Lévy Measures

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

The structure of jumps of a Lévy process is determined by its Lévy (or characteristic) measure. For an  -dimensional Lévy process, the Lévy measure of

-dimensional Lévy process, the Lévy measure of  is given by the expected number, per unit time, of jumps whose size belongs to

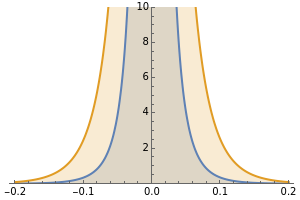

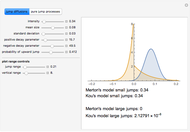

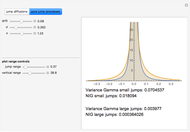

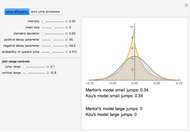

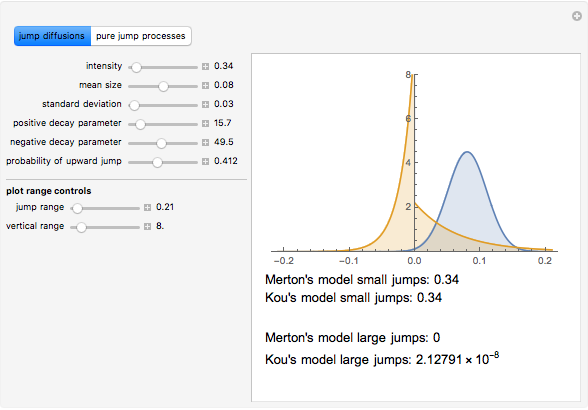

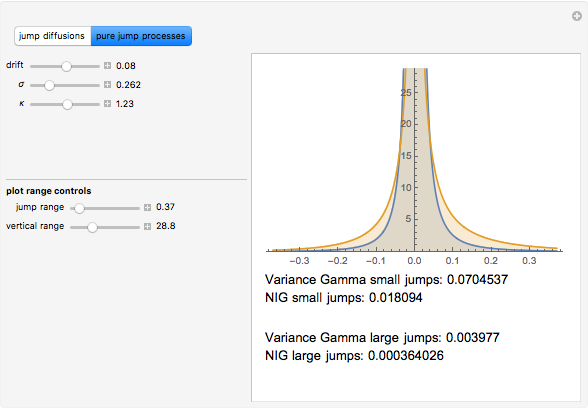

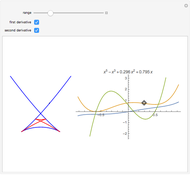

is given by the expected number, per unit time, of jumps whose size belongs to  . This Demonstration compares the Lévy measures of some well-known stochastic processes that have been much used in mathematical finance. They have been divided into two groups: the jump diffusion group, consisting of the Merton and Kou models, and the pure jump processes group, consisting of the Variance Gamma and Normal Inverse Gaussian (NIG) models. The model parametrizations have been chosen to make the comparisons easier. Below the graphs of the densities of the Lévy measures, the total weights of the "small" and "large" jumps are displayed (see the Details section for further explanation). Place the mouse over the graph of a density function to see its name.

. This Demonstration compares the Lévy measures of some well-known stochastic processes that have been much used in mathematical finance. They have been divided into two groups: the jump diffusion group, consisting of the Merton and Kou models, and the pure jump processes group, consisting of the Variance Gamma and Normal Inverse Gaussian (NIG) models. The model parametrizations have been chosen to make the comparisons easier. Below the graphs of the densities of the Lévy measures, the total weights of the "small" and "large" jumps are displayed (see the Details section for further explanation). Place the mouse over the graph of a density function to see its name.

Contributed by: Andrzej Kozlowski (March 2011)

Open content licensed under CC BY-NC-SA

Snapshots

Details

An -dimensional Lévy process  is a stochastic process with time-homogeneous independent increments, such that the sample paths of are left-continuous with right limits (almost surely), and such that

is a stochastic process with time-homogeneous independent increments, such that the sample paths of are left-continuous with right limits (almost surely), and such that  . By the Lévy-Khinchin theorem, Lévy processes are in a one-to-one correspondence with Lévy triples

. By the Lévy-Khinchin theorem, Lévy processes are in a one-to-one correspondence with Lévy triples  , where

, where  is a vector, is a positive definite matrix, and

is a vector, is a positive definite matrix, and  is a positive measure on

is a positive measure on  . The matrix is the volatility matrix of the Brownian motion component of the Lévy process, the Lévy measure determines the jump structure of the process, and the vector , sometimes called the "drift", depends on the choice of truncation function and is not an intrinsic parameter. In this Demonstration we concentrate on the Lévy measure of several well-known one-dimensional Lévy processes. The "jump diffusion" processes have nonzero Brownian component (

. The matrix is the volatility matrix of the Brownian motion component of the Lévy process, the Lévy measure determines the jump structure of the process, and the vector , sometimes called the "drift", depends on the choice of truncation function and is not an intrinsic parameter. In this Demonstration we concentrate on the Lévy measure of several well-known one-dimensional Lévy processes. The "jump diffusion" processes have nonzero Brownian component ( ), while the pure jump processes have no Brownian component (

), while the pure jump processes have no Brownian component ( ).

).

For a fixed  , you can consider jumps of absolute size less than

, you can consider jumps of absolute size less than  as "small jumps" and those of size larger than as "large jumps". In this Demonstration, as in [1] and [6], we take

as "small jumps" and those of size larger than as "large jumps". In this Demonstration, as in [1] and [6], we take  . The "total mass" of jumps of a Lévy process is given by

. The "total mass" of jumps of a Lévy process is given by  (where

(where  is the density of ) and may be finite or infinite (it is finite for the jump diffusion processes presented here and infinite for the ones that are pure jump) but the quantities

is the density of ) and may be finite or infinite (it is finite for the jump diffusion processes presented here and infinite for the ones that are pure jump) but the quantities  and

and  are always finite. Thus to compare large jumps of two processes we can always use their mass, that is, the value of , which we display under the graphs in this Demonstration. However, to compare small jumps, we use the mass

are always finite. Thus to compare large jumps of two processes we can always use their mass, that is, the value of , which we display under the graphs in this Demonstration. However, to compare small jumps, we use the mass  when it is finite (jump diffusions in this Demonstration) and when the mass is infinite (the pure jump cases in this Demonstration). Note also that the Lévy measures of the Variance Gamma and the NIG process have a singularity at 0. The Lévy measure is not a probability measure. In fact, when the measure is finite (e.g., for jump diffusions), the total mass (i.e., the sum of the masses of small and large jumps) is equal to the jump density.

when it is finite (jump diffusions in this Demonstration) and when the mass is infinite (the pure jump cases in this Demonstration). Note also that the Lévy measures of the Variance Gamma and the NIG process have a singularity at 0. The Lévy measure is not a probability measure. In fact, when the measure is finite (e.g., for jump diffusions), the total mass (i.e., the sum of the masses of small and large jumps) is equal to the jump density.

[1] R. Cont and P. Tankov, Financial Modelling with Jump Processes, Boca Raton: CRC Press, 2004.

[2] O. E. Barndorff–Nielsen, "Normal Inverse Gaussian Distributions and Stochastic Volatility Modelling," Scandinavian Journal of Statistics 24(1), 1997 pp. 1–13.

[3] S. Kou, "A Jump-Diffusion Model for Option Pricing," Management Science 48(8), 2002 pp. 1086–1101.

[4] D. B. Madan and E. Seneta, "The Variance Gamma Process (V.G.) Model for Share Market Returns," Journal of Business 63(4), pp. 511–524.

[5] R. Merton, "Option Pricing When Underlying Stock Returns Are Discontinuous," J. Financial Economics 3, 1976 pp. 125–144.

[6]. J. Bertoin, Lévy Processes, Cambridge, UK: Cambridge University Press: 1996.

Permanent Citation

The Black-Scholes European Call Option Formula Corrected Using the Gram-Charlier Expansion

The Black-Scholes European Call Option Formula Corrected Using the Gram-Charlier Expansion

Andrzej Kozlowski Option Prices in the Kou Jump Diffusion Model

Option Prices in the Kou Jump Diffusion Model

Andrzej Kozlowski Two Jump Diffusion Processes

Two Jump Diffusion Processes

Andrzej Kozlowski Standard American and European Options

Standard American and European Options

Andrzej Kozlowski Density of the Kou Jump Diffusion Process

Density of the Kou Jump Diffusion Process

Andrzej Kozlowski Early Exercise of American Options

Early Exercise of American Options

Andrzej Kozlowski Correlated Gamma Variance Processes with Common Subordinator

Correlated Gamma Variance Processes with Common Subordinator

Andrzej Kozlowski The Price of a Call Option on Electrical Power

The Price of a Call Option on Electrical Power

Andrzej Kozlowski The Difference between European Option Prices in the Black-Scholes and NIG Models Computed with the DFT

The Difference between European Option Prices in the Black-Scholes and NIG Models Computed with the DFT

Andrzej Kozlowski The Russian Option: Reduced Regret

The Russian Option: Reduced Regret

Andrzej Kozlowski

-

The Black-Scholes European Call Option Formula Corrected Using the Gram-Charlier Expansion

Andrzej Kozlowski -

Option Prices in the Kou Jump Diffusion Model

Andrzej Kozlowski -

The Polar and Bipolar of a Convex Polytope

The Polar and Bipolar of a Convex Polytope

Andrzej Kozlowski -

Two Jump Diffusion Processes

Andrzej Kozlowski -

The Vieta Mapping for the Coxeter Group A_2

The Vieta Mapping for the Coxeter Group A_2

Andrzej Kozlowski -

The Bifurcation Set of the Space of Smooth Real Functions

The Bifurcation Set of the Space of Smooth Real Functions

Andrzej Kozlowski -

The Swallowtail Singularity

The Swallowtail Singularity

Andrzej Kozlowski -

Singularities of an Ellipsoidal Wave Front

Singularities of an Ellipsoidal Wave Front

Andrzej Kozlowski -

Nonuniqueness of Option Pricing Under the Meixner Model

Nonuniqueness of Option Pricing Under the Meixner Model

Andrzej Kozlowski -

Coin Machine

Coin Machine

Andrzej Kozlowski -

A Mean-Reverting Jump Diffusion Process

A Mean-Reverting Jump Diffusion Process

Andrzej Kozlowski -

Standard American and European Options

Andrzej Kozlowski -

Density of the Kou Jump Diffusion Process

Andrzej Kozlowski -

The Meixner Process

The Meixner Process

Andrzej Kozlowski -

Fitting the Meixner Distribution to S&P 500 Returns

Fitting the Meixner Distribution to S&P 500 Returns

Andrzej Kozlowski -

Simple Graphs and Their Binomial Edge Ideals

Simple Graphs and Their Binomial Edge Ideals

Andrzej Kozlowski -

The Eneström-Kakeya Bounds for Roots of a Polynomial with Positive Coefficients

The Eneström-Kakeya Bounds for Roots of a Polynomial with Positive Coefficients

Andrzej Kozlowski -

Newton Polygon and Branching of Algebraic Curves

Newton Polygon and Branching of Algebraic Curves

Andrzej Kozlowski -

Counting the Number of Roots of Transcendental Functions in Bounded Regions Using Winding Numbers

Counting the Number of Roots of Transcendental Functions in Bounded Regions Using Winding Numbers

Andrzej Kozlowski -

The Space of Inner Products

The Space of Inner Products

Andrzej Kozlowski