Density of the Kou Jump Diffusion Process

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

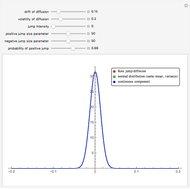

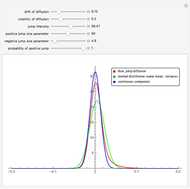

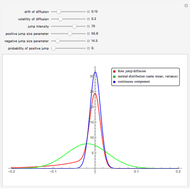

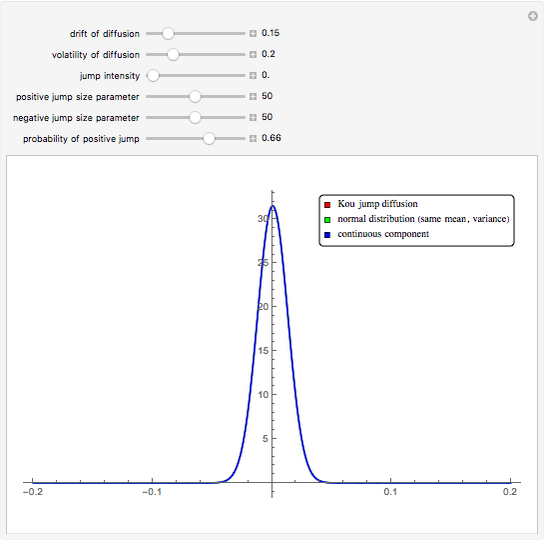

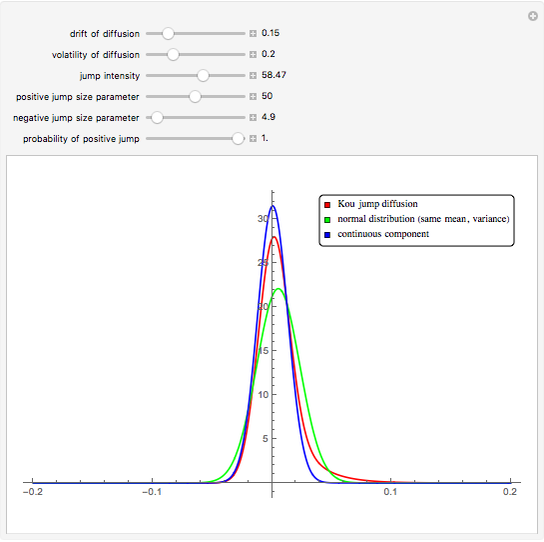

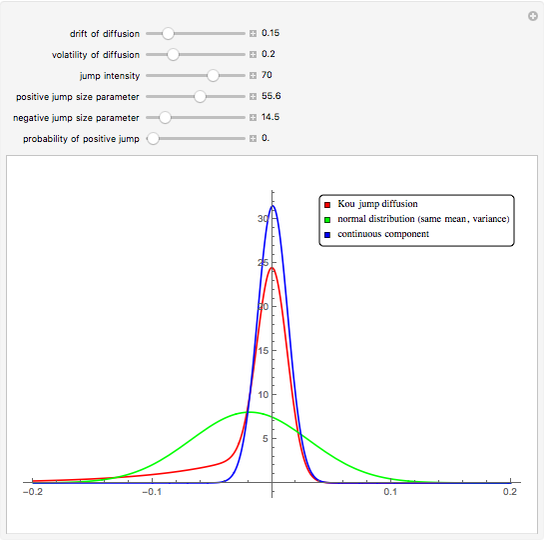

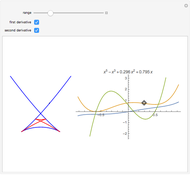

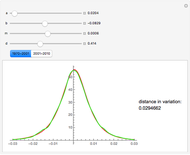

This Demonstration shows a graph of an approximate probability density function of the returns of the Kou jump diffusion process (red) together with the graphs of two closely related normal densities. The blue graph shows the density of the continuous component of the jump diffusion process. The green graph shows the density of the normal distribution with the same mean and standard deviation as the jump diffusion. When the jump intensity parameter is set to 0, all three curves coincide.

Contributed by: Andrzej Kozlowski (February 2012)

Open content licensed under CC BY-NC-SA

Snapshots

Details

The Kou jump diffusion model is one of the most convenient improvements of the classical Black–Scholes model, in which a Lévy process (a jump process with independent increments) is used in place of the standard Wiener process. The Kou model is superior to the Black–Scholes model in fitting historical stock data while being more tractable than rival jump process models for the purpose of option pricing, since for several important types of options explicit formulas can be given for the option price in the Kou model but not in the others (this is due to the "memorylessness" property of the exponential distribution). Unfortunately there is no explicit formula for the probability density function of the Lévy process on which the Kou model is based. As with all Lévy processes, the distribution of values of the process at a given moment in time is infinitely divisible, but in this case it is not closed under convolution. This means that the distribution of returns depends on the time scale over which the data is sampled (i.e. the size of increment  ). When

). When  is small, an approximate formula for the probability density function can be obtained by means of the Taylor expansion. Here we take

is small, an approximate formula for the probability density function can be obtained by means of the Taylor expansion. Here we take  which is small enough for accurate approximation.

which is small enough for accurate approximation.

Reference

[1] S. Kou, "A Jump-Diffusion Model for Option Pricing," Management Science, 48, 2002 pp. 1086–1101.

Permanent Citation

"Density of the Kou Jump Diffusion Process"

http://demonstrations.wolfram.com/DensityOfTheKouJumpDiffusionProcess/

Wolfram Demonstrations Project

Published: February 25 2012

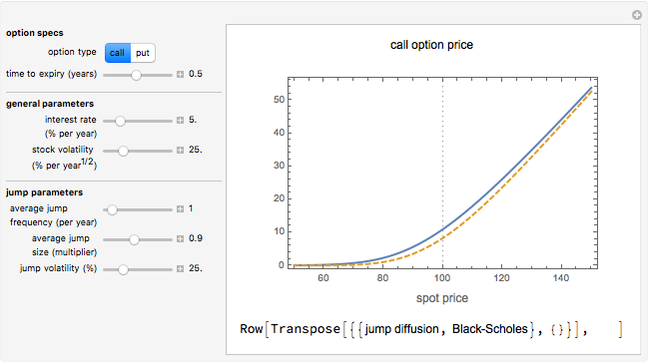

Option Prices in the Kou Jump Diffusion Model

Option Prices in the Kou Jump Diffusion Model

Andrzej Kozlowski Two Jump Diffusion Processes

Two Jump Diffusion Processes

Andrzej Kozlowski Option Prices in Merton's Jump Diffusion Model

Option Prices in Merton's Jump Diffusion Model

Peter Falloon Implied Volatility in Merton's Jump Diffusion Model

Implied Volatility in Merton's Jump Diffusion Model

Peter Falloon Merton's Jump Diffusion Model

Merton's Jump Diffusion Model

Andrzej Kozlowski Distribution of Returns from Merton's Jump Diffusion Model

Distribution of Returns from Merton's Jump Diffusion Model

Peter Falloon The Poisson Process

The Poisson Process

Andrzej Kozlowski Process-Based Cost Model for Sand-Casting Bronze Bells

Process-Based Cost Model for Sand-Casting Bronze Bells

Sam Shames Simulating the Poisson Process

Simulating the Poisson Process

Heikki Ruskeepää Process-Based Cost Model for a Print and Copy Firm

Process-Based Cost Model for a Print and Copy Firm

Sam Shames

-

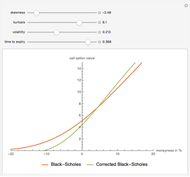

The Black-Scholes European Call Option Formula Corrected Using the Gram-Charlier Expansion

The Black-Scholes European Call Option Formula Corrected Using the Gram-Charlier Expansion

Andrzej Kozlowski -

Option Prices in the Kou Jump Diffusion Model

Andrzej Kozlowski -

The Polar and Bipolar of a Convex Polytope

The Polar and Bipolar of a Convex Polytope

Andrzej Kozlowski -

Two Jump Diffusion Processes

Andrzej Kozlowski -

The Vieta Mapping for the Coxeter Group A_2

The Vieta Mapping for the Coxeter Group A_2

Andrzej Kozlowski -

The Bifurcation Set of the Space of Smooth Real Functions

The Bifurcation Set of the Space of Smooth Real Functions

Andrzej Kozlowski -

The Swallowtail Singularity

The Swallowtail Singularity

Andrzej Kozlowski -

Singularities of an Ellipsoidal Wave Front

Singularities of an Ellipsoidal Wave Front

Andrzej Kozlowski -

Nonuniqueness of Option Pricing Under the Meixner Model

Nonuniqueness of Option Pricing Under the Meixner Model

Andrzej Kozlowski -

Coin Machine

Coin Machine

Andrzej Kozlowski -

A Mean-Reverting Jump Diffusion Process

A Mean-Reverting Jump Diffusion Process

Andrzej Kozlowski -

Standard American and European Options

Standard American and European Options

Andrzej Kozlowski -

Density of the Kou Jump Diffusion Process

Density of the Kou Jump Diffusion Process

Andrzej Kozlowski -

The Meixner Process

The Meixner Process

Andrzej Kozlowski -

Fitting the Meixner Distribution to S&P 500 Returns

Fitting the Meixner Distribution to S&P 500 Returns

Andrzej Kozlowski -

Simple Graphs and Their Binomial Edge Ideals

Simple Graphs and Their Binomial Edge Ideals

Andrzej Kozlowski -

The Eneström-Kakeya Bounds for Roots of a Polynomial with Positive Coefficients

The Eneström-Kakeya Bounds for Roots of a Polynomial with Positive Coefficients

Andrzej Kozlowski -

Newton Polygon and Branching of Algebraic Curves

Newton Polygon and Branching of Algebraic Curves

Andrzej Kozlowski -

Counting the Number of Roots of Transcendental Functions in Bounded Regions Using Winding Numbers

Counting the Number of Roots of Transcendental Functions in Bounded Regions Using Winding Numbers

Andrzej Kozlowski -

The Space of Inner Products

The Space of Inner Products

Andrzej Kozlowski