Nonuniqueness of Option Pricing Under the Meixner Model

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

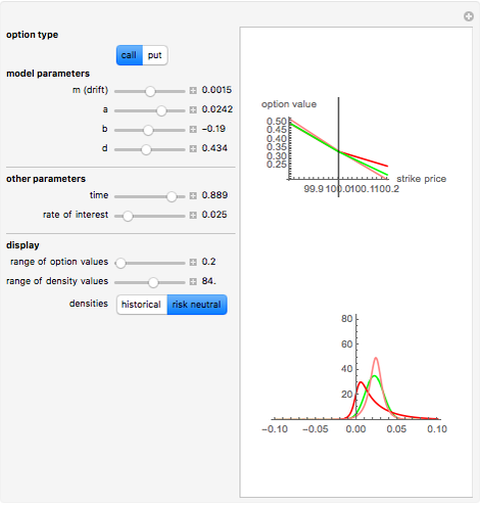

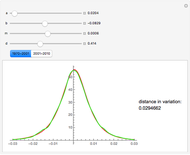

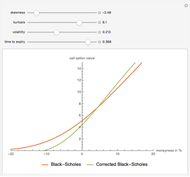

In the classical Black–Scholes model of asset prices, every option has a unique "fair" price; that is, for every price of the underlying asset, there is a unique option price that does not allow arbitrage opportunities. This is no longer true when the Black–Scholes model is replaced by a more realistic model, for example, one in which discontinuous jumps in asset price can occur. This Demonstration shows this for the case where the asset price is modeled by a Meixner process.

[more]

Contributed by: Andrzej Kozlowski (August 2012)

Open content licensed under CC BY-NC-SA

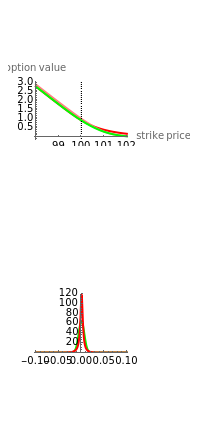

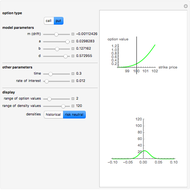

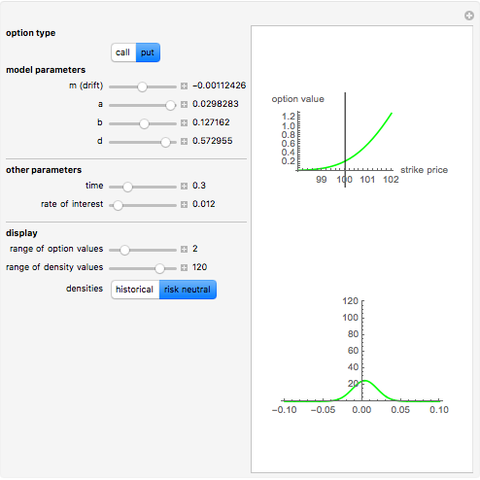

Snapshots

Details

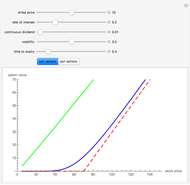

The Black–Scholes model and other one-dimensional diffusion models are examples of complete markets: any option can be perfectly replicated by a self-financing strategy involving the underlying asset and cash. This means that in such models, the price of the underlying parameters and knowledge of the relevant parameters (interest rate and volatility) uniquely determines the "fair" (i.e., arbitrage-free) price of every option. In probabilistic terms, the problem of option pricing reduces to the problem of finding a new probability measure on the space of all possible events, which is equivalent to the real-world measure (in the sense that the sets of impossible events under both measures are the same) but under which the price process is a martingale. In diffusion-based models, there is only one such measure, known as the "equivalent martingale measure".

However, models that allow jumps (e.g., models obtained by replacing the Wiener process by another Lévy process) are incomplete: there are infinitely many martingale measures equivalent to the historical (real-world) measure. A choice of any of these measures will give a consistent (arbitrage-free) system of prices for all options sold in the market. Such a measure can be given by specifying the corresponding probability density function, which can then be used to compute prices of options (as expectations with respect to the new measure). Two of the most popular are obtained by means of the so-called Esscher transform (well-known in actuarial mathematics) and by "mean correction", a method analogous to the one used in Black–Scholes pricing. In this Demonstration, we compare the prices obtained by applying both of these methods to models based on the Meixner process (an infinite-activity Lévy process) and display both the historical and equivalent risk-neutral densities. We also compare the prices and the densities with the corresponding Black–Scholes price and density. For certain values of the parameters, it may be difficult to distinguish the graphs of prices or densities of different models. In such cases, you can obtain a clearer view by adjusting either the option price range slider or the range of the graph of densities. This is particularly useful when we want to compare the tails of the distributions (the Meixner densities are both more peaked and have thicker tails than the normal density).

The starting parameters of the Meixner process are obtained by fitting the Meixner distribution to the returns of the S&P 500 index. One of the bookmarks contains parameters obtained by fitting the Meixner distribution to the returns of the Nikkei index.

Reference

[1] W. Schoutens, Lévy Processes in Finance: Pricing Financial Derivatives, New York: John Wiley & Sons, 2003.

Permanent Citation

"Nonuniqueness of Option Pricing Under the Meixner Model"

http://demonstrations.wolfram.com/NonuniquenessOfOptionPricingUnderTheMeixnerModel/

Wolfram Demonstrations Project

Published: August 16 2012

Option Prices under the Fractional Black-Scholes Model

Option Prices under the Fractional Black-Scholes Model

Andrzej Kozlowski Option Prices in the Kou Jump Diffusion Model

Option Prices in the Kou Jump Diffusion Model

Andrzej Kozlowski The Difference between European Option Prices in the Black-Scholes and NIG Models Computed with the DFT

The Difference between European Option Prices in the Black-Scholes and NIG Models Computed with the DFT

Andrzej Kozlowski Pricing a Bermudan Option with the Longstaff-Schwartz Monte Carlo Method

Pricing a Bermudan Option with the Longstaff-Schwartz Monte Carlo Method

Andrzej Kozlowski The Price of a Call Option on Electrical Power

The Price of a Call Option on Electrical Power

Andrzej Kozlowski Fitting the Meixner Distribution to S&P 500 Returns

Fitting the Meixner Distribution to S&P 500 Returns

Andrzej Kozlowski The Russian Option: Reduced Regret

The Russian Option: Reduced Regret

Andrzej Kozlowski Hedging the European Put Option

Hedging the European Put Option

Andrzej Kozlowski American Call and Put Option

American Call and Put Option

Andrzej Kozlowski Hedging the Black-Scholes Call Option

Hedging the Black-Scholes Call Option

Andrzej Kozlowski

-

The Black-Scholes European Call Option Formula Corrected Using the Gram-Charlier Expansion

The Black-Scholes European Call Option Formula Corrected Using the Gram-Charlier Expansion

Andrzej Kozlowski -

Option Prices in the Kou Jump Diffusion Model

Andrzej Kozlowski -

The Polar and Bipolar of a Convex Polytope

The Polar and Bipolar of a Convex Polytope

Andrzej Kozlowski -

Two Jump Diffusion Processes

Two Jump Diffusion Processes

Andrzej Kozlowski -

The Vieta Mapping for the Coxeter Group A_2

The Vieta Mapping for the Coxeter Group A_2

Andrzej Kozlowski -

The Bifurcation Set of the Space of Smooth Real Functions

The Bifurcation Set of the Space of Smooth Real Functions

Andrzej Kozlowski -

The Swallowtail Singularity

The Swallowtail Singularity

Andrzej Kozlowski -

Singularities of an Ellipsoidal Wave Front

Singularities of an Ellipsoidal Wave Front

Andrzej Kozlowski -

Nonuniqueness of Option Pricing Under the Meixner Model

Nonuniqueness of Option Pricing Under the Meixner Model

Andrzej Kozlowski -

Coin Machine

Coin Machine

Andrzej Kozlowski -

A Mean-Reverting Jump Diffusion Process

A Mean-Reverting Jump Diffusion Process

Andrzej Kozlowski -

Standard American and European Options

Standard American and European Options

Andrzej Kozlowski -

Density of the Kou Jump Diffusion Process

Density of the Kou Jump Diffusion Process

Andrzej Kozlowski -

The Meixner Process

The Meixner Process

Andrzej Kozlowski -

Fitting the Meixner Distribution to S&P 500 Returns

Andrzej Kozlowski -

Simple Graphs and Their Binomial Edge Ideals

Simple Graphs and Their Binomial Edge Ideals

Andrzej Kozlowski -

The Eneström-Kakeya Bounds for Roots of a Polynomial with Positive Coefficients

The Eneström-Kakeya Bounds for Roots of a Polynomial with Positive Coefficients

Andrzej Kozlowski -

Newton Polygon and Branching of Algebraic Curves

Newton Polygon and Branching of Algebraic Curves

Andrzej Kozlowski -

Counting the Number of Roots of Transcendental Functions in Bounded Regions Using Winding Numbers

Counting the Number of Roots of Transcendental Functions in Bounded Regions Using Winding Numbers

Andrzej Kozlowski -

The Space of Inner Products

The Space of Inner Products

Andrzej Kozlowski