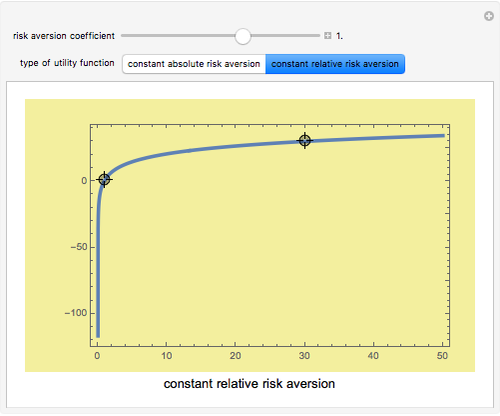

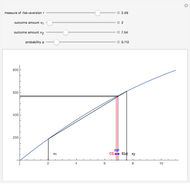

Constant Risk Aversion Utility Functions

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

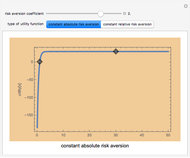

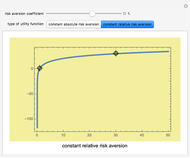

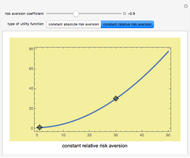

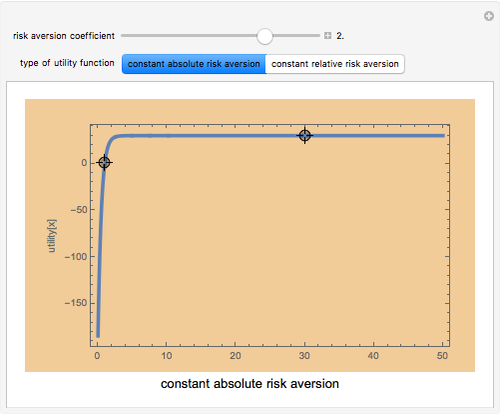

Utility functions are said to exhibit constant risk aversion under the Arrow–Pratt measure if they satisfy a secondâ€Âorder differential equation. You can set a risk aversion coefficient—the higher it is, the more risk averse—as well as the values at two points along the curve; this Demonstration plots the resulting utility function. You can choose between constant absolute risk aversion and constant relative risk aversion. The class of utility functions shown in this Demonstration are frequently used in economic analyses of risk, including finance and insurance.

Contributed by: Seth J. Chandler (March 2011)

Open content licensed under CC BY-NC-SA

Snapshots

Details

Although it appears that the locators are constrained to stay along the original curve, this is not the case: the locators are unconstrained. The fact that the curve does not change its shape is the result of constant risk aversion and the use of the  option.

option.

Snapshot 1: a high level of constant risk aversion results in a rapid flattening of the utility function

Snapshot 2: a logarithmic utility function results when constant relative aversion is set to one

Snapshot 3: a utility function reflecting negative risk aversion

Permanent Citation

"Constant Risk Aversion Utility Functions"

http://demonstrations.wolfram.com/ConstantRiskAversionUtilityFunctions/

Wolfram Demonstrations Project

Published: March 7 2011

Bilateral Accident Model

Bilateral Accident Model

Seth J. Chandler Certainty Equivalent Wealth

Certainty Equivalent Wealth

Seth J. Chandler Moral Hazard

Moral Hazard

Seth J. Chandler Constant Elasticity of Substitution Production

Constant Elasticity of Substitution Production

Kevin Balch and Seth J. Chandler Cobb-Douglas Production Functions

Cobb-Douglas Production Functions

Seth J. Chandler Land Use Regulation and Municipal Utility

Land Use Regulation and Municipal Utility

Roger J. Brown Risk, Ownership, and Control

Risk, Ownership, and Control

Roger J. Brown Risk Premiums

Risk Premiums

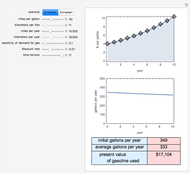

John Horton The Present Value of Future Gas Use

The Present Value of Future Gas Use

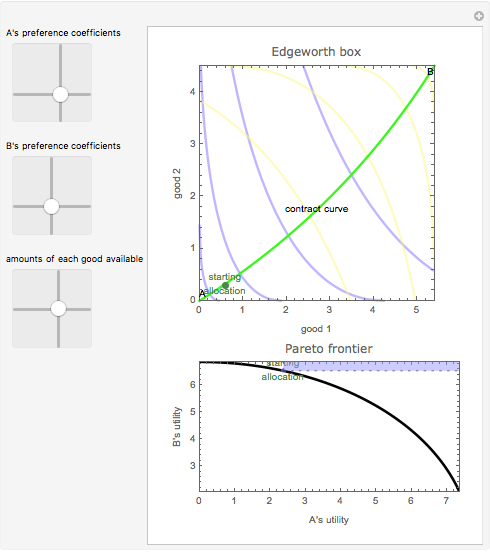

Seth J. Chandler The Edgeworth Box

The Edgeworth Box

Seth J. Chandler

-

Post-Event Bonding

Post-Event Bonding

Seth J. Chandler -

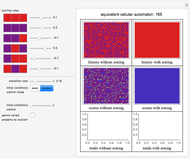

Emulating Land Use Evolution with a Cellular Automaton

Emulating Land Use Evolution with a Cellular Automaton

Seth J. Chandler -

General Assembly Resolution Viewer

General Assembly Resolution Viewer

Seth J. Chandler -

Random Acyclic Networks

Random Acyclic Networks

Seth J. Chandler -

A Theory of Insurance Lapses

A Theory of Insurance Lapses

Seth J. Chandler -

Asylum in the United States

Asylum in the United States

Seth J. Chandler -

Property Coinsurance

Property Coinsurance

Seth J. Chandler -

The Persuasion Effect: A Traditional Two-Stage Jury Model

The Persuasion Effect: A Traditional Two-Stage Jury Model

Seth J. Chandler -

Cellular Automata with Global Control

Cellular Automata with Global Control

Seth J. Chandler -

Sports Seasons Based on Score Distributions

Sports Seasons Based on Score Distributions

Seth J. Chandler -

Evidentiary Uncertainty

Evidentiary Uncertainty

Seth J. Chandler -

Spectral Measures

Spectral Measures

Seth J. Chandler -

The Banzhaf Power Index of States for Presidential Candidates

The Banzhaf Power Index of States for Presidential Candidates

Seth J. Chandler -

Liability Insurance Desirability under Lognormal Loss Distributions

Liability Insurance Desirability under Lognormal Loss Distributions

Seth J. Chandler -

The Effects of Coinsurance and Deductibles on Optimal Precautions for Weibull-Distributed Loss

The Effects of Coinsurance and Deductibles on Optimal Precautions for Weibull-Distributed Loss

Seth J. Chandler -

Collocation by Chi Square

Collocation by Chi Square

Seth J. Chandler -

The Present Value of Future Gas Use

Seth J. Chandler -

Visualizing Legal Rules: A Homicide Case

Visualizing Legal Rules: A Homicide Case

Seth J. Chandler -

Communities of Nations Bridged by Language Similarity

Communities of Nations Bridged by Language Similarity

Seth J. Chandler