC-SA

Snapshots

Details

Notwithstanding the suggestion in this Demonstration that, in many settings, the modified liability insurance contract will be superior to the traditional liability insurance contract, many American states have laws that will make such policies difficult to implement. In particular, many states have laws that prohibit the insurer from diminishing the amount it owes to the insured on account of the insured's insolvency; yet it is precisely when the insured would otherwise become insolvent that the insured often wants to have a special premium obligation to its insurer or, at a minimum excuse the insurer from having to pay the victim. This Demonstration thus highlights that these laws, if they make sense at all, are written to protect potential victims and not insureds. Because they result in additional premiums, however, these laws may deter the purchase of liability insurance or diminish the amount of coverage purchased and thus may hurt some potential victims.

Snapshot 1: as the wealth of the insured increases, in general the insured will want higher liability insurance limits

Snapshot 2: as the wealth surviving bankruptcy decreases, in general insureds will want higher liability insurance limits

Snapshot 3: as the utility loss from bankruptcy increases, low levels of insurance become comparatively less attractive

Snapshot 4: as risk aversion grows, the demand for high levels of liability insurance increases

Snapshot 5: increasing the special premium can make modified liability insurance contracts even more attractive

Permanent Citation

"Efficient Single Limit Liability Insurance"

http://demonstrations.wolfram.com/EfficientSingleLimitLiabilityInsurance/

Wolfram Demonstrations Project

Published: March 7 2011

Insurance Disclosures

Insurance Disclosures

Seth J. Chandler The Duty to Settle

The Duty to Settle

Seth J. Chandler Property Coinsurance

Property Coinsurance

Seth J. Chandler Life Insurance Pricing

Life Insurance Pricing

Seth J. Chandler A Conceptual Model of Lapse Financed Life Insurance

A Conceptual Model of Lapse Financed Life Insurance

Seth J. Chandler Coordination of Insurance Policies

Coordination of Insurance Policies

Seth J. Chandler The Efficient Dual-Limit Liability Insurance Contract

The Efficient Dual-Limit Liability Insurance Contract

Seth J. Chandler Adverse Selection

Adverse Selection

Seth J. Chandler The 2001 CSO Mortality Tables

The 2001 CSO Mortality Tables

Seth J. Chandler Risk Aversion, Load, and Optimal Insurance

Risk Aversion, Load, and Optimal Insurance

Seth J. Chandler

-

Post-Event Bonding

Post-Event Bonding

Seth J. Chandler -

Emulating Land Use Evolution with a Cellular Automaton

Emulating Land Use Evolution with a Cellular Automaton

Seth J. Chandler -

General Assembly Resolution Viewer

General Assembly Resolution Viewer

Seth J. Chandler -

Random Acyclic Networks

Random Acyclic Networks

Seth J. Chandler -

A Theory of Insurance Lapses

A Theory of Insurance Lapses

Seth J. Chandler -

Asylum in the United States

Asylum in the United States

Seth J. Chandler -

Property Coinsurance

Seth J. Chandler -

The Persuasion Effect: A Traditional Two-Stage Jury Model

The Persuasion Effect: A Traditional Two-Stage Jury Model

Seth J. Chandler -

Cellular Automata with Global Control

Cellular Automata with Global Control

Seth J. Chandler -

Sports Seasons Based on Score Distributions

Sports Seasons Based on Score Distributions

Seth J. Chandler -

Evidentiary Uncertainty

Evidentiary Uncertainty

Seth J. Chandler -

Spectral Measures

Spectral Measures

Seth J. Chandler -

The Banzhaf Power Index of States for Presidential Candidates

The Banzhaf Power Index of States for Presidential Candidates

Seth J. Chandler -

Liability Insurance Desirability under Lognormal Loss Distributions

Liability Insurance Desirability under Lognormal Loss Distributions

Seth J. Chandler -

The Effects of Coinsurance and Deductibles on Optimal Precautions for Weibull-Distributed Loss

The Effects of Coinsurance and Deductibles on Optimal Precautions for Weibull-Distributed Loss

Seth J. Chandler -

Collocation by Chi Square

Collocation by Chi Square

Seth J. Chandler -

The Present Value of Future Gas Use

The Present Value of Future Gas Use

Seth J. Chandler -

Visualizing Legal Rules: A Homicide Case

Visualizing Legal Rules: A Homicide Case

Seth J. Chandler -

Communities of Nations Bridged by Language Similarity

Communities of Nations Bridged by Language Similarity

Seth J. Chandler